For investors tracking the automotive parts industry, a pivotal development has put DAYOU AUTOMOTIVE SEAT TECHNOLOGY (002880) stock in the spotlight. The company recently announced it has been selected by Hyundai Transys as the key supplier for the complete seat assembly for the highly anticipated new Sportage (NQ6) model. This isn’t just another contract; it’s a significant indicator of the company’s operational stability, technological prowess, and future growth trajectory.

This comprehensive analysis will delve into the specifics of this new order, evaluate DAYOU’s current financial fundamentals, and weigh the potential rewards against the inherent risks. We aim to provide a clear, data-driven perspective to help you understand what this development means for the DAYOU AUTOMOTIVE SEAT TECHNOLOGY stock and its long-term investment outlook.

The Sportage (NQ6) seat contract is a testament to DAYOU’s enduring partnership with Hyundai and a critical revenue stream that could bolster its financial standing amidst existing challenges.

Contract Breakdown: The Sportage (NQ6) Seat Supply Deal

What Exactly Happened?

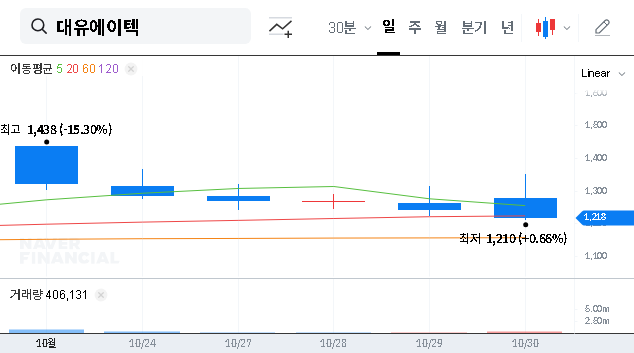

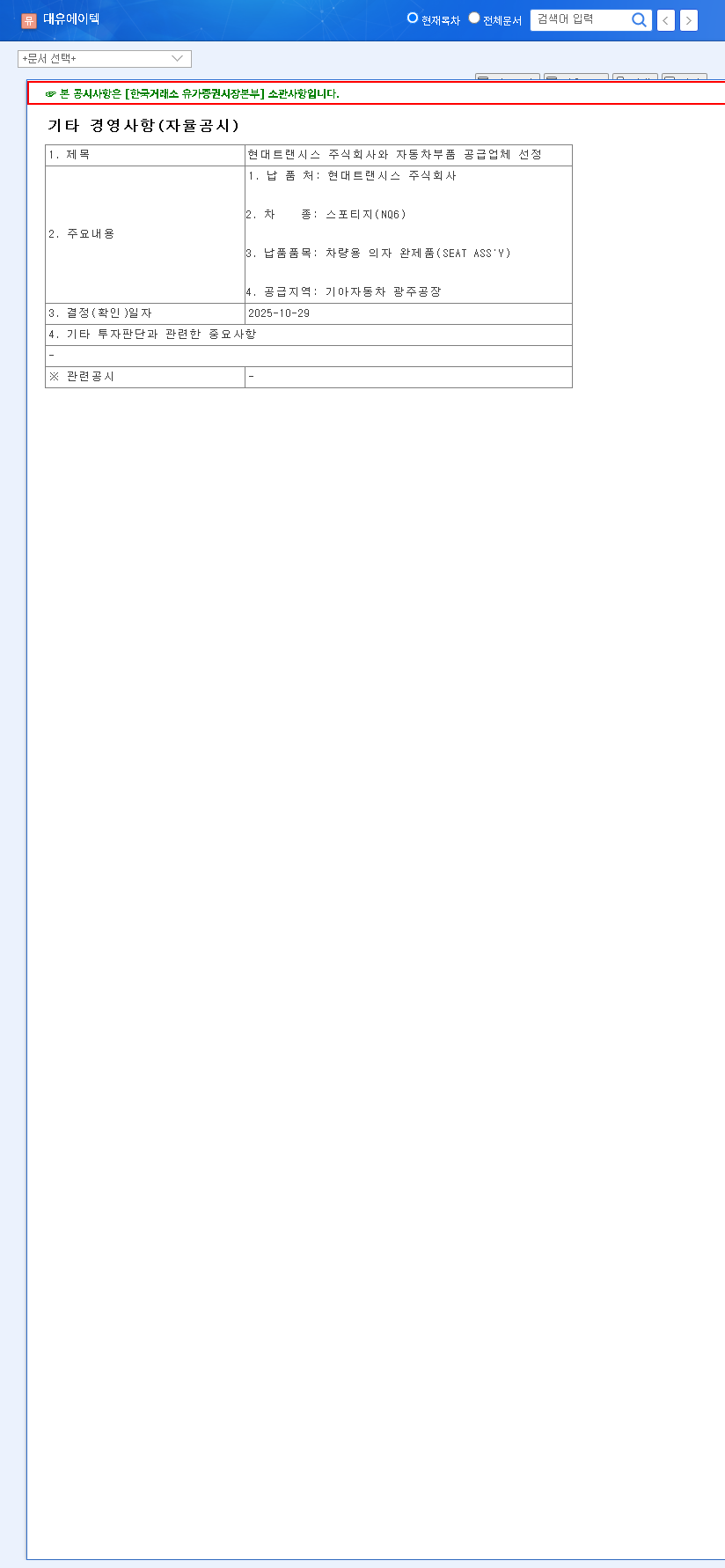

On October 30, 2025, DAYOU AUTOMOTIVE SEAT TECHNOLOGY CO., LTD formally announced its selection as the complete seat assembly supplier for the Sportage (NQ6) via Hyundai Transys. The announcement was made through a voluntary disclosure, which you can view here: Official Disclosure. Securing a contract for a globally popular model like the Sportage reaffirms DAYOU’s position as a trusted Tier 1 supplier and solidifies its relationship with the Hyundai Motor Group, a cornerstone of its business.

Deep Dive: DAYOU’s Fundamental Financial Health

As a specialized automotive seat manufacturer, DAYOU supplies essential components to industry giants like Hyundai Motor Group and KG Mobility. In the first half of 2025, the company reported sales of KRW 300.34 billion, a marginal 0.54% increase year-over-year. A standout performer was the Casper (AX1) vehicle seat segment, which saw sales soar by an impressive 43.86%, highlighting the company’s ability to capitalize on popular new models. To understand the full picture, we must examine both its strengths and weaknesses.

Positive Factors Driving Growth

- •Diversified New Model Orders: Beyond the Sportage NQ6 seat contract, DAYOU is expanding its revenue pipeline with orders for a range of new vehicles, including the Casper AX1, Ioniq 9, and PBV SW, ensuring a more resilient business model.

- •Optimized Governance: The recent merger with Smart Holdings has streamlined the corporate governance structure. This enhances management stability and decision-making efficiency, which is a positive signal for investors.

- •Proven Quality and Stability: An exceptional 24-year record without labor disputes, combined with Hyundai/Kia’s prestigious Quality 5-Star certification, underscores DAYOU’s reliable production capabilities and superior quality control systems.

Key Risk Factors to Monitor Closely

- •High Debt Load: The company’s total borrowings stand at KRW 136.7 billion, which is a significant 281.13% of its total equity. This high leverage poses a considerable financial risk and could constrain future investments.

- •Speculative Credit Rating: A short-term credit rating of B- is considered ‘highly speculative.’ This can make it more difficult and expensive for the company to secure new financing, potentially impacting liquidity.

- •Macroeconomic Headwinds: The broader automotive parts industry faces challenges from a potential global economic slowdown and rising protectionist policies, which could negatively impact exports and overall demand.

Investment Outlook: Weighing the Pros and Cons

The Sportage (NQ6) contract is undoubtedly a positive catalyst. It promises a stable, long-term revenue stream and enhances DAYOU’s reputation, which could attract further business. Industry experts, such as those at leading automotive market research firms, often view such contracts as a strong vote of confidence from major automakers.

However, investors must temper this optimism with caution. The contract’s immediate financial impact is unclear without details on volume and profitability. More importantly, this single deal does not erase the underlying financial vulnerabilities. The high debt-to-equity ratio and low credit rating remain significant concerns that require active management and a clear deleveraging strategy.

Final Verdict and Investor Action Plan

The selection as a Hyundai Transys supplier for the new Sportage is a significant operational win for DAYOU AUTOMOTIVE SEAT TECHNOLOGY. It strengthens business continuity and provides a much-needed tailwind for revenue growth. For the DAYOU AUTOMOTIVE SEAT TECHNOLOGY stock, this news provides a positive narrative.

Nevertheless, a prudent investment decision requires a balanced view. While the long-term prospects are improving, the short-term financial risks are still present. Investors should closely monitor the following key points:

- •Contract Profitability: Watch for future disclosures on the contract’s financial specifics, including expected margins.

- •Financial Improvement Efforts: Look for concrete steps taken by management to reduce debt and improve the company’s credit rating.

- •Broader Market Performance: Keep an eye on sales trends for other key models in DAYOU’s portfolio and the overall health of the global auto market.

Disclaimer: This analysis is for informational purposes only and does not constitute financial advice. All investment decisions should be made based on your own research and discretion.

Leave a Reply