The Korean pharmaceutical landscape is buzzing with anticipation as YUHAN CORPORATION, a titan in the industry, prepares to unveil its Q3 2025 earnings on November 5th. Investors and analysts are laser-focused on one key question: can the company maintain the phenomenal momentum established in the first half of the year? Central to this narrative is the global performance of its blockbuster lung cancer treatment, Lazertinib. This comprehensive stock analysis will dissect YUHAN’s robust fundamentals, evaluate the market forces at play, and provide a clear outlook on what to expect from the upcoming investor relations (IR) event.

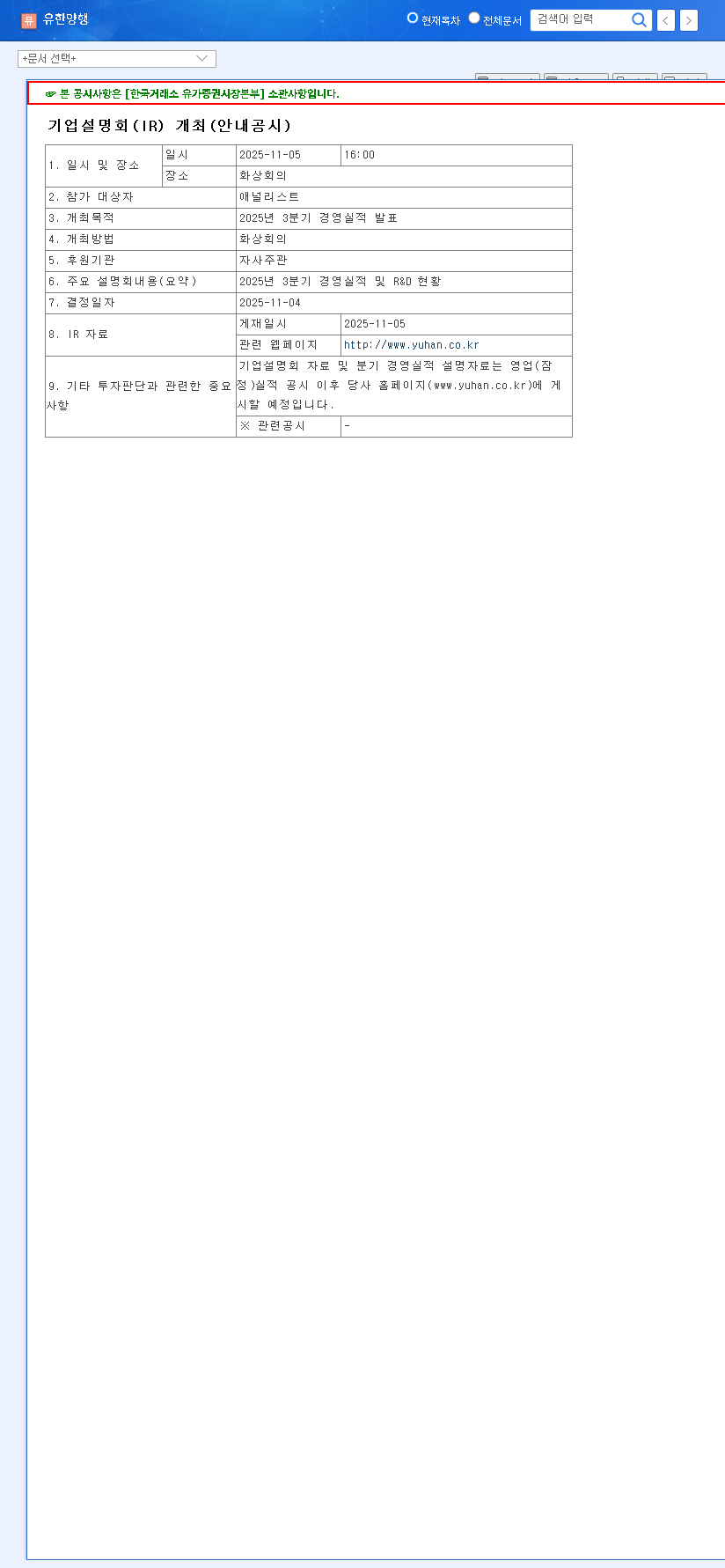

On November 5, 2025, at 4:00 PM KST, YUHAN CORPORATION will host its much-awaited IR call to present its Q3 2025 performance and R&D pipeline updates. This event is a critical data point for assessing the company’s trajectory and the efficacy of its growth strategies. The official announcement details can be reviewed in the company’s Official Disclosure on DART.

A Foundation of Strength: Recapping H1 2025 Performance

To understand the expectations for the YUHAN earnings report, we must first look at its stellar performance in the first half of 2025. The company has already laid a foundation of impressive growth, demonstrating financial resilience and operational excellence. Revenue climbed to KRW 1.07 trillion, a solid 10.0% increase year-over-year. More strikingly, operating profit skyrocketed by an incredible 194.4% to KRW 56.2 billion, while net profit grew 26.4% to KRW 54 billion. These figures paint a picture of a company firing on all cylinders, driven by both its core pharmaceutical business and expanding overseas operations.

Lazertinib: The Billion-Dollar Engine of Growth

The primary driver behind YUHAN CORPORATION’s success is unequivocally Lazertinib (brand name: Leclaza), a third-generation EGFR tyrosine kinase inhibitor (TKI) for treating non-small cell lung cancer (NSCLC). This innovative drug has become a cornerstone of the company’s portfolio, with its global expansion strategy now bearing significant fruit. Positive clinical outcomes and growing adoption in key markets across Europe, Japan, and China are fueling its revenue growth. The global NSCLC market is substantial and growing, representing a massive opportunity that YUHAN is effectively capturing. For more on the global impact of this disease, you can reference data from leading health bodies like the World Health Organization.

The continued global market penetration of Lazertinib is the single most important catalyst for YUHAN CORPORATION. Its performance in Q3 will be a powerful indicator of the company’s long-term international success.

Future-Proofing: R&D and Financial Prudence

A leading Korean pharmaceutical company cannot rest on a single product. YUHAN is actively investing in its future, allocating approximately 10% of its revenue to R&D. The company is embracing cutting-edge technology, leveraging AI and big data to accelerate drug discovery and development. This, combined with an open innovation strategy that fosters collaboration, is expected to significantly strengthen its pipeline for years to come. Financially, YUHAN remains a fortress. With total equity of KRW 2.21 trillion and a conservative debt-to-equity ratio of 37.22%, the company is well-capitalized to fund its growth initiatives without undue risk.

Investment Thesis: What to Watch in the Q3 Report

Based on current momentum, we maintain a ‘BUY’ investment opinion on YUHAN CORPORATION. The upcoming IR call will be pivotal in confirming this outlook. Here are the key factors that could impact the stock price.

Potential Positive Catalysts

- •Continued Lazertinib Momentum: Stronger-than-expected sales figures for Lazertinib in Q3 would be a significant positive, confirming its blockbuster status and global appeal.

- •Positive R&D Updates: Any concrete progress announced on other pipeline candidates, particularly those developed using their AI platform, would boost confidence in future growth engines.

- •Enhanced Shareholder Returns: Reaffirmation or an accelerated timeline for the announced dividend increases and treasury share cancellation plan (2025-2027) would be very well-received by the market.

Potential Risks and Headwinds

- •Healthcare Business Slump: While the pharma segment thrives, the healthcare division has been a weak point. A continued slump could drag on overall sentiment.

- •Unexpected R&D Setbacks: Any negative clinical trial data or delays in the pipeline could cause short-term volatility in the stock price.

- •Macroeconomic Volatility: Unfavorable shifts in currency exchange rates (USD/KRW) or sharp interest rate hikes could negatively impact profitability and investor sentiment.

Conclusion: A Compelling Growth Story

YUHAN CORPORATION presents a compelling case for investors. The company’s growth is not speculative; it’s anchored by the tangible success of Lazertinib, supported by a robust financial position, and fueled by a forward-looking R&D strategy. While risks exist, the potential catalysts appear to outweigh the headwinds. We advise investors to closely monitor the Q3 YUHAN earnings call for confirmation of these positive trends. For more background, you can review our previous H1 2025 performance review. The November 5th announcement will be a key moment in validating YUHAN’s position as a premier Korean pharmaceutical investment.

Leave a Reply