The latest SK Bioscience earnings report for the third quarter of 2025 has sent a mixed but intriguing signal to the market. On November 3, 2025, the company announced preliminary results showing a slight miss on revenue but a remarkable improvement in profitability, achieving a net profit turnaround. This detailed SK Bioscience analysis will dissect these figures, explore the fundamental drivers, and provide a comprehensive outlook on the SK Bioscience stock for potential investors.

Does this represent a genuine inflection point for the company, or are there underlying challenges that warrant caution? For anyone considering an SK Bioscience investment, understanding the nuances of this report is critical.

SK Bioscience Q3 2025 Earnings: The Official Numbers

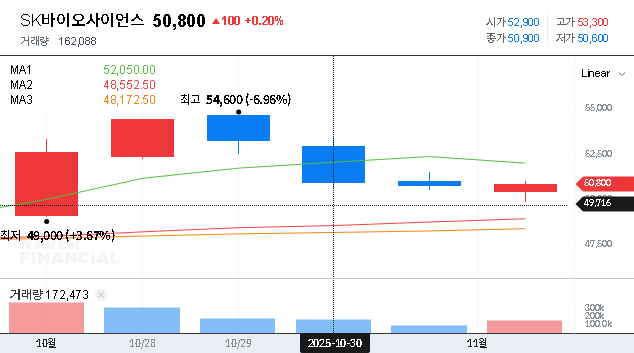

SK Bioscience reported its preliminary consolidated financial results for Q3 2025, which presented a complex picture. While top-line growth was slightly below consensus, the bottom-line performance significantly exceeded expectations. You can view the complete filing here: Official Disclosure (DART).

- •Revenue: KRW 150.8 billion (missing the market expectation of KRW 157.3 billion by 4.1%).

- •Operating Loss: KRW 19.4 billion (a significant 45.3% improvement over the expected loss of KRW 35.5 billion).

- •Net Profit: KRW 24.5 billion (a successful turnaround to profitability, marking a key positive highlight).

The key takeaway is the divergence between revenue and profit. This suggests effective cost management, a favorable product mix, or other efficiency gains are beginning to bear fruit, even as top-line growth remains a challenge.

Core Business Analysis: CDMO Strength and R&D Pipeline

The CDMO Engine and IDT Biologika Acquisition

The Contract Development and Manufacturing Organization (CDMO) segment remains the backbone of SK Bioscience’s revenue, accounting for nearly 79% of its total. The strategic acquisition of German-based IDT Biologika has solidified the company’s position as a major global player. This move not only expands manufacturing capacity but also provides access to a new client base and advanced technologies. With the global CDMO market projected to grow at a compound annual growth rate (CAGR) of 14% through 2030, according to industry reports from sources like Grand View Research, this segment is a critical long-term growth driver.

Future Growth: The Vaccine Pipeline

While the COVID-19 vaccine business has normalized, SK Bioscience is heavily investing in its future pipeline. Key projects that could shape future SK Bioscience earnings include:

- •Next-Generation Pneumococcal Vaccine (GBP410): Currently in Phase 3 clinical trials, this vaccine targets a massive and stable market.

- •mRNA Vaccine Platform (GBP560): Now in Phase 1/2 trials, this platform represents the next frontier in vaccine technology and could open up numerous opportunities.

- •Sanofi Partnership: The co-distribution of vaccines like ‘Bexartus’ and ‘Avaxim’ diversifies the product portfolio and strengthens commercial capabilities.

However, these are long-term plays. The company’s R&D expenses remain high, at 21.5% of revenue in H1 2025, which pressures short-term profitability but is essential for securing future growth. For more information on vaccine development, see our article on The Future of Vaccine Technology.

SK Bioscience is at a crucial juncture. The Q3 2025 results show a company successfully managing costs and leveraging its CDMO strength while investing heavily in a future beyond COVID-19. The market is now watching for signs of sustainable revenue growth to validate this strategy.

SK Bioscience Stock: Investment Outlook & Risk Factors

The Q3 earnings report provides fuel for both bulls and bears. A balanced SK Bioscience analysis requires looking at both sides of the coin.

The Bull Case (Positive Factors)

- •Profitability Turnaround: The dramatic improvement in operating loss and the shift to net profit could signal a bottoming out and attract positive investor sentiment.

- •CDMO Market Leadership: The IDT Biologika acquisition positions SK Bioscience to capitalize on a high-growth, resilient market.

- •Promising Pipeline: Successful commercialization of even one of its late-stage vaccines could be a game-changer for revenue and valuation.

The Bear Case (Negative Factors)

- •Stagnant Revenue Growth: The reliance on the CDMO business and the early stage of the vaccine portfolio create revenue volatility and a lack of clear near-term growth catalysts.

- •Profitability Pressure: High R&D spending and costs associated with integrating IDT Biologika will continue to weigh on operating margins.

- •Macroeconomic Headwinds: Global economic uncertainty, interest rate fluctuations, and currency volatility can negatively impact international operations and stock valuation.

Final Verdict: Cautious Optimism

Our recommendation is one of “Wait and See for Further Confirmation.” The Q3 2025 SK Bioscience earnings are undoubtedly a step in the right direction, showcasing disciplined operational management. The net profit turnaround is a significant psychological victory.

However, for a sustained upward trend in the SK Bioscience stock, the market needs to see evidence of a return to consistent revenue growth. Investors should closely monitor the next few quarterly reports for signs that the top line is recovering and that the improvements in profitability are structural, not just a one-off. A cautious, monitoring approach is the most prudent strategy at this time.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. All investment decisions should be made based on your own research and judgment.

Leave a Reply