The recent DK&D share cancellation announcement has created significant buzz among investors. On November 4, 2025, DK&D CO.,LTD (KRX: 263020) confirmed its decision to cancel a substantial number of treasury shares, a move often seen as a direct commitment to enhancing shareholder value. But what does this corporate action truly signify for the company’s future and its stock price?

This comprehensive analysis will dissect the event, examining DK&D’s underlying fundamentals, the direct financial impacts of the cancellation, and the broader macroeconomic factors at play. We’ll provide a clear, balanced perspective to help you make more informed investment decisions regarding DK&D stock.

The DK&D Share Cancellation: Key Details

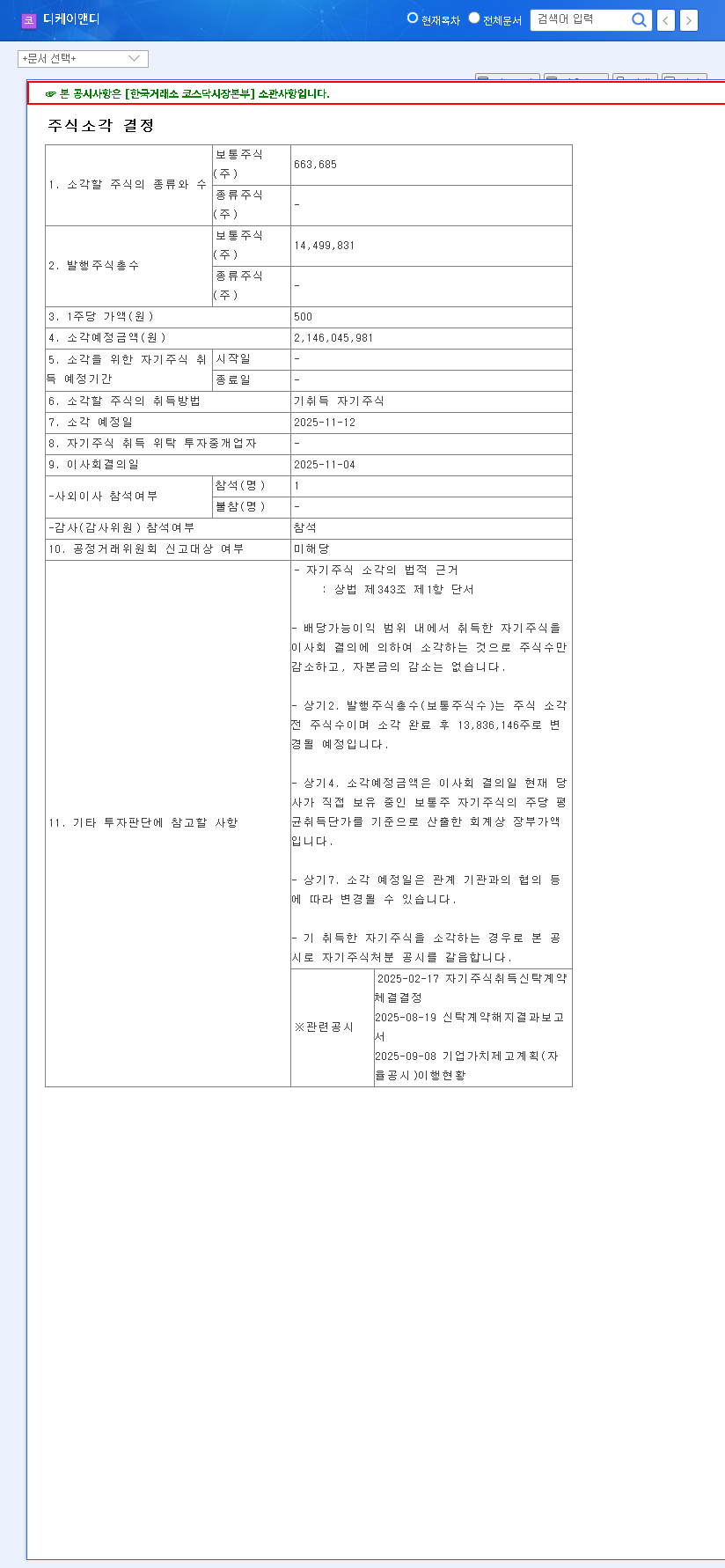

On November 4, 2025, DK&D’s board officially approved the cancellation of treasury stock. This is not a share buyback where the company purchases shares from the open market; rather, these are shares the company already owns. The primary goal of such a shareholder return policy is to reduce the total number of outstanding shares, thereby increasing the ownership stake of each remaining shareholder.

Here are the essential facts based on the official filing:

- •Shares to be Canceled: 663,685 common shares

- •Estimated Value: Approximately 2.1 billion KRW

- •Market Cap Impact: Represents roughly 4.92% of the company’s market capitalization.

- •Scheduled Date: November 12, 2025

- •Source: Official Disclosure (DART Report)

Analyzing the Impact on Shareholder Value

The core benefit of a treasury stock cancellation is the direct enhancement of per-share metrics. By reducing the denominator (total shares), key indicators like Earnings Per Share (EPS) and Book Value Per Share (BPS) automatically increase, assuming earnings and book value remain constant. This is a powerful, tax-efficient way to return value to shareholders compared to dividends.

By canceling nearly 5% of its shares, DK&D is sending a strong signal that management believes its stock is undervalued and is confident in its future earnings potential. This can significantly boost investor sentiment.

Positive Catalysts for DK&D Stock

- •Improved Financial Ratios: The immediate increase in EPS can make the stock appear cheaper on a price-to-earnings (P/E) basis, potentially attracting value investors. Learn more about how Earnings Per Share (EPS) is calculated.

- •Supply and Demand Dynamics: Reducing the supply of available shares can, in theory, lead to a higher price per share if demand remains stable or increases.

- •Management Confidence: This action signals that the company’s leadership has faith in its long-term prospects and believes investing in its own stock is a prudent use of capital.

A Look at DK&D’s Financial Health (H1 2025)

While the share cancellation is a positive headline, it’s crucial to evaluate it within the context of the company’s recent performance. The H1 2025 report presents a mixed but generally stable picture. For a deeper dive, investors should review our guide on analyzing company financial statements.

Strengths and Growth Areas

Consolidated revenue grew an impressive 29.4% year-over-year to 67.5 billion KRW. This growth was driven by solid performance across its core segments: synthetic leather, non-woven fabrics, and particularly its hat business, which saw a surge in exports. The company’s strategic focus on eco-friendly materials and new B2C channels also suggests forward-thinking leadership.

Points of Caution

Despite strong revenue, net profit fell by 53.3% to 3.47 billion KRW. This decline was attributed to lower operating profit in the hat division and a one-time loss from the disposal of subsidiary shares. Furthermore, H1 2025 operating cash flow was negative, a metric to monitor closely. However, the company’s financial stability remains robust, with a low debt-to-equity ratio of just 39.96%, mitigating concerns about leverage.

Macroeconomic Headwinds to Consider

No company operates in a vacuum. DK&D’s export-heavy model makes it susceptible to several external risks:

- •Exchange Rate Fluctuations: A strengthening Korean Won (KRW) against the USD or EUR can erode the value of international sales and hurt profitability.

- •Interest Rate Environment: While DK&D’s low debt is a shield, a sustained high-interest-rate climate can increase future borrowing costs and dampen overall economic activity.

- •Commodity and Freight Costs: Volatility in oil prices and global shipping rates can directly impact raw material costs and supply chain efficiency.

Final Verdict: A Cautiously Optimistic Outlook

The DK&D share cancellation is a fundamentally positive development for shareholders. It is a clear and decisive action that enhances per-share value and signals management’s confidence.

However, investors should balance this positive signal with a pragmatic view of the company’s challenges. The recent decline in net profitability, although partly due to a one-off event, requires monitoring. Similarly, the macroeconomic environment poses tangible risks to DK&D’s export-oriented business model. In conclusion, this event strengthens the long-term investment case for DK&D, but investors should continue to track quarterly earnings and external economic indicators before making significant capital allocations.

Leave a Reply