The recent announcement of UTI’s significant ₩11.2 billion investment into the UTI foldable cover glass market has sent ripples through the investment community. By acquiring a subsidiary in Vietnam, UTI is making a high-stakes play for a dominant position in a next-generation technology sector. However, this ambitious move comes at a time when the company’s financial health is precarious, as revealed by its H1 2025 report. This creates a critical question for stakeholders: is this a visionary step toward long-term growth, or a reckless gamble that could jeopardize the company’s short-term survival? This comprehensive analysis will dissect the investment, evaluate the latest UTI financial analysis, and outline a prudent strategy for investors.

Unpacking the ₩11.2 Billion UTI Investment

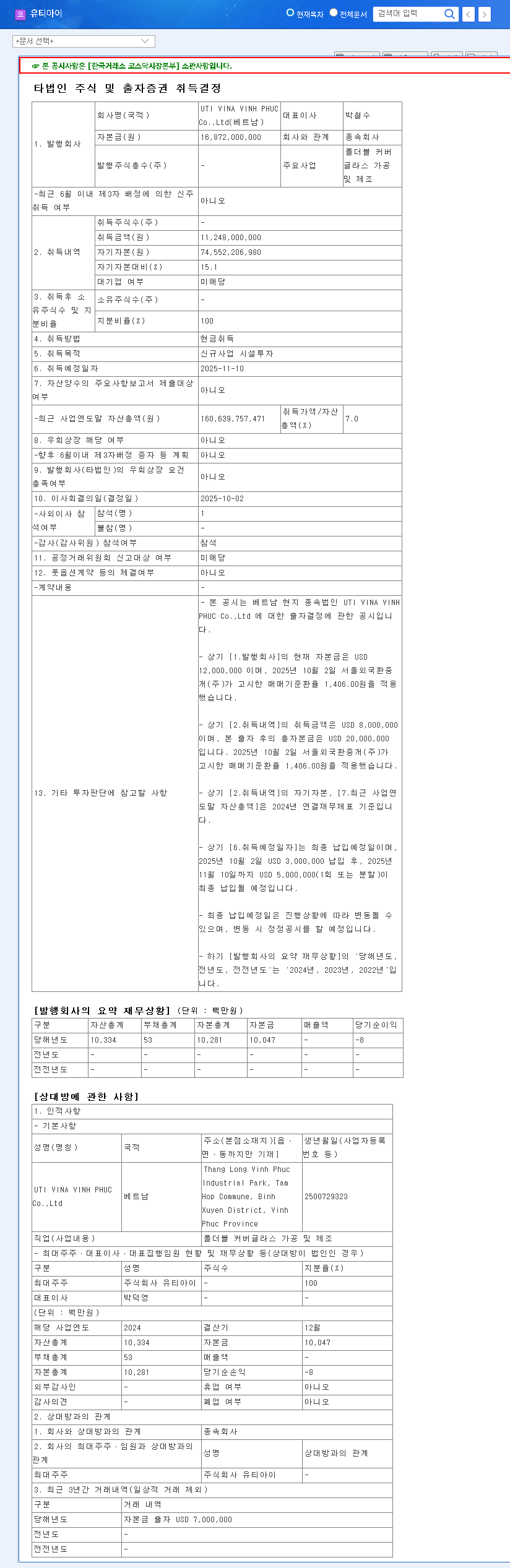

On November 10, 2025, UTI is scheduled to complete its acquisition of 100% of UTI VINA VINH PHUC Co., Ltd in Vietnam. This strategic move, detailed in an Official Disclosure, represents a major pivot for the company. The core purpose is to establish a dedicated facility for processing and manufacturing foldable cover glass, a critical component for the burgeoning foldable smartphone and device market. The key details of this UTI investment are as follows:

- •Acquired Entity: UTI VINA VINH PHUC Co.,Ltd (Vietnam)

- •Core Business: Foldable Cover Glass Processing & Manufacturing

- •Acquisition Amount: ₩11.2 Billion (representing 15.1% of equity)

- •Strategic Goal: Secure future growth engines and diversify revenue streams.

A Company Under Pressure: UTI Financial Analysis (H1 2025)

The timing of this large-scale investment is alarming when contextualized by UTI’s recent performance. The H1 2025 report paints a picture of a company facing severe financial headwinds, making this new venture in Vietnam cover glass manufacturing a significant risk.

With a debt-to-equity ratio soaring past 215% and cash reserves plummeting, UTI is funding future growth by stretching its present-day finances to the absolute limit.

Revenue Collapse and Deepening Losses

UTI’s core business segments are struggling. The Camera Window division saw sales plummet by nearly 60% year-over-year due to a slowdown in the smartphone market and intense competition. While the ‘Slimming’ business showed nascent growth, it was not nearly enough to offset the broader decline. This culminated in a consolidated operating loss of ₩19.2 billion and a net loss of ₩20.4 billion for the first half of 2025.

Soaring Debt and Liquidity Crisis

The company’s balance sheet is a major cause for concern. Total liabilities have ballooned to ₩101.5 billion, driven by the issuance of convertible bonds. This has pushed the debt-to-equity ratio to a staggering 215.19%. Even more critically, cash and cash equivalents have dwindled from ₩54 billion to just ₩10.8 billion. The current ratio stands at a perilous 43.99%, signaling a severe short-term liquidity crunch that makes an ₩11.2 billion cash outlay for the UTI VINA VINH PHUC acquisition exceptionally risky. You can learn more about navigating high-debt companies in our guide.

Opportunity vs. Risk: The Future of the UTI Foldable Cover Glass Bet

The Bull Case: Securing a High-Growth Future

Despite the financial strain, the logic behind the UTI foldable cover glass investment is clear. The market for foldable devices is projected to grow exponentially. According to market analysts at IDC, shipments are expected to double within the next few years. By establishing a production base in Vietnam, UTI can leverage lower operating costs, enhance its global price competitiveness, and position itself as a key supplier in this lucrative value chain. Success in this venture could completely transform the company’s growth trajectory and lead to significant long-term returns.

The Bear Case: A Burden Too Heavy to Carry?

The negative aspects are immediate and severe. The ₩11.2 billion cash outflow will further cripple the company’s liquidity, potentially forcing it to seek additional, and likely expensive, financing. Furthermore, new manufacturing operations require significant ramp-up time and capital expenditure before they become profitable. In the short term, this will likely expand UTI’s deficit. There’s a tangible risk that the new business will not scale quickly enough to offset the continued decline in its legacy segments, creating a perfect storm of financial distress.

Investor Strategy: Navigating UTI’s High-Stakes Future

For current and prospective investors, a cautious and highly diligent approach is paramount. The potential upside of the UTI investment is matched only by its considerable downside. Monitoring the following key areas is essential:

- •Monitor New Business Performance: Closely track tangible results from the Vietnam facility, including production yields, initial client contracts, revenue generation, and profit margins.

- •Scrutinize Financial Health Initiatives: Verify the company’s plans for funding the investment and managing existing debt. Look for concrete strategies to improve cash flow and restore liquidity.

- •Evaluate Core Business Recovery: Assess whether the legacy camera window business can stabilize and if the Slimming business can accelerate its growth to provide a more stable foundation.

- •Stay Abreast of Macroeconomic Factors: Keep an eye on exchange rates (KRW/USD) and the overall health of the IT market, as these will directly impact UTI’s costs and revenues.

In conclusion, UTI’s move into the UTI foldable cover glass sector is a classic high-risk, high-reward scenario. While the company is commendably investing in its future, the precariousness of its current financial state cannot be ignored. A prudent investment decision requires a deep understanding of both the immense growth potential and the significant, immediate financial dangers.

Leave a Reply