For investors tracking the financial sector, the latest preliminary report from Lotte Non-Life Insurance presents a fascinating and complex picture. The company’s Q3 2025 earnings reveal a significant surge in profitability, a welcome sign after previous volatility. However, this profit growth is set against a backdrop of declining revenue and concerns over its capital adequacy. This comprehensive analysis will dissect these results, explore the underlying drivers, and evaluate the critical risks, providing a clear outlook for potential and current investors.

Lotte Non-Life Insurance Q3 2025 Earnings at a Glance

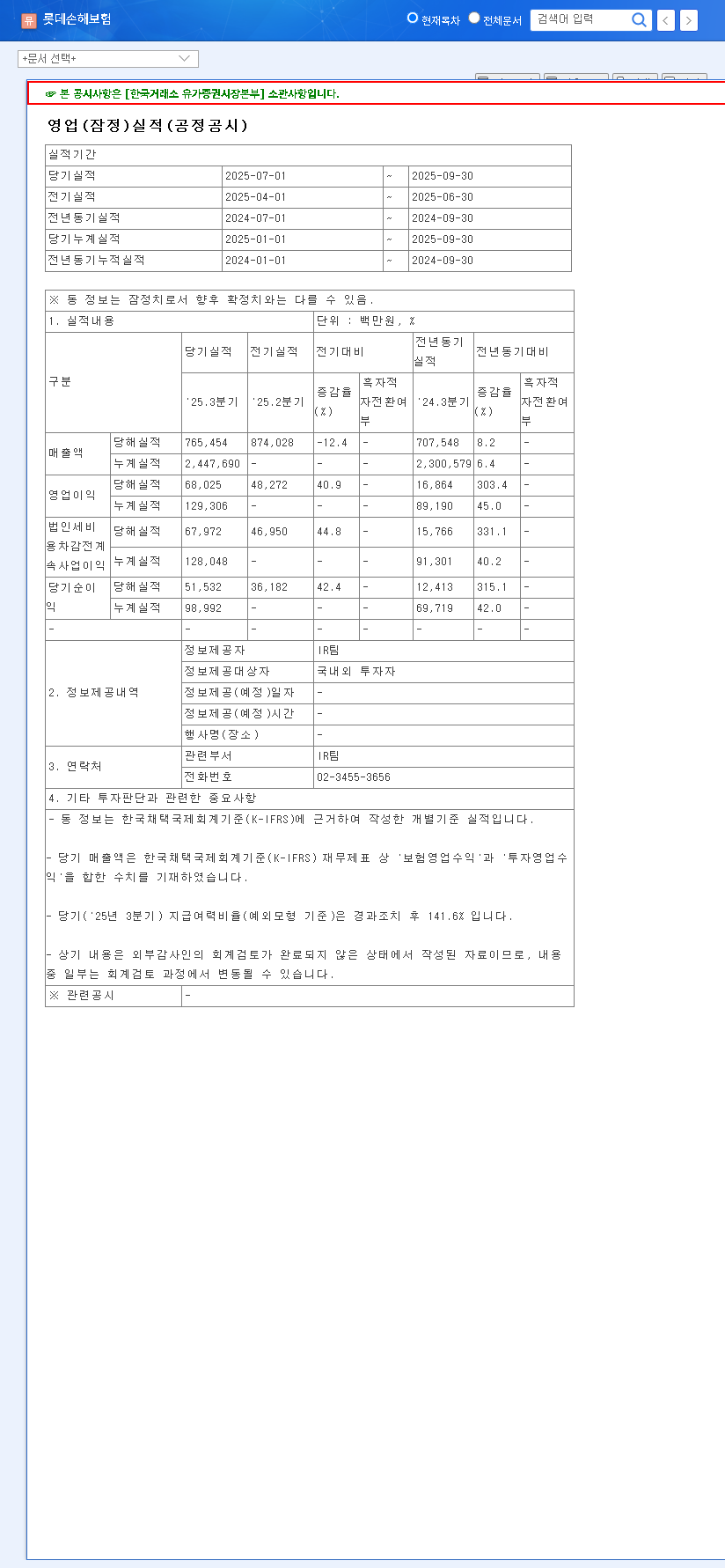

Lotte Non-Life Insurance has released its preliminary operating results for the third quarter of 2025, showing a remarkable turnaround in profitability. Here are the headline figures:

- •Revenue: KRW 765.5 billion (a decrease from Q2)

- •Operating Profit: KRW 68 billion (a 40.8% increase quarter-over-quarter)

- •Net Profit: KRW 51.5 billion (a 42.3% increase quarter-over-quarter)

These figures, derived from the company’s official filing, paint a clear picture of enhanced operational efficiency. For verification, you can view the Official Disclosure (DART). The primary takeaway is the impressive profit jump despite lower top-line revenue, signaling a potential strategic shift towards higher-margin business lines or improved asset management.

Analyzing the Drivers of Profitability

Core Operational Improvements

The sharp increase in operating and net profit suggests that the value-driven strategies implemented by Lotte Non-Life Insurance are beginning to bear fruit. This could stem from several factors, including more disciplined underwriting, a reduction in the loss ratio for key insurance products, or superior performance from its investment portfolio. The resolution of negative one-off factors from the second quarter likely also played a significant role in this recovery.

Macroeconomic Tailwinds

The broader economic environment has provided a mixed but potentially favorable landscape. A high-interest-rate environment can bolster investment returns for insurers, who hold vast portfolios of fixed-income securities. Furthermore, favorable exchange rate movements (rising KRW/USD and KRW/EUR) can create translation gains on foreign currency assets, boosting the bottom line. These external factors are crucial for understanding the sustainability of the current profit levels. For more on this, you can read about how interest rates impact insurance companies.

While the Q3 profit surge is a strong positive signal, the declining K-ICS solvency ratio introduces a critical element of risk that investors must not overlook. It’s a classic case of balancing short-term performance with long-term financial stability.

The Elephant in the Room: K-ICS Solvency Ratio

A critical metric for any insurer is its solvency ratio, which measures its ability to meet long-term debt obligations. In Korea, this is measured by the K-ICS (Korean Insurance Capital Standard). The latest report reveals a concerning trend for Lotte Non-Life Insurance:

- •K-ICS Ratio (Exception Model): 129.46%

- •K-ICS Ratio (Standard Model): 103.70%

While these figures are above the regulatory minimum, they represent a decline from previous periods. A falling K-ICS solvency ratio can be a red flag, indicating potential future pressure to raise capital, which could dilute existing shareholders, or a reduced capacity for aggressive investment and growth. This is a significant risk factor that counterbalances the positive earnings news.

Investor Playbook & Future Outlook

The Q3 2025 results for Lotte Non-Life Insurance are encouraging, but it is premature to declare a complete fundamental recovery. Cautious optimism is the most prudent approach. Investors should closely monitor the following key areas in upcoming quarters:

- •Profit Sustainability: Is the Q3 performance an anomaly, or can the company maintain this level of profitability? Look for consistent operating margins.

- •Revenue Trend Reversal: A continued decline in revenue, even with high profits, could signal a shrinking market share. Watch for a stabilization or return to top-line growth.

- •K-ICS Ratio Management: Any further deterioration in the solvency ratio would be a major concern. Look for management commentary and actions aimed at shoring up their capital base. You can review our archive of Lotte’s past performance reports for historical context.

In conclusion, Lotte Non-Life Insurance has demonstrated a strong improvement in its core earnings power. However, the accompanying risks, particularly the declining solvency ratio, require careful and continuous monitoring. The path forward will depend on the company’s ability to manage these competing forces effectively.

Leave a Reply