The latest COSMO ADVANCED MATERIALS & TECHNOLOGY CO., LTD earnings report for Q3 2025 sent a significant shockwave through the market. With figures falling drastically short of analyst expectations across the board, investors are now grappling with uncertainty. The report, confirmed by the Official Disclosure on DART, reveals deep-seated challenges in its core business segments.

This comprehensive COSMO stock analysis will dissect the disappointing Q3 2025 results, explore the root causes behind the underperformance, and provide a balanced investment outlook. We’ll examine the immediate impacts and the long-term strategic pivots necessary for the company to navigate the current industry turbulence.

The Q3 2025 Earnings Report: A Staggering Miss

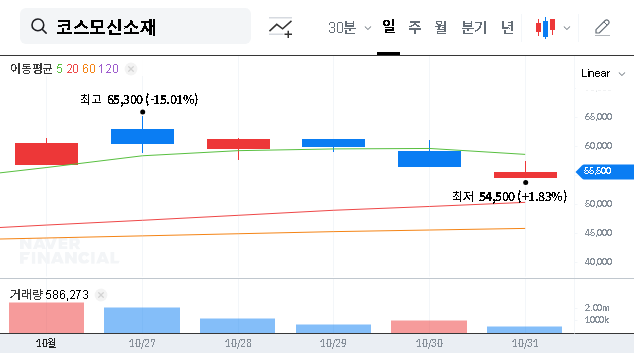

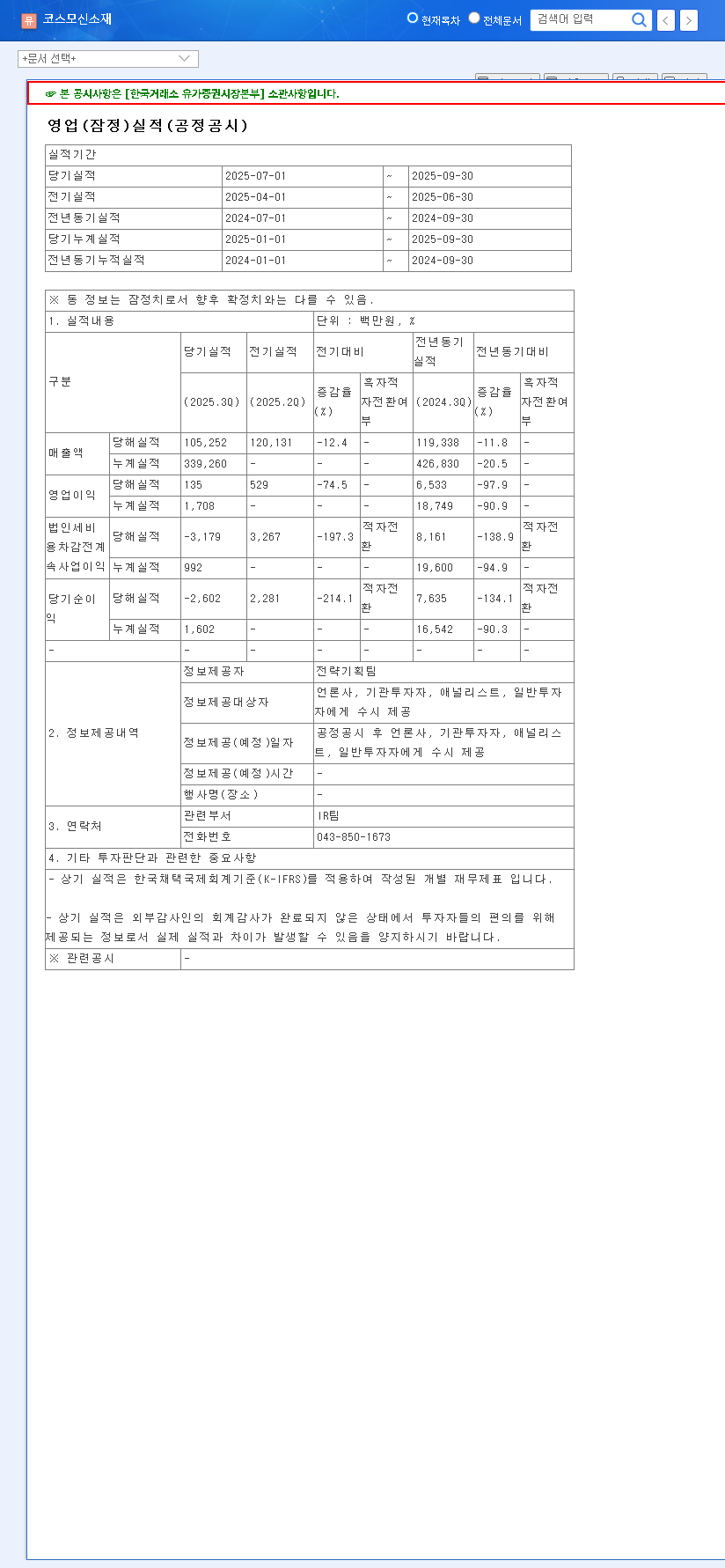

On October 31, 2025, COSMO ADVANCED MATERIALS & TECHNOLOGY CO., LTD released its provisional Q3 earnings, and the numbers painted a grim picture. The performance not only continued the slump from the first half of the year but significantly intensified it.

- •Revenue: 105.3 billion KRW, a 7.0% miss against the 113.7 billion KRW consensus.

- •Operating Profit: A mere 0.1 billion KRW, representing a shocking 83.3% miss compared to the 0.6 billion KRW estimate.

- •Net Profit: A net loss of -2.6 billion KRW, a staggering 750.0% deviation from the estimated profit of 0.4 billion KRW.

The transition to a net loss is the most alarming signal for investors, indicating that operational and market pressures have fully eroded the company’s profitability for the quarter.

Why the Underperformance? Analyzing the Core Issues

The poor COSMO ADVANCED MATERIALS & TECHNOLOGY CO., LTD earnings weren’t caused by a single issue, but a convergence of powerful headwinds in its key markets.

The EV Battery Market ‘Chasm’ Deepens

The primary culprit is the severe downturn in the EV battery cathode material division. This segment suffered from a dramatic fall in sales volume and a factory utilization rate of just 1.62%. This is a direct consequence of the ongoing EV market slowdown, a phenomenon often described as the ‘chasm’. This term, popularized in technology marketing, refers to the difficult transition from selling to early adopters to capturing the mainstream market. High interest rates, insufficient charging infrastructure, and price sensitivity among mainstream consumers are slowing EV adoption rates globally, as detailed in reports by industry analysts like BloombergNEF.

Weakness in Diversified Business Lines

Compounding the EV woes, other business units also faltered. The functional film business saw its revenue plummet by 52.3% year-over-year due to a sharp decline in demand for IT products like smartphones and laptops. Similarly, the legacy toner business continued its structural decline, pressured by office digitalization and intense price competition.

The Q3 results highlight a perfect storm: a cyclical downturn in the high-growth EV sector combined with structural weakness in the company’s legacy businesses.

Investment Outlook: Navigating Risks and Opportunities

Given the severity of the Q3 miss, a cautious and strategic approach is essential. The short-term investment outlook is fraught with challenges, including likely stock price pressure and downward revisions from analysts. However, mid-to-long-term catalysts could change the narrative.

Key Investment Risks

- •Prolonged EV Slump: A longer-than-expected ‘chasm’ phase in the EV market could keep utilization rates critically low.

- •Profitability Drag: The new 80,000-ton NCM cathode material facility, while a long-term asset, represents a significant short-term financial drag without a sharp increase in demand.

- •Macroeconomic Headwinds: Persistently high interest rates and volatile foreign exchange markets could continue to strain financials.

Potential Long-Term Catalysts

- •Strategic NCM Investment: Once the EV market recovers, the new facility positions the company to capitalize on demand for high-performance cathode materials. Learn more about The Future of Battery Technology on our blog.

- •AI Market Exposure: The expansion of functional film lines to serve the burgeoning AI hardware market could become a significant new growth driver, offsetting declines in traditional IT.

- •Product Innovation: Successful development of next-gen products like Mid-Ni, High-Ni, or precursor-free cathode materials could provide a strong competitive edge.

Final Verdict: A ‘Neutral’ Stance with Vigilance

The disappointing COSMO Q3 2025 results warrant a ‘Neutral’ investment opinion. The risks are clear and present, and a turnaround is not imminent. Investors should wait for concrete signs of fundamental improvement before considering a position. Key metrics to monitor in upcoming quarters include an uptick in the cathode division’s utilization rate, stabilization in the functional film segment, and any new customer wins that signal a recovery in demand. Until then, caution is the most prudent strategy.

Leave a Reply