The recent news of a significant private equity investment in LB SEMICON, INC. has captured the attention of the market, leaving many investors analyzing the future of LB SEMICON stock. A consortium of investment funds, led by UAMCO-KB Credit No. 1 Private Equity Fund, has secured a substantial 15.88% stake in the company through the acquisition of convertible bonds. While the stated purpose is a ‘simple investment,’ this move has profound implications for the company’s trajectory, governance, and shareholder value. This comprehensive analysis will break down the deal, evaluate LB SEMICON’s current fundamentals, and provide a strategic outlook for investors.

Breaking Down the Investment Deal

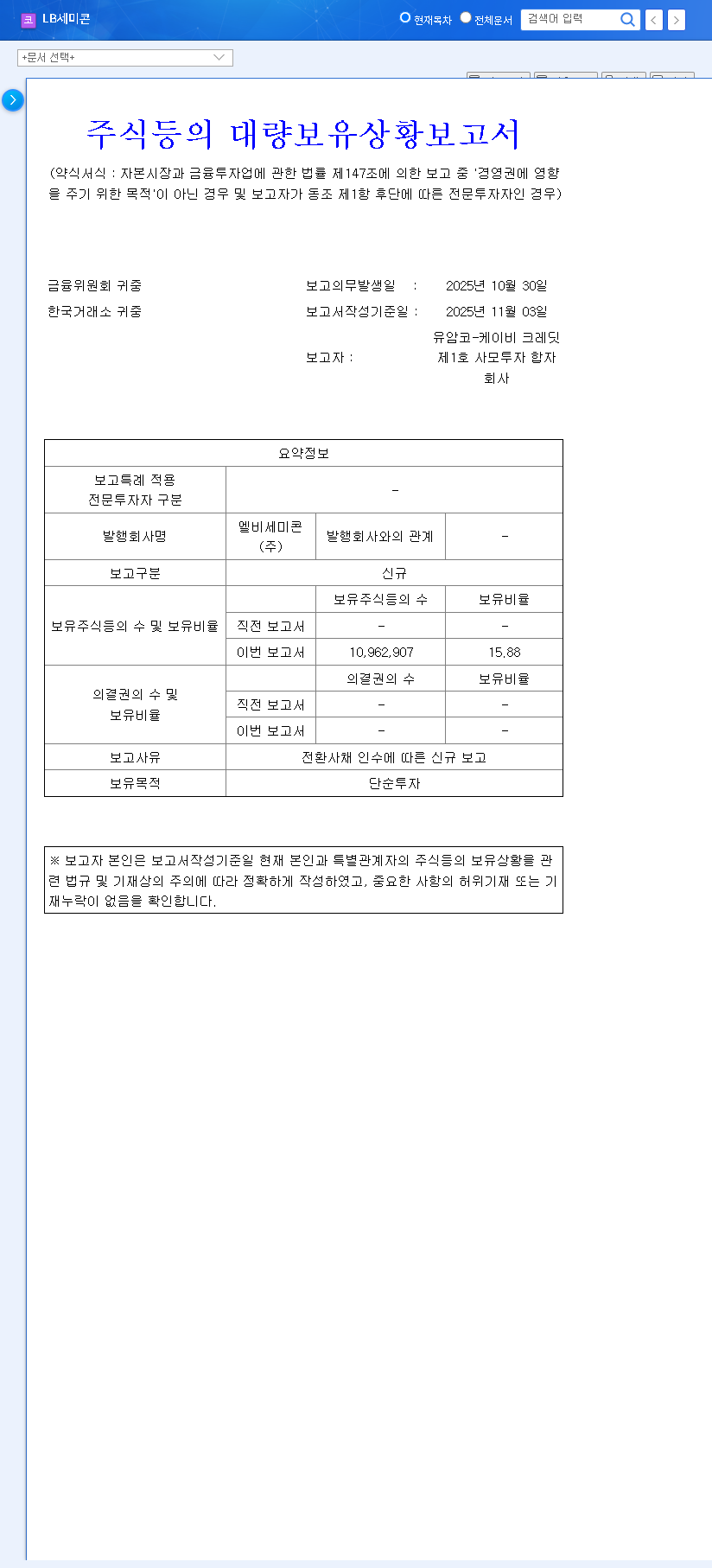

On November 3, 2025, a significant shareholding report was filed, revealing a major new position in LB SEMICON. According to the Official Disclosure, the acquisition involves several entities acquiring a total of 10,962,907 shares via convertible bonds, amounting to a 15.88% stake. The key players are:

- •UAMCO-KB Credit No. 1 Private Equity Fund: 4,567,878 shares

- •KB Digital Platform Fund: 1,827,151 shares

- •KB SBI Global Advanced Strategy Private Equity Fund: 4,567,878 shares

The declaration of a “simple investment” purpose is crucial. It signals that the funds do not intend a hostile takeover, but rather aim to capitalize on the company’s potential growth. This type of private equity investment is often seen as a vote of confidence in a company’s long-term strategy and management.

Current Financial Health: A Reality Check for LB SEMICON

To understand the impact of this investment, we must first assess LB SEMICON’s current financial standing. The H1 26th fiscal year report paints a challenging picture, highlighting areas where this new capital could be pivotal.

Profitability and Cash Flow Concerns

Despite a modest 2.8% year-over-year revenue increase to KRW 232.5 billion, profitability has worsened. The company reported an operating loss of KRW 7.3 billion and a net loss that ballooned to KRW 13.77 billion. These figures are driven by rising costs and derivative valuation losses. Furthermore, operating cash flow turned negative to a KRW 12.9 billion outflow, strained by a heavier working capital burden. This indicates that while sales are occurring, the company is struggling to convert them into cash efficiently.

Balance Sheet Pressures

The balance sheet also shows signs of stress. A concerning 88% surge in inventory assets suggests potential issues with demand or management efficiency. Simultaneously, the debt-to-equity ratio has climbed to 125.1%, signaling an increased financial risk. While the merger with LB Lusem Co., Ltd. boosted capital surplus, the overall financial position requires careful management and strategic intervention.

This private equity investment arrives at a critical juncture for LB SEMICON. While fundamentals show strain, the infusion of capital and confidence could be the catalyst needed to navigate market headwinds and capitalize on growth opportunities in the semiconductor OSAT industry.

The Two Sides of the Coin: Impact on LB SEMICON Stock

The Bull Case: Potential Positive Catalysts

- •Enhanced Stability: A large, stable shareholder base can fortify corporate governance and allow management to focus on long-term strategic goals without fear of hostile takeovers.

- •Market Validation: Investment from reputable private equity funds serves as a strong market signal, validating LB SEMICON’s growth potential in advanced packaging (WLP, FOWLP) for AI and autonomous driving sectors. This can ease future fundraising efforts.

- •Increased Attention: Major shareholding changes often draw market attention, potentially boosting trading volume and short-term volatility for LB SEMICON stock.

The Bear Case: Potential Risks for Investors

The primary risk stems from the investment vehicle itself: convertible bonds. These debt instruments can be converted into a predetermined number of common shares. This introduces several concerns:

- •Stock Dilution: If and when these bonds are converted, the total number of outstanding shares will increase. This dilutes the ownership percentage of existing shareholders and can put downward pressure on earnings per share (EPS) and the stock price.

- •Conversion Price Adjustments: The terms of the convertible bonds may allow for the conversion price to be adjusted downwards based on stock performance, which could further increase the dilutive effect.

- •Market Uncertainty: The overhang of a large block of potential new shares can create uncertainty, potentially capping short-term stock price appreciation as the market anticipates future conversion.

Outlook and Strategic Recommendations for Investors

The private equity investment in LB SEMICON is a net positive for short-term stability but introduces long-term variables. Investors should adopt a cautious but optimistic long-term perspective. Success will not be determined by this deal alone, but by how the company leverages this opportunity to fix its underlying fundamentals. For more on this sector, review our complete guide to analyzing semiconductor stocks.

Monitor these key areas closely:

- •Path to Profitability: Watch for improvements in operating margins and a reduction in net losses in upcoming quarterly reports.

- •Inventory Levels: A reduction in the high inventory assets is critical for improving cash flow and efficiency.

- •Advanced Packaging Wins: Look for news of new contracts or progress in the high-growth AI and automotive semiconductor markets.

- •Bond Conversion News: Stay informed about any announcements regarding the timing and price of the convertible bond conversions.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. All investment decisions should be made with personal discretion and responsibility.

Leave a Reply