ICD Co., Ltd. recently announced a landmark deal, securing a significant ₩9.9 billion manufacturing equipment supply contract with Japan’s renowned Canon Tokki Corporation. This ICD Canon Tokki contract has sent ripples through the investor community, validating ICD’s advanced technology in the FPD (Flat Panel Display) sector and signaling potential for robust revenue growth. However, this positive development is set against a backdrop of persistent financial challenges for the company.

While the deal is a clear vote of confidence, can it single-handedly steer ICD toward profitability and sustainable growth? This article provides a comprehensive ICD financial analysis, dissecting the contract’s implications, the company’s underlying financial health, and the external market risks that investors must consider. Our goal is to equip you with a balanced perspective to inform your investment strategy regarding ICD’s future.

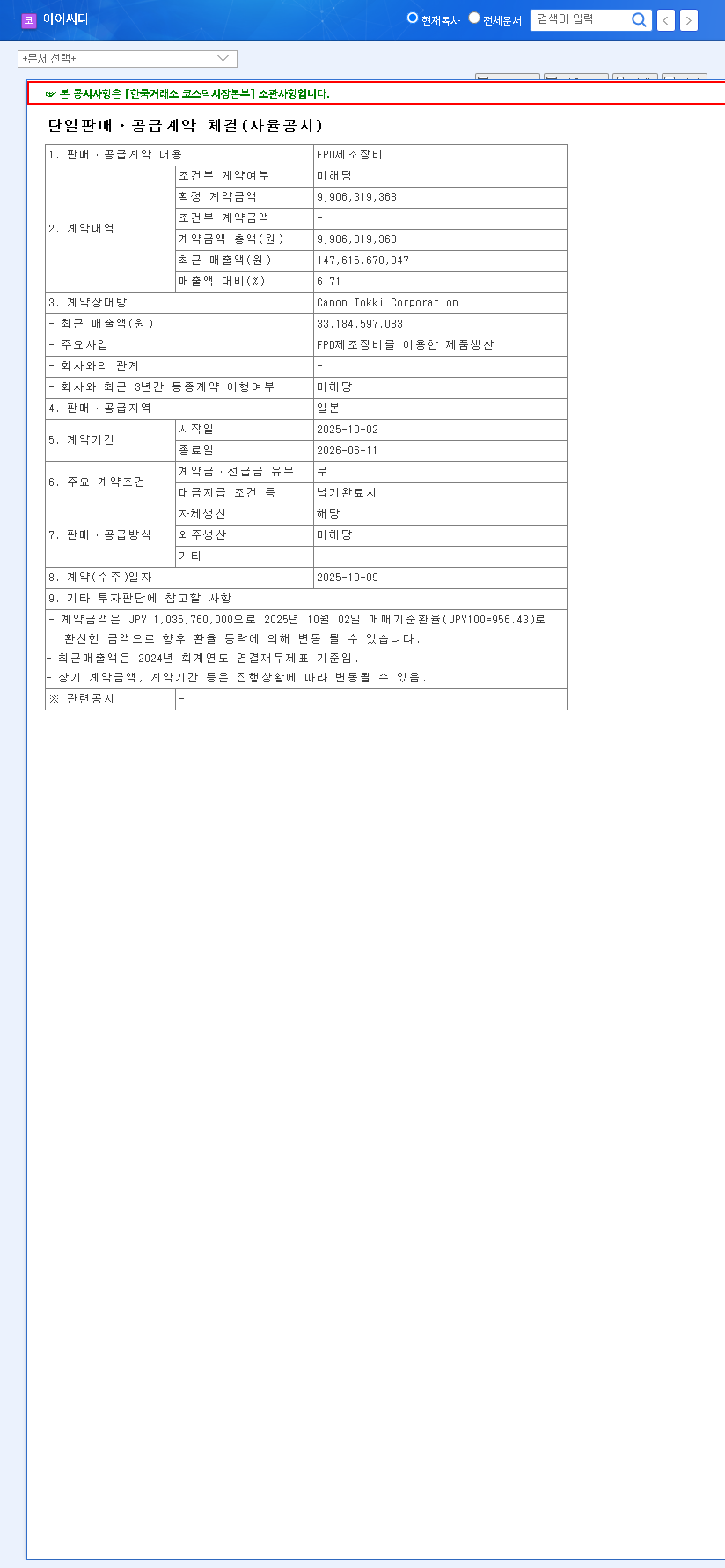

Unpacking the ICD Canon Tokki Contract Details

On October 10, 2025, ICD publicly disclosed a pivotal agreement for the supply of FPD manufacturing equipment. This deal underscores a crucial partnership with Canon Tokki, a global leader and standard-setter in the display manufacturing industry. The specifics of the agreement provide a clear timeline for revenue recognition.

Contract Value: ₩9.9 Billion KRW

Counterparty: Canon Tokki Corporation (Japan)

Contract Period: October 2, 2025 – June 11, 2026 (Approx. 8 months)

Revenue Impact: Represents 6.71% of ICD’s 2024 total revenue

The full details of this agreement were filed and can be reviewed in the Official Disclosure, providing transparency for stakeholders.

The Bull Case: Why This Deal Matters

Validation in a Growing OLED Market

ICD’s core competency lies within the competitive OLED display equipment sector. The global OLED market continues its aggressive expansion, driven by demand for superior displays in smartphones, televisions, and increasingly, automotive systems. As documented by industry reports from sources like leading market research firms, this trend is set to continue. Securing a contract with Canon Tokki, a titan in the Japanese technology landscape, is more than just a sale; it’s a powerful international endorsement of ICD’s technological prowess and product reliability. It builds on previous successes, like the contract with Chengdu BOE, solidifying ICD’s position as a key supplier in the global display chain.

Positive Impact on Revenue and Stock Price

The ₩9.9 billion injection will be recognized over three financial quarters (Q4 2025 – Q2 2026), providing predictable revenue and boosting short-term financial forecasts. This enhanced visibility often resonates positively with the market, potentially providing upward momentum for the ICD stock price. Furthermore, a successful partnership with a prestigious client like Canon Tokki enhances ICD’s reputation, which can be a critical factor in securing future large-scale orders.

The Bear Case: Navigating Significant Financial Headwinds

Despite the celebratory nature of the Canon Tokki news, a prudent ICD financial analysis reveals deep-seated challenges that this single contract cannot entirely resolve.

Persistent Profitability and Debt Concerns

The company’s financial statements tell a cautionary tale. Despite revenue growth in 2024, ICD reported a staggering operating loss of ₩26.7 billion and a net loss of ₩28.3 billion. This indicates that its cost structure, potentially burdened by high fixed costs and R&D expenses, is unsustainable at current levels. Key financial health concerns include:

- •High Debt Ratio: The debt-to-equity ratio has climbed to 97.04%, signaling increased financial risk and leverage.

- •Convertible Bonds: A substantial volume of unredeemed convertible bonds presents a dual threat of rising interest expenses and potential stock dilution for existing shareholders upon conversion.

Macroeconomic and Operational Risks

Beyond its internal financials, ICD must navigate a volatile global economic landscape. Rising interest rates in key markets increase the cost of servicing its debt. Furthermore, fluctuating exchange rates, international oil prices, and logistics costs can erode the profitability of its FPD manufacturing equipment sales. The uncertainty surrounding the final revenue realization from the previously announced Chengdu BOE contract also remains a point of concern for investors seeking clarity.

Investor Action Plan & Final Verdict

The ICD Canon Tokki contract is an undeniable operational victory and a testament to the company’s competitive technology. It provides a welcome short-term boost. However, investors should view it as a positive signal within a broader, more complex financial picture rather than a cure-all solution.

Moving forward, the focus should be on management’s ability to translate this operational success into fundamental financial improvement. Key areas to monitor include:

- •Profitability Strategy: Look for concrete cost-cutting measures and efficiency improvements in quarterly reports.

- •Financial Deleveraging: Monitor plans for managing debt and the overhang from convertible bonds.

- •Transparent Communication: Pay attention to the company’s investor relations for clear updates on contract execution and financial health. To learn more, read our guide on how to analyze a tech company’s balance sheet.

In conclusion, while this contract provides positive momentum, long-term success for ICD hinges on a disciplined return to profitability and financial stability. The market is watching, and the next few quarters will be critical.

Leave a Reply