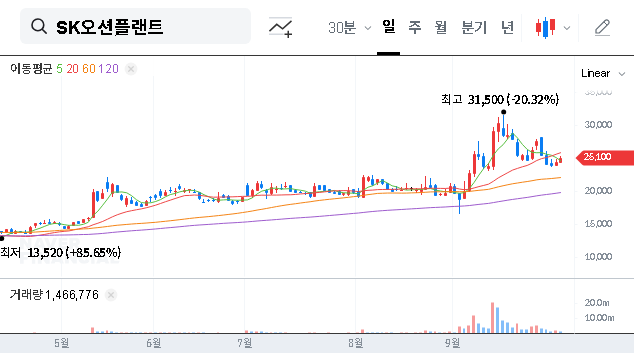

When South Korea’s largest institutional investor makes a move, the market pays attention. News recently broke that the National Pension Service (NPS) has increased its stake in SK Oceanplant (100090), signaling a significant vote of confidence. But does this automatically make SK Oceanplant stock a strong buy? For savvy investors, this is not just a headline; it’s a prompt for a deeper investigation.

This comprehensive analysis will dissect what the NPS’s investment means, evaluate the underlying health of SK Oceanplant, and navigate the complex macroeconomic landscape to provide a clear investment outlook. We’ll explore the fundamentals, risks, and potential rewards to help you make an informed decision.

The Catalyst: National Pension Service Increases Its Holding

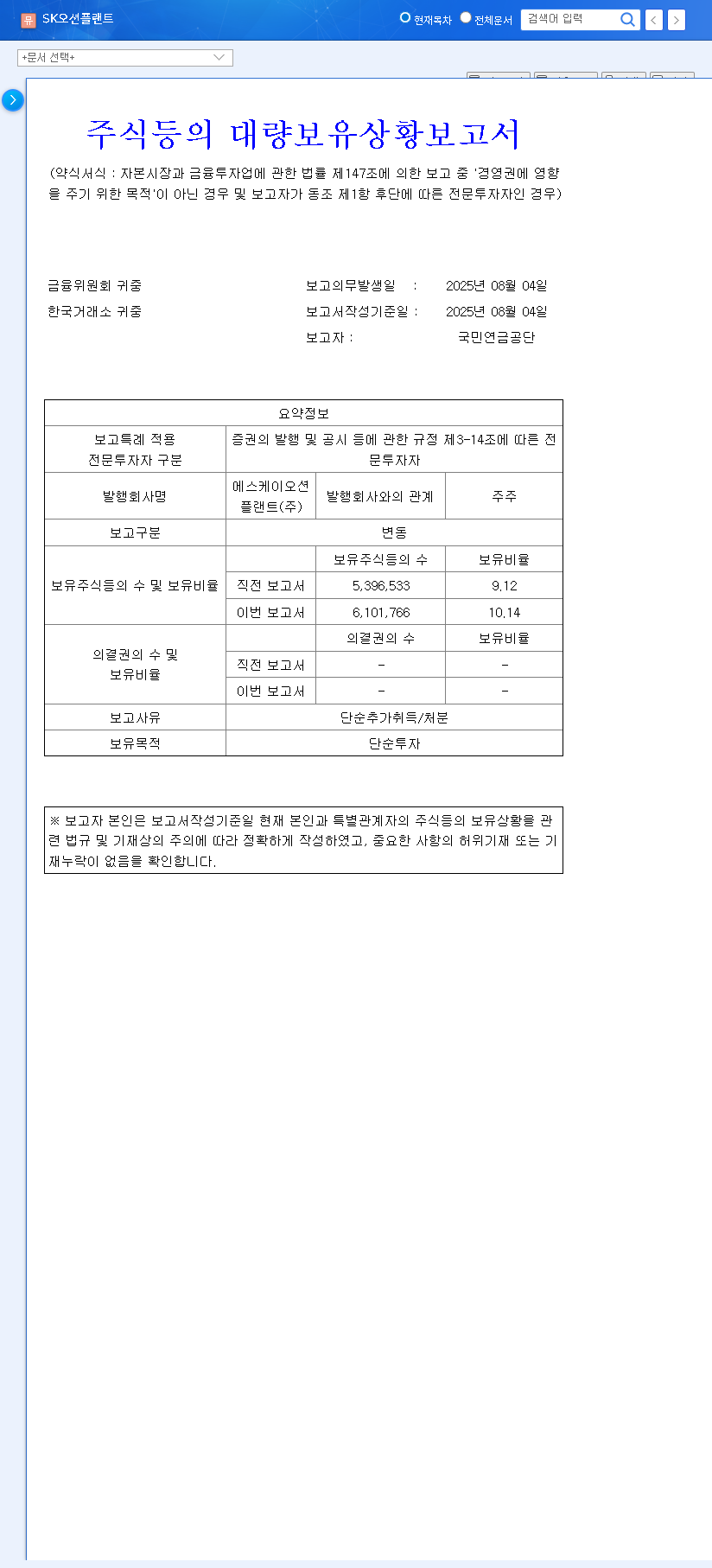

On October 1, 2025, a significant filing revealed that the National Pension Service of Korea increased its ownership in SK Oceanplant from 9.12% to 10.14%. While the stated purpose is for ‘simple investment,’ the action itself speaks volumes. An institution of this magnitude, managing the nation’s retirement funds, does not make such decisions lightly. This move suggests a belief in the company’s long-term value proposition and growth potential.

An increased stake from a major institutional investor like the NPS is often interpreted as a strong positive signal, reflecting confidence in a company’s future trajectory and management, independent of short-term market noise.

Investors can view the official report directly from the source. This transparency is crucial for due diligence. Official Disclosure: Click to view DART report.

Fundamental Analysis: A Look Under the Hood of SK Oceanplant

While the NPS news is a bullish signal, the company’s financials present a mixed picture that requires careful consideration. A recent business report restatement has enhanced transparency, which is a positive step toward building investor trust. However, the projected performance for 2024 raises some questions.

Key Financial Indicators (2022-2024 Projections)

- •Revenue: Expected to rebound to KRW 2,495.8 billion in 2024 after a dip in 2023. This indicates strong top-line demand.

- •Operating Profit: A projected sharp decline to KRW 4.0 billion in 2024 is a major red flag, suggesting significant margin compression or rising operational costs.

- •Net Income & EPS: Both are expected to increase, which may seem contradictory to the operating profit decline. This could be due to non-operational gains or accounting adjustments. For more on this, see our guide on how to analyze an income statement.

- •Debt-to-Equity Ratio: Remaining high at over 700%, this indicates significant leverage and financial risk, which is common but still a concern in capital-intensive industries.

The Macro Environment: Headwinds and Tailwinds

No company operates in a vacuum. The SK Oceanplant stock outlook is heavily influenced by global economic trends. These factors can significantly impact profitability.

Currency, Rates, and Commodities

- •Exchange Rates: A high KRW/USD rate is generally favorable for an exporter like SK Oceanplant, boosting the value of its international sales. However, volatility remains a risk to be monitored.

- •Interest Rates: The trend of falling benchmark rates in the US and Korea is a positive. Lower rates reduce borrowing costs for financing large projects and can improve investor sentiment across the market. Authoritative sources like Bloomberg’s market data show this easing trend.

- •Shipping Indices: A rising Baltic Dirty Tanker Index suggests higher demand for seaborne shipping, a positive for the industry. Conversely, a falling China Containerized Freight Index could signal a slowdown in global trade, presenting a potential headwind.

Investment Strategy & Final Outlook

Synthesizing these factors, the investment case for SK Oceanplant is one of long-term potential balanced by short-term risks. The NPS’s backing provides a strong foundation of confidence, but the concerning operating profit forecast and high debt cannot be ignored.

A prudent strategy would be to adopt a long-term perspective. Instead of anticipating a rapid stock price surge, investors should monitor key performance indicators that will ultimately drive the company’s value.

Key Factors to Watch Going Forward:

- •New Project Orders: The lifeblood of the business. Securing large-scale offshore plant and shipbuilding contracts is the single most important catalyst for growth.

- •Margin Improvement: Watch for signs that the company is getting its operational costs under control and improving profitability on its projects.

- •Deleveraging Efforts: Any progress in reducing the high debt-to-equity ratio will significantly de-risk the stock and improve its financial stability.

Frequently Asked Questions (FAQ)

Q1: Why did the National Pension Service really increase its SK Oceanplant stake?

A1: The official reason is for ‘simple investment.’ This typically means the institution sees the stock as undervalued and expects it to appreciate over the long term. It’s a vote of confidence in the fundamental value and future growth prospects of SK Oceanplant.

Q2: What is the biggest short-term risk for SK Oceanplant stock?

A2: The biggest immediate risk is the projected collapse in operating profit for 2024. If the company fails to manage costs and improve margins, it could put significant pressure on the 100090 stock price, regardless of revenue growth.

Q3: Is SK Oceanplant a good investment now?

A3: It appears to be a better fit for long-term, patient investors. While the NPS endorsement is powerful, the financial red flags (low operating profit, high debt) require caution. Success hinges on future contract wins and improved financial management.

Leave a Reply