The market is buzzing with speculation surrounding the potential Doosan SK Siltron acquisition, a move that could fundamentally reshape Doosan Corporation’s future. A recent report ignited a firestorm of investor interest, sending Doosan Corp stock soaring and leaving many to wonder if this is a strategic masterstroke or a high-stakes gamble. This potential deal positions Doosan at the heart of the booming semiconductor industry, but it also comes with significant financial and integration challenges.

This comprehensive analysis will delve into the short-term and long-term implications of this rumored acquisition. We will explore the strategic value of SK Siltron, assess Doosan’s financial capacity to execute such a large-scale purchase, and weigh the potential rewards against the inherent risks. For investors navigating this period of high volatility, we offer a clear-eyed perspective to help inform your next steps.

The Spark: How the Acquisition Rumors Ignited the Market

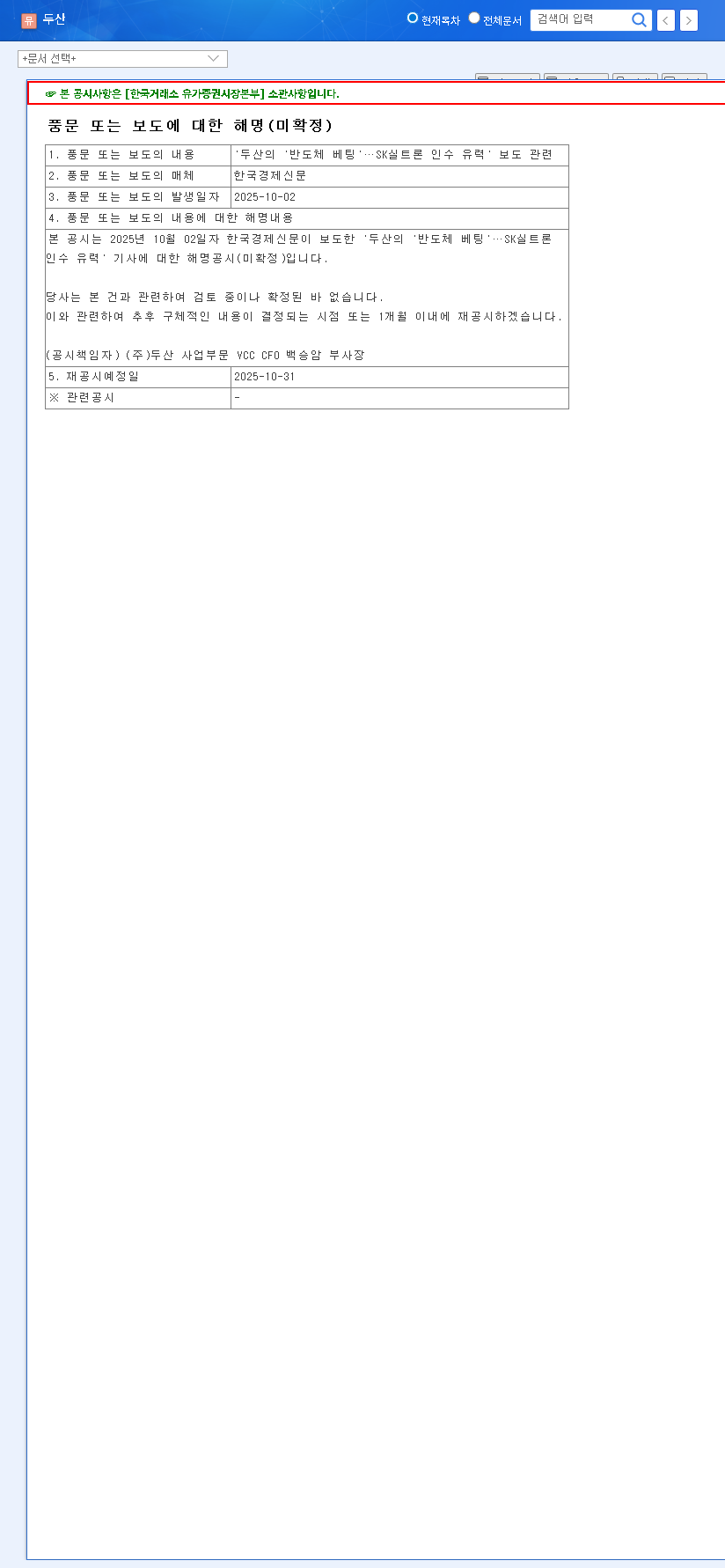

On October 2, 2025, a pivotal report from the Korea Economic Daily titled, “Doosan’s ‘Semiconductor Bet’…SK Siltron Acquisition Likely,” acted as a catalyst, causing a dramatic surge in Doosan Corp.’s stock price. The market’s reaction was swift and decisive, reflecting immense optimism about the company’s potential pivot towards high-tech manufacturing. In response, Doosan Corp. issued a regulatory disclosure to temper expectations, stating, “We are reviewing this matter, but nothing has been confirmed.” This statement was accompanied by an Official Disclosure, providing transparency. However, the promise of a re-disclosure by October 31 has kept anticipation high, fueling continued speculation.

Why SK Siltron is a Coveted Asset

The market’s excitement is not unfounded. Acquiring SK Siltron would be a transformative event for Doosan, providing an entry into the highly profitable and strategically critical semiconductor wafer market. To understand the significance, we must first look at SK Siltron’s role in the global tech ecosystem.

A Global Leader in a Critical Industry

SK Siltron is a global powerhouse in the manufacturing of silicon wafers, the foundational material upon which virtually all microchips are built. As the demand for advanced semiconductors skyrockets—driven by AI, high-performance computing, and IoT—the value of premier wafer suppliers like SK Siltron has escalated dramatically. These are not mere components; they are the bedrock of the digital economy.

By acquiring a key player in the global semiconductor industry, Doosan would not just be buying a company; it would be securing a vital position in the future of technology and securing a new engine for Doosan Corp growth.

Synergy with Doosan’s Existing Portfolio

Doosan is no stranger to the electronics sector. The company has a history in semiconductor substrate materials through its former Electronic BG (Business Group), which focused on products like copper-clad laminates (CCL). A successful Doosan SK Siltron acquisition would create powerful synergies, allowing the company to re-leverage its expertise and strengthen its position across the entire semiconductor value chain, from raw materials to advanced components.

Weighing the Financials: Can Doosan Afford This Bet?

A deal of this magnitude naturally raises questions about financial feasibility. The acquisition cost for SK Siltron is expected to be substantial, placing Doosan Corp.’s balance sheet under intense scrutiny. Let’s examine the pros and cons.

- •Potential Financial Burden: A large acquisition could significantly increase Doosan’s debt load and interest expenses, potentially straining its financial health in the short term.

- •Signs of Financial Flexibility: On the other hand, Doosan exhibits strong financial fundamentals. Its low P/E ratio (4.47x), exceptionally high retained earnings (2,488.17%), and a manageable consolidated debt-to-equity ratio (21.38%) suggest it has the capacity to structure a financing deal without over-leveraging.

- •Acquisition Uncertainty: The deal is far from certain. The process could face competitive bidding, and failure to complete the acquisition could lead to a sharp correction in the Doosan Corp stock price.

- •Post-Merger Integration (PMI) Risks: Even if successful, integrating two large organizations presents significant challenges. Cultural clashes and operational friction could delay the realization of expected synergies.

Conclusion: A Pivotal Moment for Investors

The potential Doosan SK Siltron acquisition is a watershed moment for the company. If successful, it promises to unlock immense long-term value and reposition Doosan as a key player in a high-growth industry. However, the path is fraught with financial risks and execution uncertainty.

For investors, the key is to remain vigilant and informed. The current stock price surge is based on optimism and expectation. The reality will depend on the final terms of the deal, the financing structure, and the company’s post-merger integration plan. It’s essential to develop a long-term investment strategy that accounts for both the massive upside and the significant risks involved.

The most critical action is to watch for the re-disclosure scheduled by October 31. This announcement will provide the concrete details needed to move from speculation to informed decision-making.

Frequently Asked Questions (FAQ)

Is the Doosan SK Siltron acquisition confirmed?

No. As of now, it is a rumor based on a media report. Doosan Corp. has officially stated the matter is under review but unconfirmed. A definitive answer is expected by the re-disclosure deadline of October 31, 2025.

What is the biggest benefit for Doosan Corp?

The primary benefit would be securing a new, high-growth engine by entering the thriving semiconductor wafer market. This would diversify Doosan’s portfolio and position it for significant long-term profitability and corporate value appreciation.

What are the main risks involved in this deal?

The key risks include the substantial financial burden of the acquisition, the uncertainty of the deal’s success, the complexities of integrating SK Siltron’s business and culture, and the inherent volatility of the global semiconductor market.

What should investors do now?

A cautious approach is advised. The current surge in Doosan Corp stock is speculative. Investors should wait for the official re-disclosure on or before October 31 to understand the specific terms, financing, and strategic plan before making any investment decisions.

Leave a Reply