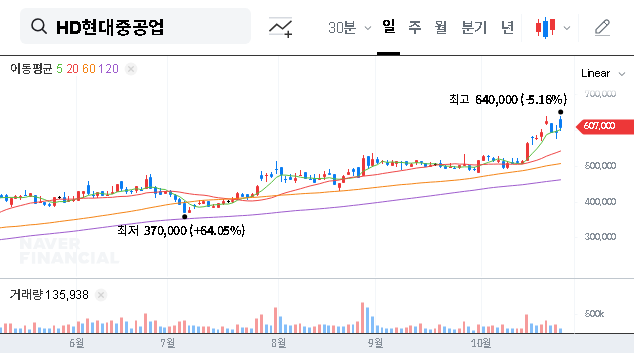

The new HD Hyundai Heavy Industries contract, a monumental 468.9 billion KRW deal, has sent ripples through the market, cementing the company’s status as a cornerstone of the South Korea defense industry. Announced on October 30, 2025, this agreement with the Defense Acquisition Program Administration (DAPA) for the KSS-II submarine performance upgrade is more than just a figure on a balance sheet; it’s a long-term strategic win that promises stable growth and technological validation. This deep-dive analysis will dissect the contract’s implications, evaluate HHI’s robust fundamentals, and provide a comprehensive outlook for investors considering HD Hyundai Heavy Industries stock.

This significant development represents a major step forward in modernizing naval capabilities and highlights HHI’s critical role in national security. For stakeholders and potential investors, understanding the nuances of this deal is key to appreciating the company’s future trajectory.

Deconstructing the Landmark KSS-II Upgrade Contract

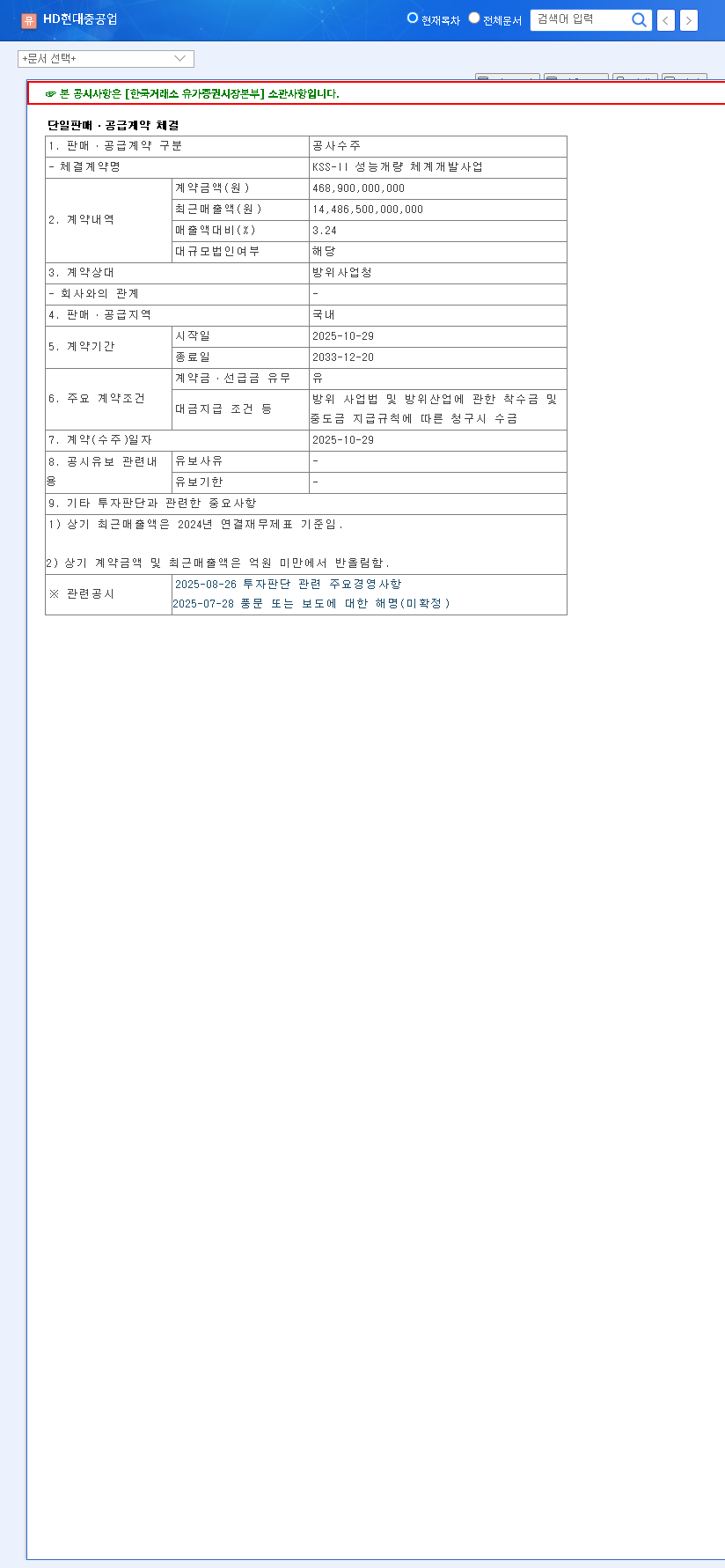

On October 30, 2025, HD Hyundai Heavy Industries formalized a landmark single sales and supply contract for the ‘KSS-II Performance Improvement System Development Project’. The agreement, valued at a substantial 468.9 billion KRW, was made with South Korea’s Defense Acquisition Program Administration (DAPA). The project’s timeline is extensive, running for over eight years from October 29, 2025, to December 20, 2033, ensuring a predictable and long-term revenue stream for HHI’s defense division. You can view the Official Disclosure for this DAPA contract on the DART system.

What is the KSS-II Upgrade?

The KSS-II, also known as the Type 214 submarine, is a critical asset in the Republic of Korea Navy’s fleet. This performance improvement project is not a routine maintenance task; it is a comprehensive modernization effort. This KSS-II upgrade will likely involve integrating state-of-the-art systems, including advanced sonar, new combat management systems, and potentially enhanced propulsion and stealth technologies. By undertaking this complex project, HHI is not just fulfilling a contract but is also at the forefront of advancing naval defense technology, a move that reinforces its global standing.

This long-term, high-value HD Hyundai Heavy Industries contract provides a clear runway for revenue growth, strengthens its defense portfolio, and powerfully validates its advanced technological capabilities on a global stage.

Core Strengths: HHI’s Diversified & Robust Foundation

The new defense contract amplifies the strength of HHI’s already formidable business fundamentals. The company’s diversified portfolio provides a stable base that mitigates risks and creates synergistic opportunities. For more context on industry trends, you can explore our overview of the global shipbuilding market.

- •Shipbuilding Leadership: Constituting 70% of revenue, HHI is a dominant force, particularly in the eco-friendly vessel market. With stricter regulations like the IMO’s emissions standards, demand for green ships is set to surge, positioning HHI for sustained market leadership.

- •Offshore & Energy Expansion: As oil prices stabilize, a recovery in offshore plant orders is anticipated. HHI is also future-proofing its portfolio by investing in next-generation energy, including renewables and Small Modular Reactors (SMRs).

- •Engine & Machinery Innovation: The company leads in developing advanced engines, including ammonia-fueled models, which gives it a significant competitive advantage as the maritime industry transitions to cleaner fuels.

- •Stellar Financial Health: With a stable debt-to-equity ratio of 219.30% and a negative net borrowings ratio, HHI’s financial standing is exceptionally sound. A massive 2.2 trillion KRW in net cash flow from operations ensures ample liquidity for future investments.

Investment Thesis: Why the HHI Stock Outlook is Bright

The KSS-II project is a powerful catalyst for HD Hyundai Heavy Industries stock. The direct and indirect benefits create a compelling investment case.

Key Positive Impacts on HHI

- •Guaranteed Revenue Stream: The 8-year contract ensures stable revenue and enhances earnings visibility, a highly attractive feature for investors seeking stability.

- •Enhanced Business Diversification: A stronger defense segment reduces reliance on the cyclical shipbuilding industry, creating a more resilient and balanced business model.

- •Global Technology Showcase: Successfully executing the KSS-II upgrade will serve as a powerful marketing tool, potentially opening doors to further international defense contracts.

Investor Action Plan & Recommendation

Given the confluence of a landmark defense contract, strong underlying fundamentals, and a clear path to improved profitability, the outlook for HHI is decidedly positive. This event serves as a strong affirmation of the company’s growth strategy and technical expertise. Therefore, a ‘Buy’ recommendation is warranted for investors with a medium to long-term horizon.

However, prudent investors should continue to monitor key variables, including the project’s specific profit margins, broader macroeconomic conditions, and the company’s ability to secure follow-on orders in the defense sector. The synergy between its defense and commercial divisions will be a key factor in maximizing long-term shareholder value.

Frequently Asked Questions (FAQ)

What is the value and scope of the recent HD Hyundai Heavy Industries contract?

HHI secured a contract worth 468.9 billion KRW from DAPA for the ‘KSS-II Performance Improvement System Development Project,’ which involves upgrading key naval submarine systems over approximately eight years.

How does this contract impact HHI’s revenue?

The contract amount represents roughly 3.24% of HHI’s recent annual revenue and will be recognized incrementally over the long-term contract period, providing a stable and predictable contribution to top-line growth.

What is the investment outlook for HD Hyundai Heavy Industries stock after this deal?

The outlook is highly positive. The deal demonstrates fundamental strength, diversifies revenue, and showcases technological leadership. This combination is expected to boost investor confidence and have a favorable impact on the stock price, supporting a ‘Buy’ rating.

Leave a Reply