The latest Daeduck Electronics earnings report for Q3 2025 has sent a powerful shockwave through the market, signaling a potential major turnaround for the tech component giant. Amidst the persistent volatility of the IT industry, Daeduck Electronics Co., Ltd. (353200) delivered a performance that didn’t just meet, but dramatically exceeded market expectations. This comprehensive analysis will break down the ‘surprise earnings,’ explore the fundamental drivers, and provide a forward-looking perspective for investors evaluating Daeduck Electronics stock.

Q3 2025 Daeduck Electronics Earnings: By The Numbers

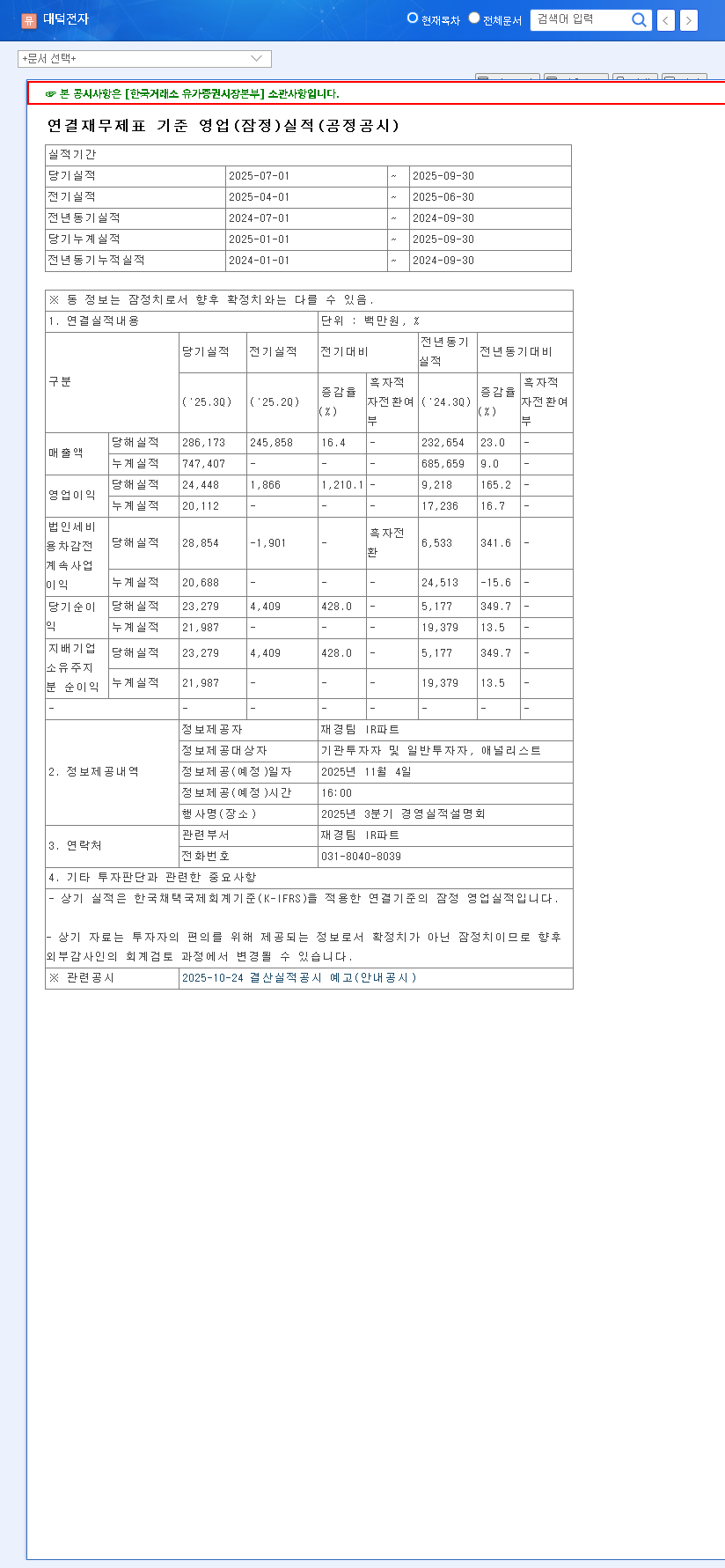

On November 4, 2025, Daeduck Electronics announced its preliminary Q3 earnings, effectively crushing consensus estimates and reversing the losses from the previous two quarters. The figures, confirmed by their Official Disclosure, paint a clear picture of resurgence:

- •Revenue: KRW 286.2 billion, which is +4.4% above the market estimate of KRW 274.0 billion.

- •Operating Profit: KRW 24.4 billion, a staggering +44.4% above the market estimate of KRW 16.9 billion.

- •Net Profit: KRW 23.3 billion, an impressive +53.3% above the market estimate of KRW 15.2 billion.

The most crucial takeaway is the dramatic shift from consecutive losses in Q1 and Q2 to a substantial profit in Q3. This isn’t just a beat; it’s a powerful statement about the company’s operational health and market positioning.

What’s Fueling the Turnaround?

This stellar performance wasn’t a fluke. It’s the result of a powerful synergy between strengthening internal fundamentals and a more favorable external market environment, creating a perfect storm for growth.

1. Robust Corporate Fundamentals

Daeduck’s core business revolves around manufacturing high-value Printed Circuit Boards (PCBs), the foundational components for nearly all modern electronics. The company has successfully pivoted to high-demand sectors:

- •Surging AI & Server Demand: The global boom in AI requires advanced PCBs like Flip Chip Ball Grid Arrays (FC-BGA) for powerful processors. Daeduck is a key player in this high-margin segment, directly benefiting from the growth of data centers and AI hardware. For more on this technology, see this in-depth overview of advanced semiconductor packaging.

- •Improved Profitability: The Q3 operating profit margin hit approximately 8.52%, a significant leap from previous estimates. This demonstrates successful cost management and a focus on higher-value products.

- •Stable Financials: A consistently declining debt-to-equity ratio, dropping from 267% in 2022 to a projected 230% in 2024, points towards a healthier and more resilient financial structure.

2. A Favorable Market Environment

External factors have also aligned to bolster the Daeduck Electronics earnings report:

- •IT Industry Recovery: After a period of inventory correction, demand from major customers like Samsung Electronics and SK Hynix is stabilizing. The relentless growth in AI, autonomous driving, and 5G/6G provides a strong, ongoing demand pipeline for high-performance PCBs.

- •Macroeconomic Tailwinds: As an export-heavy company, the stabilization of the KRW/USD exchange rate provides predictability. Furthermore, declining oil prices and international freight costs have eased the burden on logistics and raw material procurement, directly boosting the bottom line.

Investor Outlook: What’s Next for Daeduck Electronics Stock?

The strong earnings report is expected to significantly improve investor sentiment and act as a positive catalyst for the Daeduck Electronics stock price. However, investors should weigh both the opportunities and potential risks.

The Bull Case (Reasons for Optimism)

- •Proven profitability and operational efficiency.

- •Strong positioning in high-growth markets (AI, automotive).

- •Continued recovery in the broader semiconductor and IT industries.

- •Strengthening financial health and reduced debt load.

The Bear Case (Points of Caution)

- •Sustainability: One strong quarter is excellent, but the market will be watching Q4 and 2026 guidance to confirm this is a sustained trend, not a one-off rebound.

- •Global Economy: Any significant global economic downturn could curb IT spending and impact demand.

- •Competition: The PCB industry is highly competitive, and maintaining a technological and pricing edge is a constant battle.

In conclusion, the Q3 2025 Daeduck Electronics earnings are a resounding signal of a company on the mend, firing on all cylinders. While macroeconomic risks remain, the combination of strong execution and alignment with key tech trends provides a compelling case for a sustained turnaround. Investors should continue to monitor industry demand and the company’s Q4 results closely. For further reading, consider our guide on How to Analyze Tech Component Stocks.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. The final responsibility for investment decisions rests with the investor.

Leave a Reply