Investors are closely evaluating Chong Kun Dang stock following the release of its Q3 2025 provisional earnings. While the headline numbers present a mixed picture, the real story lies deeper within the company’s fundamentals, its promising R&D pipeline, and the macroeconomic headwinds it faces. This comprehensive Chong Kun Dang investment analysis will unpack the latest financial data, explore the game-changing potential of its new drug candidates, and provide a strategic outlook for potential investors.

Does the recent performance signal a buying opportunity, or do underlying risks warrant caution? Let’s dissect the details to form a clear investment thesis.

Deep Dive: Chong Kun Dang Q3 2025 Earnings Breakdown

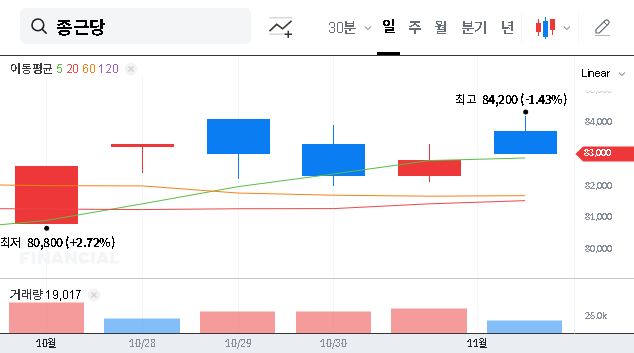

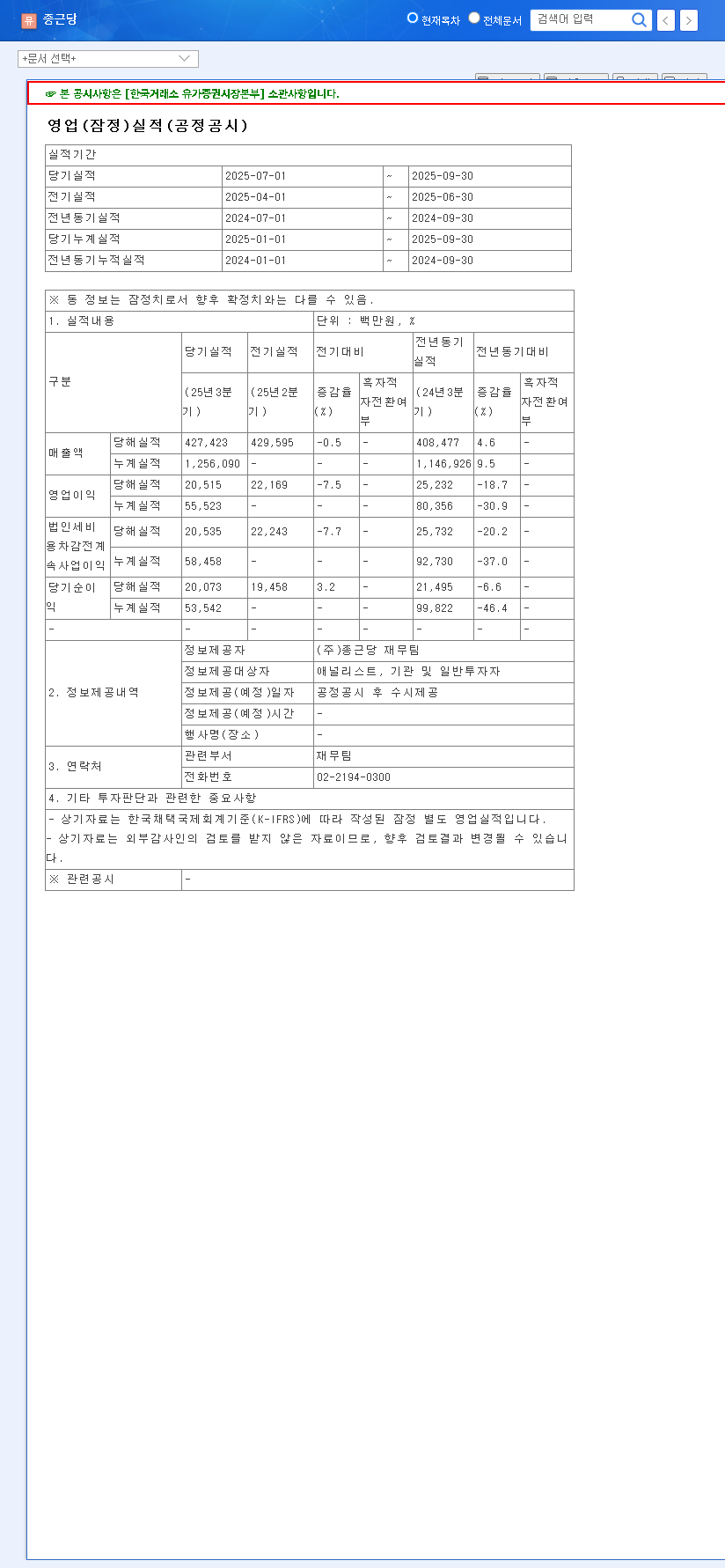

On November 3, 2025, Chong Kun Dang Pharmaceutical Corp. released its provisional operating performance through an Official Disclosure on the DART system. These figures provide a critical snapshot of the company’s recent health.

Key Financial Metrics at a Glance

- •Q3 2025 Revenue: KRW 427.4 billion

- •Q3 2025 Operating Profit: KRW 20.5 billion

- •Q3 2025 Net Income: KRW 20.1 billion

Compared to the prior quarter (Q2 2025), revenue dipped slightly, but both operating profit and net income saw a welcome increase. However, the year-over-year comparison with Q3 2024 tells a different story, with operating profit showing a decrease despite a slight rise in revenue. This suggests potential pressure on profit margins that warrants closer inspection.

Beyond the Headlines: A Fundamental Analysis of Chong Kun Dang Stock

To truly understand the investment potential of Chong Kun Dang stock, we must look beyond a single quarter’s results. The fundamentals reveal a company in transition, balancing heavy investment in the future with present-day challenges.

The Bull Case: R&D and the CKD-510 Game-Changer

The most significant long-term catalyst is the company’s robust R&D pipeline. The CKD-510 technology export deal, valued at an astounding KRW 1.7 trillion, is a massive validation of Chong Kun Dang’s research capabilities. This deal not only promises substantial future revenue streams but also significantly bolsters the company’s financial health and reputation on the global stage. An R&D investment ratio nearing 10% of revenue signals a strong commitment to innovation, which is critical for growth in the competitive pharmaceutical sector. Furthermore, stable sales from key products like Prolia and Atorzet provide a solid foundation for these future-focused investments. For more on industry R&D trends, see this comprehensive report on pharmaceutical innovation.

The Bear Case: Headwinds and Potential Risks

Despite the R&D promise, several risks temper the outlook. The first half of 2025 saw a year-on-year decrease in revenue and profitability, largely due to rising R&D and administrative costs. Other key risks include:

- •Market Competition: The domestic pharmaceutical market in Korea is intensely competitive, putting constant pressure on pricing and market share.

- •Regulatory Hurdles: Government drug pricing policies and ongoing legal disputes, such as the one concerning choline alfoscerate, create significant uncertainty.

- •Operational Cash Flow: A recent shift to negative operating cash flow, coupled with rising inventory levels, requires careful management to ensure financial stability.

These factors are common among many top Korean pharmaceutical stocks, highlighting industry-wide challenges.

The core investment thesis for Chong Kun Dang hinges on whether the long-term potential of its R&D pipeline, particularly CKD-510, can outweigh the short-to-medium term market and regulatory pressures.

Strategic Investment Outlook for Chong Kun Dang

Considering the full picture, a nuanced investment approach is required. The recent improvement in the Chong Kun Dang earnings for Q3 is a positive sign, but the stock price is unlikely to see a sustained surge without clearer resolution of the fundamental risks. The stock has been trading sideways, reflecting this market uncertainty.

For long-term investors, the focus should remain squarely on the clinical progress of CKD-510 and the company’s ability to successfully monetize its technology exports. For short-term traders, a cautious stance is advisable, paying close attention to Q4 earnings guidance and overall market sentiment. Effective risk management, including monitoring legal outcomes and inventory levels, is paramount for any position in Chong Kun Dang stock.

Frequently Asked Questions (FAQ)

What were Chong Kun Dang’s key earnings figures for Q3 2025?

Chong Kun Dang reported Q3 2025 provisional revenue of KRW 427.4 billion, operating profit of KRW 20.5 billion, and net income of KRW 20.1 billion. While profit metrics improved from Q2, they were down compared to the previous year.

Why is the CKD-510 technology deal so important for Chong Kun Dang stock?

The KRW 1.7 trillion CKD-510 deal is a major long-term growth catalyst. It validates the company’s R&D strength, provides a significant future revenue source, and enhances its global competitive standing, making it a cornerstone of the investment case for Chong Kun Dang stock.

What are the main risks to consider before investing?

The primary risks include intense competition in the Korean market, unfavorable government drug pricing policies, unresolved legal disputes, and operational challenges like increased inventory and negative cash flow. These factors create uncertainty for the stock’s performance.

Leave a Reply