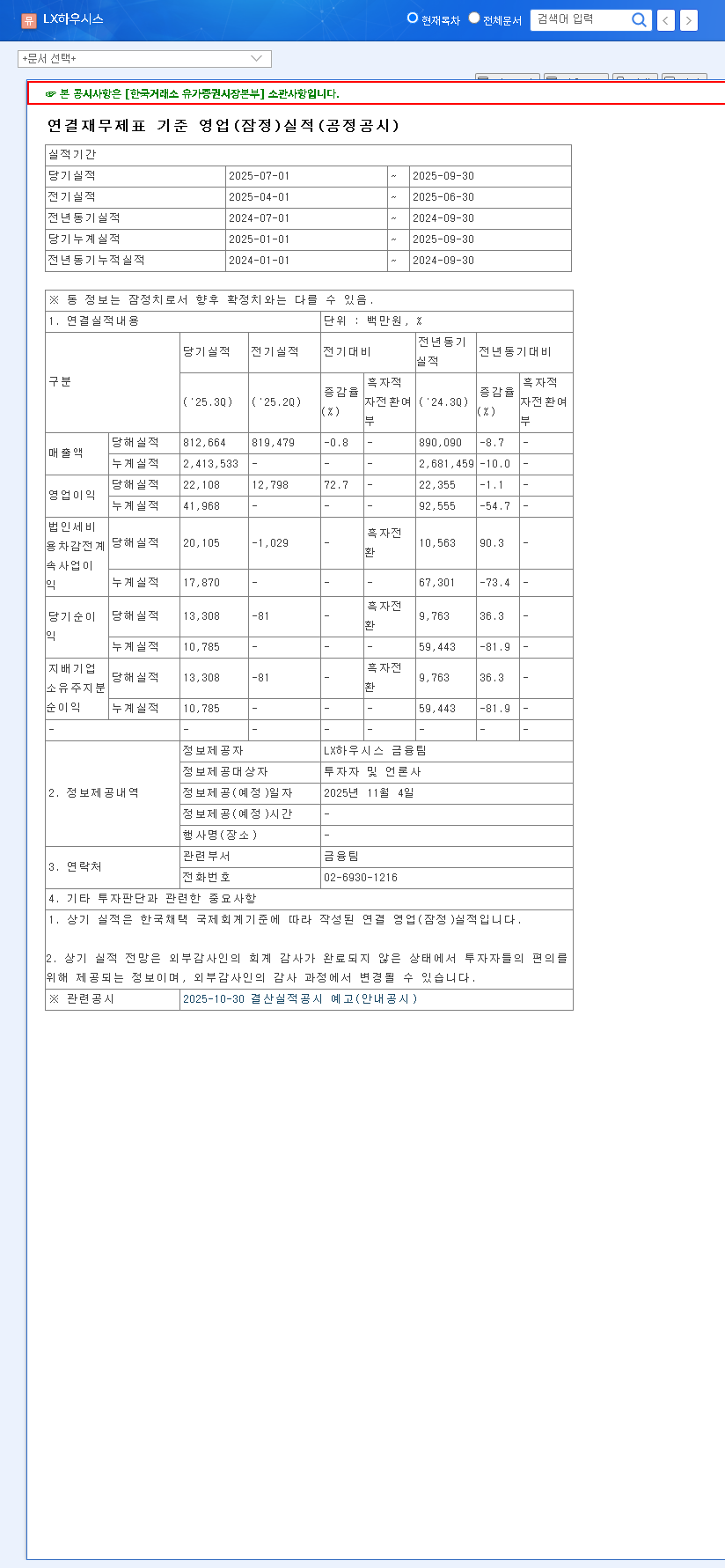

The latest LX HAUSYS Q3 earnings report for 2025 has sent ripples through the market. On November 4, 2025, LX HAUSYS, LTD. (108670) announced preliminary results that defied expectations. Despite navigating a turbulent economic landscape with high interest rates and a sluggish housing market, the company posted an operating profit that beat consensus by 26% and a net profit that skyrocketed 93% above predictions—a definitive ‘earnings surprise’. This detailed analysis unpacks the performance, explores the driving forces, and provides a forward-looking perspective for investors.

What fueled this remarkable profitability? How does the persistent weakness in the building materials sector weigh against the soaring success of automotive materials? We will delve into the core numbers, assess the implications for LX HAUSYS stock, and outline the strategic path forward.

Unpacking the LX HAUSYS Q3 Earnings Report

The official Q3 2025 preliminary results, which you can view in the Official Disclosure (DART), presented a mixed but ultimately positive picture. While top-line revenue saw a slight dip, profitability metrics told a story of operational excellence and strategic success in key growth areas.

Performance vs. Market Consensus

- •Revenue: KRW 812.7 billion, which was 3% below the market expectation of KRW 839.9 billion.

- •Operating Profit: KRW 22.1 billion, a significant 26% above the market expectation of KRW 17.5 billion.

- •Net Profit: KRW 13.3 billion, an astounding 93% above the market expectation of KRW 6.9 billion.

The key takeaway is clear: While facing revenue headwinds, LX HAUSYS demonstrated impressive control over its costs and capitalized on high-margin segments, leading to a substantial beat on the bottom line.

The Twin Engines: Automotive Soars, Building Materials Stalls

The Q3 results highlight a stark divergence in the performance of LX HAUSYS’s main divisions. Understanding this dynamic is crucial for any LX HAUSYS stock analysis.

Driver 1: Robust Growth in Automotive & Industrial Films

The Automotive Materials division continued its powerful growth trajectory, serving as the primary engine for the profit surprise. This segment is benefiting from several powerful secular trends, including the global shift toward electric vehicles (EVs) and a consumer preference for premium, high-tech vehicle interiors. As automakers invest in more sophisticated cabin experiences, demand for LX HAUSYS’s advanced films and materials has surged, significantly boosting the company’s profitability and revenue mix.

Driver 2: Disciplined Cost Management

In a challenging macroeconomic environment, as detailed by sources like Reuters on global economic trends, effective cost control becomes paramount. LX HAUSYS has demonstrated exceptional discipline in managing operational expenses, optimizing its supply chain, and improving manufacturing efficiency. This financial prudence was a critical factor in converting revenue into a much healthier operating profit than the market anticipated.

The Drag: Persistent Sluggishness in Building Materials

Conversely, the Building Materials division remains the company’s primary headwind. The continued downturn in the housing and construction markets, fueled by high interest rates, has suppressed demand for core building products. This division’s struggle is the main reason for the overall revenue miss and raises structural questions about its long-term growth prospects in the current economic cycle. The company’s future success will partly depend on its ability to innovate within this segment, potentially through a greater focus on the remodeling and renovation market.

Investor Outlook: Short-Term Optimism vs. Long-Term Questions

This LX HAUSYS earnings surprise will likely have a positive, albeit potentially short-lived, impact on the stock price. Investors must weigh the immediate good news against underlying risks.

- •Positive Signal: The strong profitability proves the company’s resilience and the success of its diversification into the high-growth automotive sector. This re-confirms the automotive segment as a core value driver.

- •Risk Factor: The structural weakness in the building materials division cannot be ignored. A sustained slump in construction could continue to drag on overall revenue and cap long-term growth potential.

- •External Threats: Macroeconomic headwinds, including interest rate volatility and geopolitical risks, remain significant. Furthermore, the potential financial impact from the ongoing silica exposure lawsuit requires careful monitoring by investors.

Strategic Path Forward for Sustainable Growth

To sustain this momentum, LX HAUSYS must pursue a dual strategy: optimizing its legacy business while aggressively expanding its growth engine.

For Building Materials, the focus should be on shifting the portfolio towards high-value, eco-friendly products for the renovation market, which is often more resilient than new construction. For Automotive Materials, the strategy should involve expanding its technological lead and exploring adjacent markets like autonomous driving components and Urban Air Mobility (UAM) to secure future dominance.

Conclusion: A Promising Yet Challenging Road Ahead

The LX HAUSYS Q3 earnings report is a testament to the company’s successful strategic pivot and operational discipline. The outstanding performance of the automotive division has more than compensated for the struggles in the building materials segment, delivering a powerful message to the market. However, the path forward requires navigating significant external risks and addressing the structural challenges in its foundational business. Investors should feel encouraged by the short-term results but remain vigilant, closely monitoring the recovery of the construction market and the continued growth trajectory of the automotive business to make informed long-term decisions.

Leave a Reply