The latest Inzisoft Q3 2025 earnings report has sent ripples through the investment community, presenting a complex and seemingly contradictory financial picture. While core metrics like revenue and operating profit experienced a significant downturn, net income soared, leaving many to question the company’s true health. This report unpacks these confusing numbers, providing a detailed Inzisoft financial analysis to help investors navigate the short-term turbulence and evaluate the long-term potential.

Is this an ‘earnings shock’ signaling deeper issues, or a temporary blip for a company with solid fundamentals? Let’s dive into the data to uncover the story behind the figures and what they mean for the Inzisoft stock outlook.

Unpacking the Q3 2025 Preliminary Results

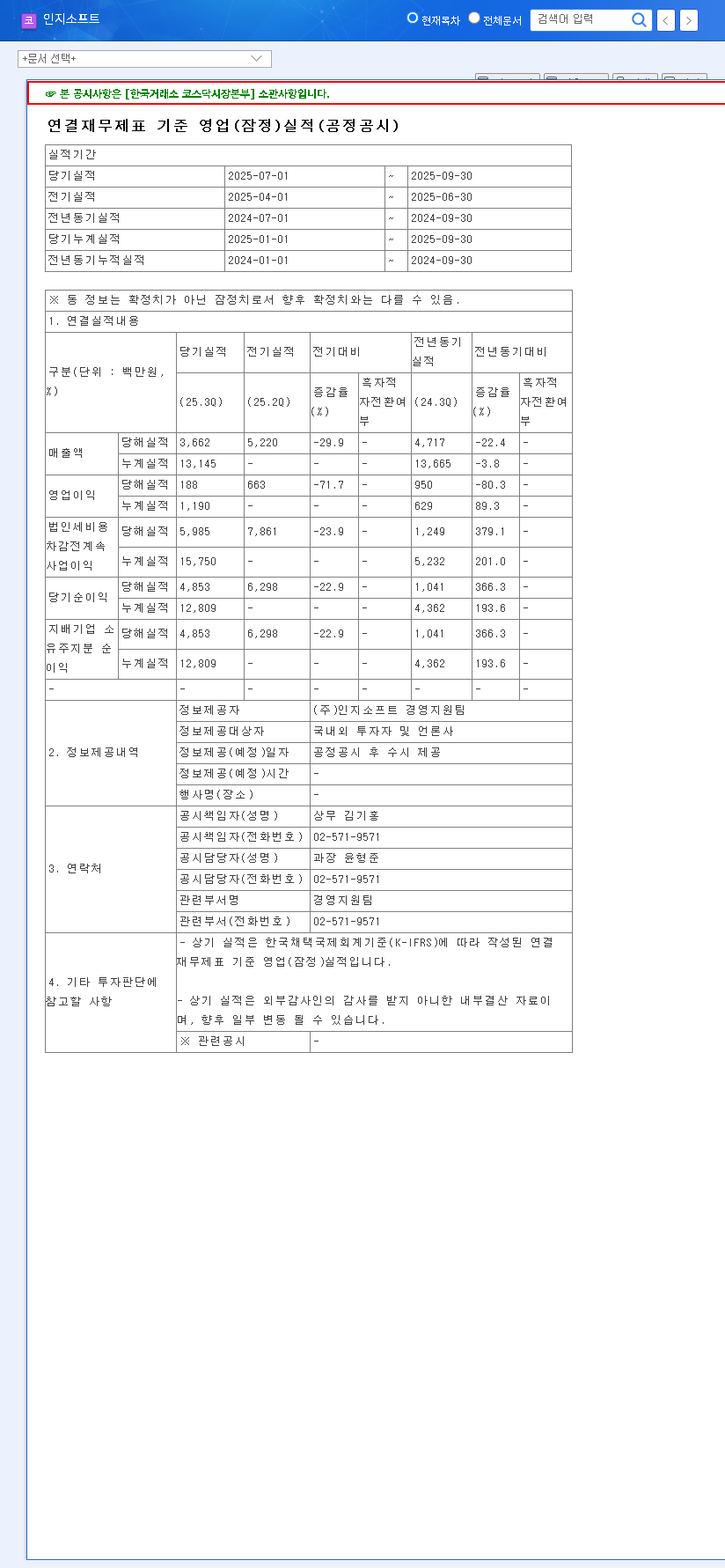

Inzisoft Co., Ltd. announced its preliminary consolidated financial results for the third quarter of 2025, revealing a stark contrast between its operational performance and bottom-line profit. The key figures reported were a revenue of KRW 3.7 billion and an operating profit of just KRW 0.2 billion. Simultaneously, net income reached an impressive KRW 4.9 billion. This divergence demands a closer examination.

An Alarming Decline in Core Operations

The top-line numbers paint a concerning picture. Revenue saw a 28.8% decrease from the previous quarter, while operating profit plummeted by a staggering 71.4%. This sharp decline in operating profit, which is the profit from a company’s core business operations, raises immediate red flags about either a sudden drop in demand, rising costs, or inefficiencies in cost management. Compared to the same period last year (Q3 2024), both revenue and operating profit were substantially lower, indicating this isn’t just a sequential dip but a significant year-over-year contraction in core business health.

The Net Income Anomaly: A Non-Operational Boost

The silver lining in the Inzisoft Q3 2025 earnings report was the KRW 4.9 billion in net income. However, this impressive figure does not stem from the company’s main business activities. The report clarifies that this increase is primarily due to non-operating factors, specifically the fair value valuation of financial assets. This means the profit was generated from investments or other financial instruments, not from selling its software or services.

While a high net income is generally positive, its reliance on volatile non-operating factors rather than sustainable core business profits is a critical point of concern for long-term investors. It highlights a potential vulnerability in the company’s earnings structure.

Evaluating the Long-Term Growth Trajectory

Despite the concerning Q3 results, it’s crucial to look beyond a single quarter. Inzisoft’s fundamentals and market position may still hold significant long-term promise. The strong performance in the first half of 2025, where revenue grew 24.2% year-over-year, shows that the company has a recent history of robust growth. This Q3 result could be an outlier rather than the new norm.

A Diversified and Future-Focused Portfolio

Inzisoft’s strength lies in its diverse portfolio of technologies aligned with the ongoing digital transformation in the financial sector. Its offerings are not just relevant; they are critical for modern financial institutions. For a deeper understanding of their technology, you can read our overview of financial IT solutions.

- •AI OCR & RPA: Automating document processing and back-office tasks, a high-growth area.

- •Cloud-Based SaaS (Q-service): Shifting to a recurring revenue model, which offers greater predictability.

- •Digital Branch Systems: Powering the modernization of banking customer experiences.

Furthermore, the company’s commitment to R&D and its significant holding of treasury shares (18.9% of total shares) signal management’s confidence in future growth and its dedication to enhancing shareholder value.

Investor Action Plan: A ‘Neutral’ Stance Advised

Given the conflicting data, a knee-jerk reaction would be unwise. The Inzisoft Q3 2025 earnings report is likely to cause short-term stock price volatility. However, the underlying long-term drivers remain intact. Therefore, a ‘Neutral’ investment opinion is prudent at this time. Investors should carefully monitor several key areas before making a decision.

According to global market trends reported by sources like Reuters, the demand for financial digital transformation remains strong, which bodes well for Inzisoft’s core market. The critical question is whether the Q3 performance issues are temporary or structural.

Key Monitoring Points for Investors:

- •Official Q3 Report Analysis: Scrutinize the final, detailed report for specific reasons behind the operating profit collapse. Was it a one-time expense or a lasting issue? For direct information, refer to the Official Disclosure on DART.

- •Q4 Outlook & Guidance: Pay close attention to the company’s guidance for the upcoming quarter. Any sign of a rebound in core business profitability will be a key bullish signal.

- •New Business Traction: Look for concrete performance data on their SaaS and AI OCR initiatives. Tangible revenue growth in these areas will validate the long-term strategy.

- •Litigation Updates: Keep an eye on the outcomes of any ongoing legal cases, as they represent a potential financial risk.

In conclusion, while the headline numbers from the Inzisoft Q3 2025 earnings are jarring, a patient and analytical approach is required. The company’s future hinges on its ability to prove that its core operations can return to a growth trajectory and are not permanently impaired. The next few months will be critical in revealing whether Q3 was an anomaly or a new reality.

Leave a Reply