In a significant market development, the National Pension Service (NPS) of South Korea has officially disclosed a 5.00% stake in Taekwang, a specialized plant equipment manufacturer. This move, executed for ‘simple investment’ purposes, has sent ripples through the financial community. For investors, the critical question is clear: Is the acquisition of the NPS Taekwang stake a powerful endorsement of the company’s future, or simply a routine portfolio diversification? This comprehensive Taekwang investment analysis will dissect the disclosure, evaluate the company’s fundamentals, and outline a strategic path forward for potential and current shareholders.

The Official Disclosure: NPS Acquires 5% Stake in Taekwang

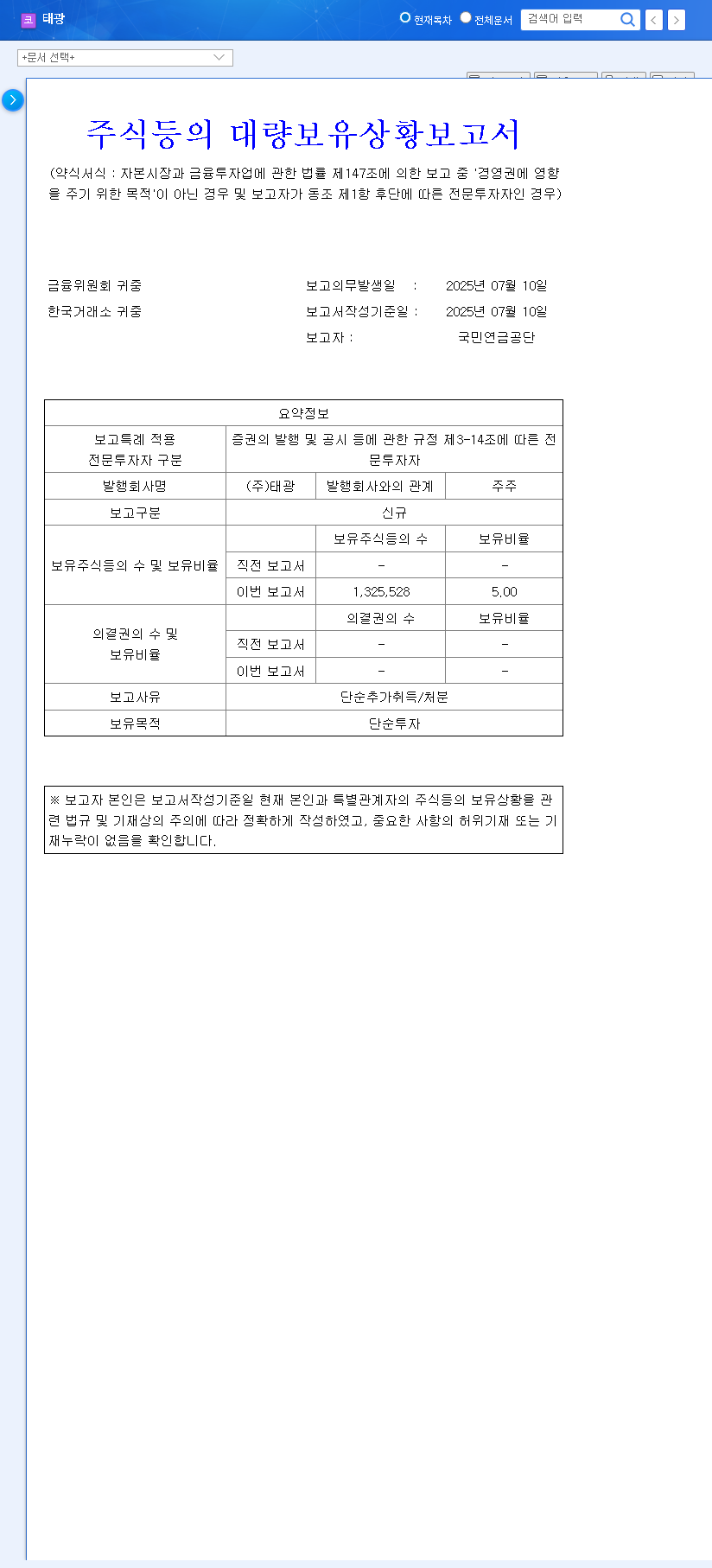

On October 1, 2025, the National Pension Service formally announced its 5.00% ownership in Taekwang via a ‘Report on the Status of Large-Volume Holdings of Shares.’ This was filed as a ‘simple investment,’ which typically indicates the investor does not intend to influence company management directly. The news is particularly noteworthy given Taekwang’s market capitalization of 738 billion KRW at the time. The investment by the nation’s largest and most influential institutional investor is a powerful signal that warrants close examination. The full details can be reviewed in the Official Disclosure (DART Source).

When an institution like the NPS makes a move, the market listens. Their acquisition is often seen as a seal of approval, signaling deep research and confidence in a company’s long-term value proposition.

Analyzing the Impact of the NPS Taekwang Stake

The involvement of the National Pension Service is more than just a large transaction; it’s a statement of institutional confidence. This can trigger what is known as the ‘NPS effect,’ where retail and other institutional investors follow suit, creating positive stock price momentum. Such an endorsement suggests that Taekwang’s projected financial improvements and strategic direction have passed the rigorous due diligence of a major market player. For more context on how markets react to such news, investors often consult analysis from high-authority sources like Bloomberg.

Positive Catalyst: Strong Financial Projections for 2025

A core reason for the NPS’s interest likely lies in Taekwang’s promising financial turnaround. Projections for 2025 paint a picture of robust recovery and growth, marking a significant shift from previous years.

- •Profitability Turnaround: Operating profit is projected to reach 23.7 billion KRW, a dramatic recovery from a loss of -9.9 billion KRW in 2022. The operating profit margin is expected to hit a healthy 10.11%.

- •Revenue Growth: Revenue is forecast to climb to 233.9 billion KRW, demonstrating steady top-line expansion.

- •Shareholder Value: Earnings Per Share (EPS) are anticipated to surge to 2,268 KRW, with a corresponding Return on Equity (ROE) of 8.49%.

- •Financial Stability: The company is expected to maintain a stable debt-to-equity ratio of just 25.82%, indicating a solid balance sheet.

Key Concerns and Potential Risks

Despite the positive outlook, a thorough Taekwang investment analysis must consider the challenges. The underperformance of key subsidiaries, particularly HYTC Co., Ltd. in the secondary battery equipment sector, is a significant drag. Despite a booming market, HYTC has seen its revenue and profits decline due to fierce competition and investment volatility from clients. Furthermore, the company’s negligible R&D spending over the past five years raises serious questions about its ability to innovate and secure long-term competitive advantages. Macroeconomic factors like interest rate fluctuations also remain a persistent threat.

Actionable Investment Strategy for Taekwang Stock

Given the mix of strong tailwinds and notable headwinds, investors should adopt a multi-faceted strategy. Understanding the nuances of large-scale purchases is key; for more on this, review our guide to interpreting institutional stock purchases.

Short-Term (3-6 Months)

In the short term, the NPS Taekwang stake is likely to provide positive momentum. Investors should monitor trading volumes and track whether other institutional investors begin to build positions. Any positive announcements in the next quarterly report could act as a further catalyst.

Mid-to-Long-Term (1-3 Years)

Long-term success hinges on Taekwang addressing its core weaknesses. Key areas to monitor include:

- •Subsidiary Turnaround: Watch for strategic shifts or performance improvements at HYTC Co., Ltd.

- •R&D Investment: Look for concrete plans and capital allocation towards research and development in corporate filings.

- •Profit Margin Sustainability: Verify if the company can sustain and grow its projected 10.11% operating margin in subsequent quarters.

In conclusion, the National Pension Service’s investment is a significant vote of confidence in Taekwang’s recovery story. However, for this to translate into sustainable, long-term shareholder value, the company must resolve its subsidiary issues and commit to innovation. Cautious optimism, backed by diligent monitoring of fundamentals, is the recommended approach.

Leave a Reply