As November 3, 2025, approaches, all eyes in the investment community are on the upcoming HANWHA SYSTEMS Q3 2025 IR (Investor Relations) conference. This event is more than just an earnings report; it’s a critical moment that will shape market perception and influence the company’s valuation. Hanwha Systems stands at a crossroads, with its formidable defense sector showing robust growth while its ICT division faces significant headwinds. This comprehensive Hanwha Systems analysis will delve into the company’s recent performance, dissect its segmental challenges, and outline the key factors investors must watch. By understanding the intricate balance of growth drivers and investment risks, you can gain the insights needed to make informed decisions regarding Hanwha Systems stock.

The Q3 2025 IR is a pivotal event. Investors will be keenly listening for confirmation of sustained defense-sector momentum and, more importantly, a clear and credible turnaround strategy for the underperforming ICT segment.

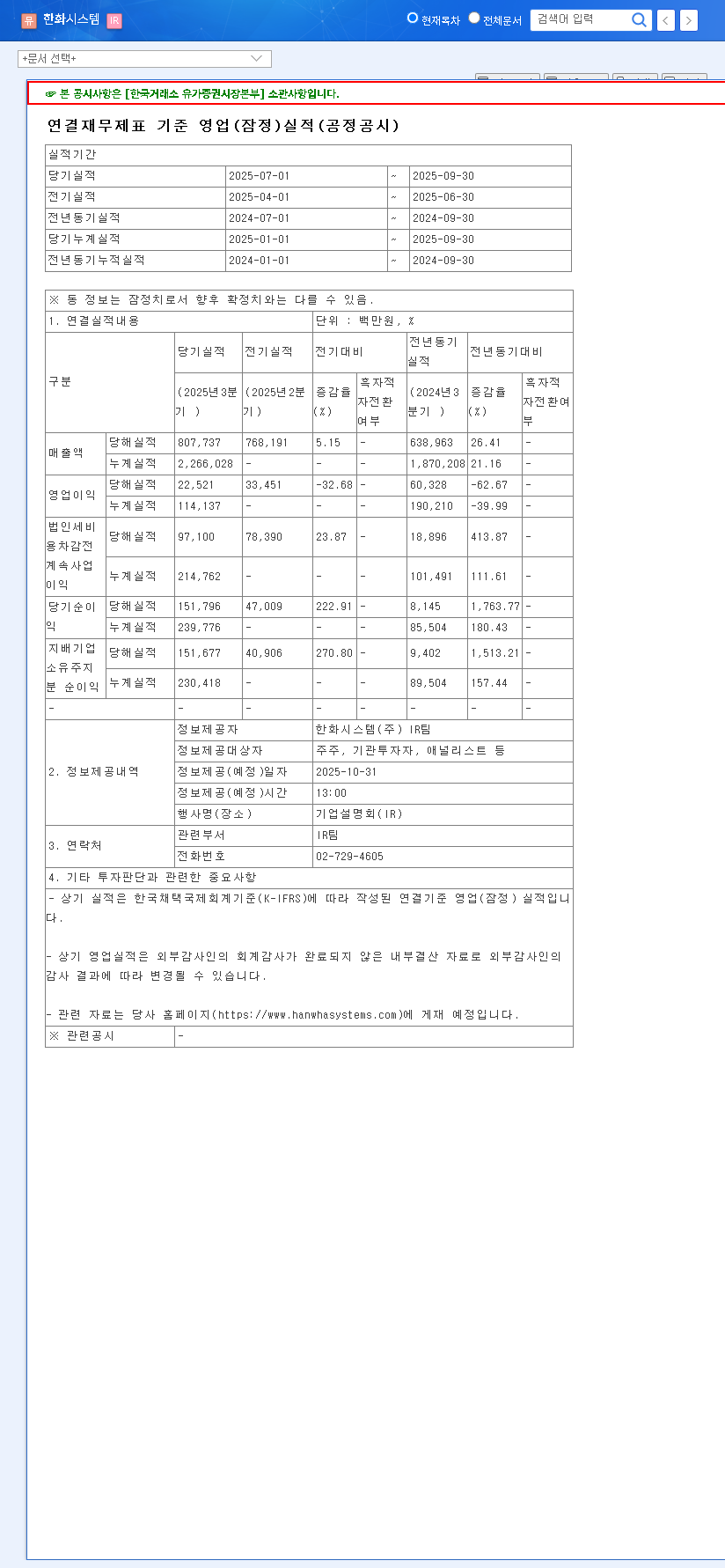

H1 2025 Performance Review: A Tale of Two Segments

The first half of 2025 painted a complex picture for Hanwha Systems. While the company achieved impressive top-line growth, profitability faced significant pressure. According to the company’s Official Disclosure, headline figures reveal a nuanced story.

- •Strong Revenue Growth: Consolidated revenue reached KRW 1.4583 trillion, an 18.4% increase year-on-year, fueled primarily by overseas subsidiaries and new business ventures.

- •Profitability Squeeze: Operating profit saw a sharp decline of 29.8% to KRW 91.6 billion. This was largely due to an expanded operating loss in the ICT sector, which overshadowed profit growth in the defense segment.

- •Surprising Net Income Rise: Despite the operating profit drop, net income grew by 13.7% to KRW 88.0 billion, bolstered by non-operating factors like valuation gains on overseas investment assets.

- •Improved Financial Health: The debt-to-equity ratio improved significantly to 111.33%, and the order backlog swelled by 15.3% to a massive KRW 11.82 trillion, securing a strong future revenue stream.

In-Depth Segment Analysis

The Defense Sector: A Pillar of Strength

Hanwha Systems’ defense sector remains the bedrock of its stability and growth. With revenues of KRW 900.5 billion in H1, it continues to benefit from increasing global defense spending and geopolitical tensions. The company’s competitive edge is sharpened by its investment in next-generation technologies like advanced AESA radar systems and satellite communications. The robust order backlog suggests that this segment will continue to be a primary earnings driver. The key question for the HANWHA SYSTEMS Q3 2025 IR will be the scale and timeline of major overseas export contracts.

The ICT Sector: Navigating a Turnaround

In stark contrast, the ICT sector has become a point of concern, with revenue dropping 17.7% to KRW 288.5 billion. The decline is attributed to fierce competition in the legacy System Integration (SI) business and the financial burden of transitioning to cloud-based services. While investments in deep-tech areas like AI, blockchain, and urban air mobility (UAM) hold future promise, the market is anxious for signs of short-term profitability. Investors will demand a clear strategy from management on how they plan to stabilize this division and monetize their future-forward investments.

Market Expectations & Macro-Economic Headwinds

The macroeconomic environment presents both opportunities and threats. Persistently high interest rates increase financial costs, which can strain capital-intensive projects in the ICT and new business sectors. Furthermore, a strong US dollar against the Korean Won (KRW 1,431.30) poses a risk of foreign exchange losses. On the other hand, global instability indirectly bolsters the Hanwha Systems defense sector. During the upcoming Hanwha Systems earnings call, management’s commentary on navigating these external pressures will be critically important.

Potential Scenarios from the Q3 IR Event

Positive Scenario: A strong earnings beat, coupled with the announcement of a major new defense contract, would ignite investor confidence. If management presents a convincing turnaround plan for the ICT sector with tangible milestones, and provides a clear roadmap for its exciting new ventures like its burgeoning space division, the stock could see a significant re-rating.

Negative Scenario: Conversely, if earnings miss expectations, the defense sector’s growth slows, or the ICT losses widen, investor sentiment could turn sour. Vague answers regarding future growth strategies or an inability to address macroeconomic risks could lead to increased uncertainty and a potential sell-off, especially if the current stock price already reflects high expectations.

Key Questions for Investors

Q1: What are the most critical announcements to listen for?

Focus on the defense sector’s overseas export performance, the ICT sector’s profitability path, and concrete roadmaps for future growth engines like space and UAM. Updates on financial health and major litigation risks are also crucial.

Q2: Why is the ICT sector struggling and can it recover?

The sector is squeezed by competition in its traditional businesses and heavy investment in cloud transformation. Recovery hinges on successfully monetizing new deep-tech ventures (AI, blockchain). A presentation of tangible progress during the IR could signal a positive turnaround.

Q3: What are Hanwha Systems’ main long-term growth drivers?

The primary long-term drivers are the sustained global demand for its defense products and strategic investments in high-potential new areas like space exploration, urban air mobility (UAM), AI, and autonomous driving sensors.

Conclusion: An Investment Strategy for the Q3 IR

Hanwha Systems presents a compelling, if complex, investment case. The long-term growth story, underpinned by a world-class defense division and ambitious future-tech bets, is intact. The improved balance sheet and massive order backlog provide a significant buffer. However, the immediate drag from the ICT sector cannot be ignored. The HANWHA SYSTEMS Q3 2025 IR is the company’s chance to reassure the market. Investors should adopt a cautious but optimistic approach, carefully analyzing the IR content for evidence that the company is effectively managing its risks while executing its growth strategy. Positive communication and clear strategic vision could be the catalyst that unlocks the next phase of value for Hanwha Systems stock.

Disclaimer: This analysis is for informational purposes only and is based on publicly available data. It does not constitute investment advice. Investors are responsible for their own investment decisions.

Leave a Reply