The latest preliminary Q3 2025 earnings report from ISC Co., LTD. (ISC) initially caused a stir, with figures falling short of market consensus. But for savvy investors, this moment warrants a deeper look beyond the headline numbers. Is this a sign of weakness, or a temporary pause in a long-term growth story fueled by the AI revolution? At the heart of this story is ISC’s commanding position in the critical AI semiconductor test socket market, a non-negotiable component for the future of technology.

This comprehensive analysis unpacks ISC’s financial performance, explores its unshakeable market leadership, and evaluates the powerful tailwinds and potential risks on the horizon. We’ll provide a clear perspective on why ISC’s fundamental strengths present a compelling long-term thesis.

Decoding the Q3 2025 Earnings Report

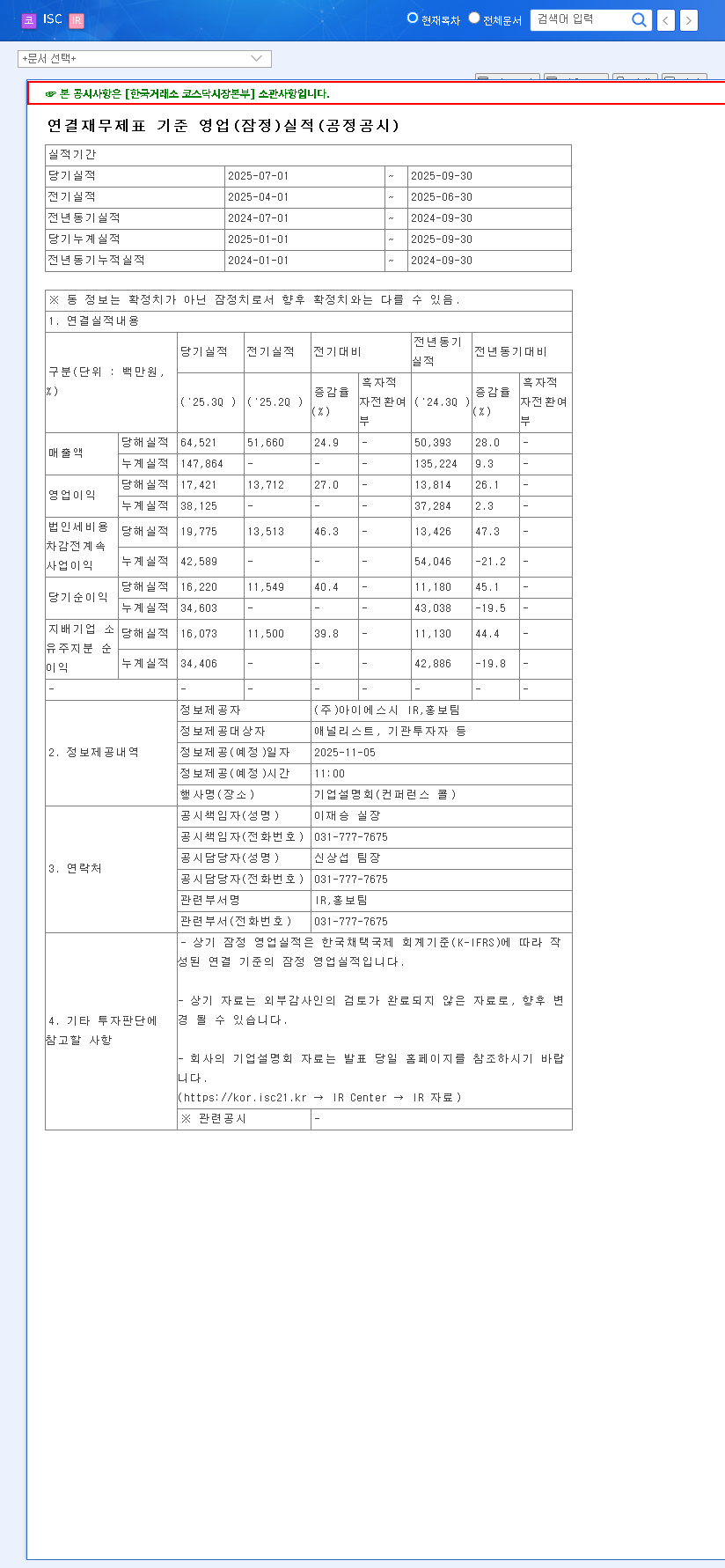

ISC Co., LTD. released its preliminary financial results for the third quarter of 2025, which, while showing growth, did not meet the high expectations set by analysts. This created some short-term market volatility. For a detailed breakdown of the financials, you can review the Official Disclosure filed with DART.

Key Performance Summary vs. Expectations

- •Revenue: KRW 64.5 billion (Missed consensus of KRW 67.6 billion by -5.0%)

- •Operating Profit: KRW 17.4 billion (Missed consensus of KRW 18.8 billion by -7.4%)

- •Net Income: KRW 16.1 billion (Missed consensus of KRW 18.4 billion by -12.5%)

While any miss can be disappointing, context is crucial. This performance comes after a stellar Q2 2025 where revenue and operating profit grew by over 50% quarter-over-quarter. This suggests the Q3 figures may represent a period of normalization or temporary adjustment rather than a fundamental flaw in the company’s growth engine.

The Unwavering Core: Dominance in the AI Semiconductor Test Socket Market

Despite the quarterly noise, ISC’s core fundamentals are stronger than ever. The company is not just a participant but a leader in the high-stakes world of semiconductor test solutions. As AI and machine learning chips become exponentially more complex, the need for sophisticated testing becomes paramount. This is where the AI semiconductor test socket, ISC’s specialty, plays an indispensable role, ensuring the reliability and performance of chips that power our digital world. For more on chip complexity, see this analysis from leading industry experts.

ISC’s market grip is staggering. Non-memory revenue constitutes 85% of their total, with revenue from AI-related products surging to 62% in Q2. Within the generative AI hardware sector, ISC commands a near-monopolistic 95% revenue share.

This dominance is built on unparalleled technological expertise, catering to major AI accelerator and ASIC clients. As flagship smartphones and data centers increasingly rely on advanced AI processors, demand for ISC’s high-performance test sockets is set for structural, long-term growth.

Future Growth Drivers and Financial Stability

ISC is not resting on its laurels. The company is actively cultivating new avenues for growth that complement its core business and fortify its market position.

New Business Synergies

- •Acquired Businesses: Synergies with a recently acquired equipment material business are expected to streamline operations and open up new revenue streams.

- •Expanded Product Lines: The expansion into high-speed burn-in testers and module testers in the second half of the year will tap into adjacent, high-demand market segments.

A Rock-Solid Financial Foundation

Underpinning this growth is a remarkably stable financial structure. Operating cash flow surged to KRW 19.1 billion in the first half of 2025, and the debt-to-equity ratio sits at an exceptionally low 15.67%. This financial prudence gives ISC the flexibility to invest in R&D and navigate economic uncertainties without being over-leveraged.

Balanced Outlook: Navigating Risks and Opportunities

No investment is without risk. It’s crucial to monitor whether the Q3 earnings underperformance was truly temporary or signals a slowdown in market demand. Furthermore, a potential global economic slowdown, hinted at by mixed shipping rate indicators, could indirectly impact the entire semiconductor industry. Competition in the tech-intensive testing market also requires constant vigilance.

However, these risks are balanced by favorable market conditions. Stable interest rates in the US and South Korea reduce borrowing costs, and favorable currency exchange rates positively impact ISC’s export-heavy business model. Most importantly, the AI trend is a powerful secular force that is likely to override cyclical economic downturns.

Investor Takeaway: A Long-Term Vision

The Q3 2025 ISC earnings report may create short-term stock price fluctuations. However, for those with a long-term perspective, such volatility can present a strategic entry point. The core investment thesis for ISC remains intact and compelling.

The unstoppable growth of the AI industry directly translates into sustained demand for ISC’s market-leading AI semiconductor test socket products. Investors should focus on tracking the company’s AI revenue contribution and the progress of its new business ventures. By looking past the quarterly noise and focusing on the powerful fundamentals and structural growth story, one can formulate a wise and prudent investment strategy. To learn more about this sector, read our Guide to Investing in the AI Hardware Boom.

Leave a Reply