The recent news of the SK ie technology rights offering has sent ripples through the investment community, presenting a critical juncture for the company and its shareholders. With 209.4 billion KRW on the line, investors are faced with a pivotal question: is this capital raise a strategic masterstroke to solidify SKIET’s market leadership and financial stability, or does it signal underlying risks and the unwelcome dilution of shareholder value? This comprehensive analysis will dissect the offering, evaluate SKIET’s robust fundamentals, and provide a strategic roadmap for investors navigating this event.

We will explore the intricacies of this major financial decision, its potential impact on SKIET stock analysis, and what it means for the company’s long-term trajectory in the competitive EV battery separator market.

Dissecting the SK ie technology Rights Offering

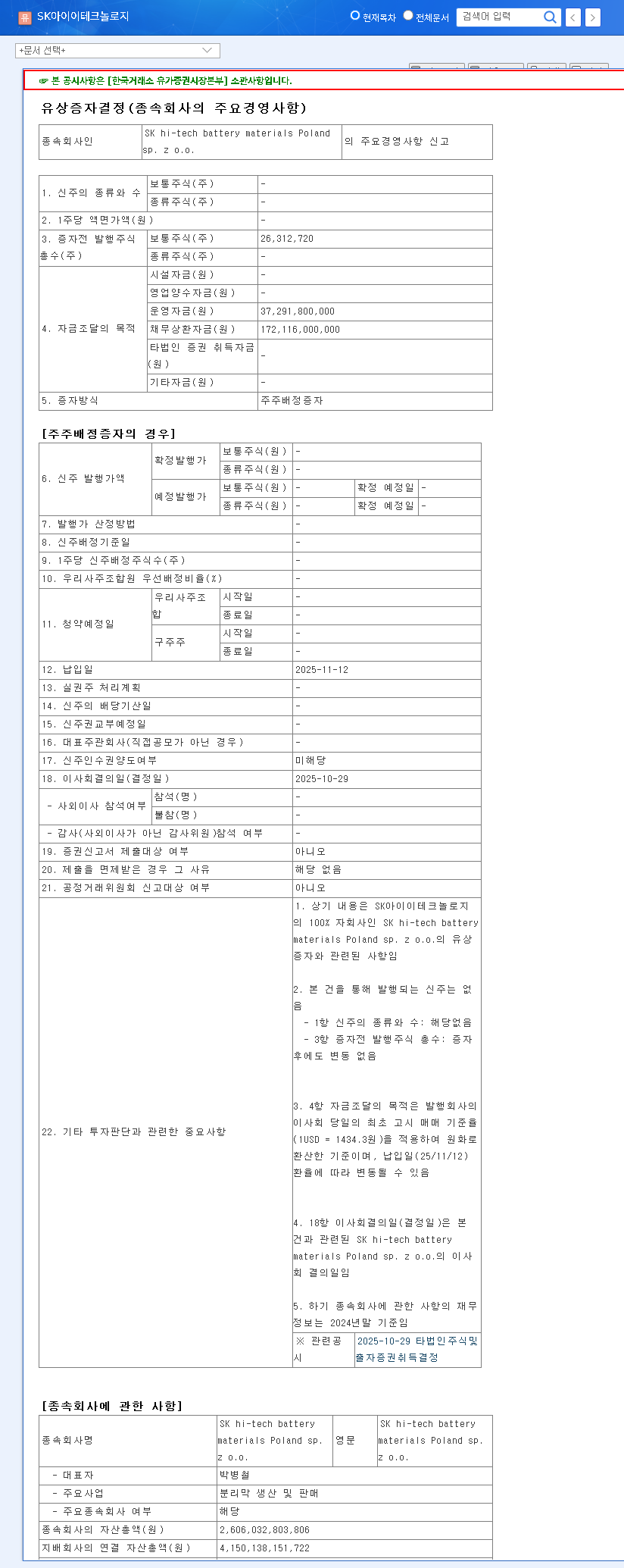

On October 29, 2025, SK ie technology Co., Ltd. (SKIET) formally announced a significant rights offering aimed at its subsidiary, SKhi-techbatterymaterialsPolandsp.zo.o. This move, conducted via a shareholder allocation method, is designed to raise a substantial 209.4 billion KRW. The primary motivation behind this capital injection is twofold: a strategic deleveraging of the subsidiary’s balance sheet and securing necessary operational liquidity.

The core of the strategy is to allocate the majority of the funds, approximately 172.1 billion KRW, towards debt repayment, with the remaining 37.3 billion KRW earmarked for operating capital. This allocation clearly signals a management priority to fortify the company’s financial foundation.

This decision is not just a financial maneuver; it’s a statement of intent to improve the overall financial structure, reduce interest burdens, and ensure the Polish subsidiary can operate and expand with greater stability. For detailed, official information, investors should consult the original filing. Official Disclosure: Click to view DART report.

Company Fundamentals and Market Position

Improving Financial Health and Profitability

Despite a decrease in top-line sales, SKIET’s recent financial reports reveal a positive trend in profitability. Through disciplined cost-cutting and a strategic shift towards higher-margin, value-added products, both operating and net profits are on an upward trajectory. The company’s debt-to-equity ratio has notably improved, falling from 58.95% to a more manageable 49.38%, a clear indicator of enhanced SKIET financial health. This rights offering, primarily aimed at debt reduction, is set to further strengthen this positive trend, de-risking the balance sheet and improving resilience against economic headwinds.

Unmatched Technological Edge in the LiBS Market

SKIET’s competitive advantage is anchored in its world-class technology within the Lithium-ion Battery Separator (LiBS market). Key differentiators include:

- •Sequential Stretching Process: A proprietary manufacturing technique that allows for precise control over separator pore structure, enhancing battery safety and performance.

- •Thin Film Leadership: The development of ultra-thin 5㎛ film products, which enables higher energy density in batteries—a critical factor for increasing EV range.

- •Advanced Coating Technology: Commercialization of double-sided simultaneous coating, improving the durability and lifespan of the battery cell.

Furthermore, global policy is creating significant tailwinds. The U.S. Inflation Reduction Act (IRA) and its stringent supply chain requirements are expected to disadvantage Chinese competitors, positioning SKIET to capture a larger share of the lucrative North American market. For more on this, you can review expert analysis from high-authority sources like Reuters on the IRA’s impact on EV supply chains.

Investor Impact and Strategic Outlook

The Double-Edged Sword: Dilution vs. Growth

The most immediate concern for existing shareholders is the potential for value dilution. A rights offering increases the total number of shares outstanding, which can decrease the value per share if an investor chooses not to participate. This often causes short-term downward pressure on the stock price. However, the long-term view can be markedly different. By using the funds to pay down debt and invest in operations, SKIET is positioning itself for more sustainable and profitable growth. A healthier balance sheet can lead to a higher valuation multiple from the market over time, potentially offsetting the initial dilution. The key is whether management can efficiently convert this new capital into tangible returns. Investors looking to deepen their knowledge may want to read our guide on analyzing a company’s financial health.

An Action Plan for Investors

Navigating the SK ie technology rights offering requires a calculated approach. Here are strategic steps to consider:

- •Analyze the Terms: Carefully review the official disclosure for specifics on the new share price, subscription ratio, and key dates. Understanding the discount offered is crucial to evaluating the proposition.

- •Assess Long-Term Conviction: If you believe in SKIET’s technological leadership and the growth of the EV battery separator market, participating in the offering could be a way to increase your position at a potential discount.

- •Monitor Fund Utilization: Post-offering, closely watch quarterly earnings reports to see how management is deploying the capital. Evidence of effective debt reduction and operational improvements will be key validation points.

- •Consider Macro Factors: Keep an eye on interest rates, currency fluctuations, and raw material costs, as these will continue to influence SKIET’s performance.

Conclusion: A Strategic Move for a Stronger Future

While the short-term market reaction to the SK ie technology rights offering may be one of caution due to dilution concerns, the underlying strategic rationale is sound. This is a proactive move to strengthen the company’s financial core, reduce risk, and empower its European operations for future growth. For the long-term investor, the decision hinges on confidence in SKIET’s management and its enduring technological prowess in the booming LiBS market. If executed effectively, this capital raise is less of a crisis and more of a catalyst, paving the way for a more resilient and valuable enterprise.

Leave a Reply