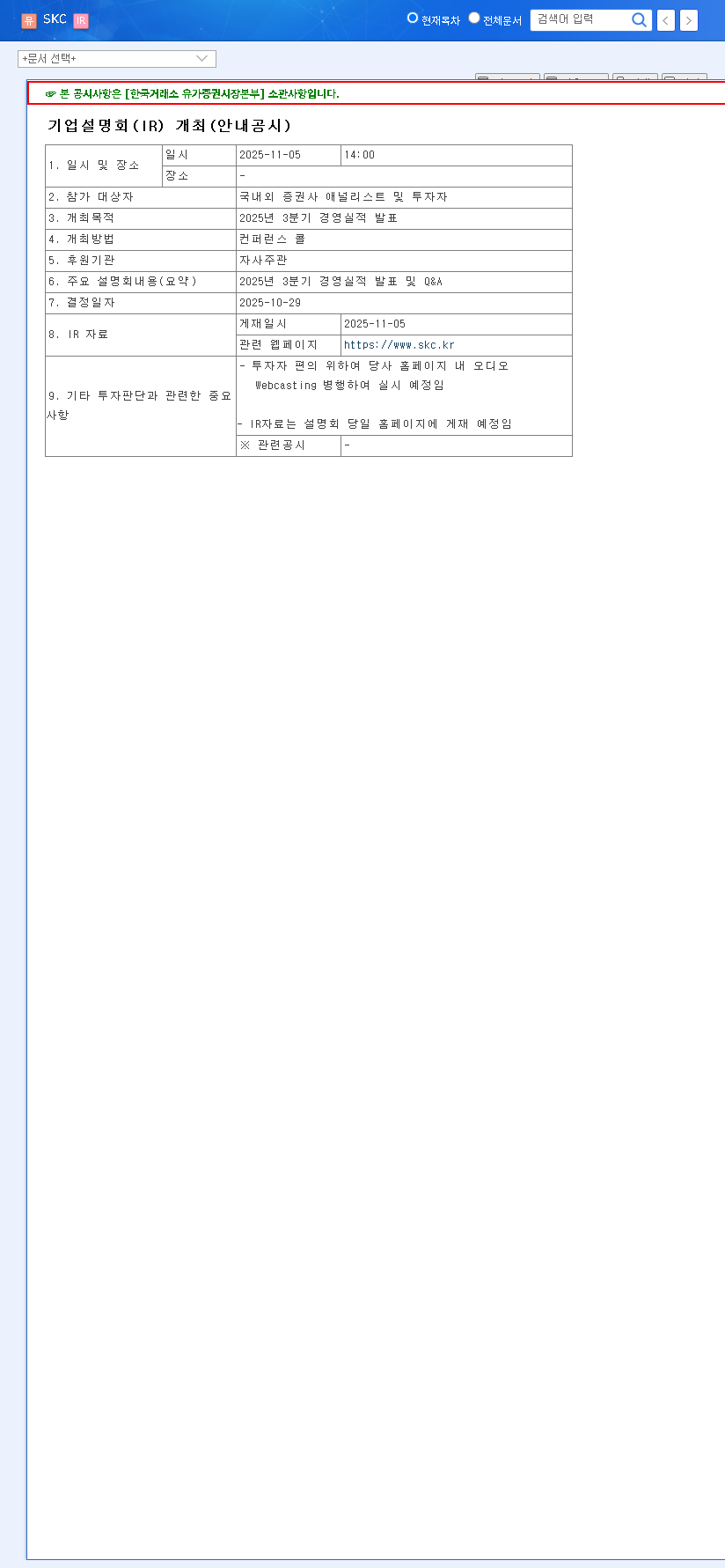

The upcoming SKC LTD Q3 2025 earnings announcement and subsequent investor relations (IR) call, scheduled for November 6, 2025, at 09:00 KST, represents a pivotal moment for the company and its stakeholders. Investors are eagerly awaiting clarity on the effectiveness of SKC’s strategic business restructuring, the performance of its core divisions, and the roadmap for future growth. This event is far more than a simple financial report; it’s a critical test of management’s ability to navigate a complex market and deliver on its promises.

This comprehensive analysis dissects the key factors influencing SKC’s performance, from the challenges in battery materials to the explosive growth in AI semiconductors. We provide an in-depth look at the fundamentals, potential catalysts, and risks to help you formulate a prudent investment strategy ahead of the official SKC investor relations briefing. All data is based on the company’s H1 2025 performance and market analysis, with further details available in the Official Disclosure.

SKC’s Strategic Overhaul: Focusing the Portfolio

SKC is in the midst of a significant business transformation, sharpening its focus on three core pillars: rechargeable battery materials (led by SK Nexilis), chemicals (SK picglobal), and semiconductor materials (anchored by ISC and SK Enpulse). Recent strategic divestitures, including the sale of the Fine Ceramics, CMP PAD, and FCCL businesses, are not signs of weakness but rather calculated moves to streamline operations, concentrate resources on high-growth areas, and bolster the company’s financial health. The issuance of exchangeable bonds in May 2025 further underscores this strategy, securing vital capital for future investments while managing debt.

The core question for the Q3 2025 earnings call is whether the growth in the semiconductor division can offset the persistent headwinds in the battery materials and chemicals sectors, proving the restructuring strategy is bearing fruit.

Deep Dive: Performance by Business Segment

1. Rechargeable Battery Materials (SK Nexilis)

The copper foil business, essential for EV batteries, faces a mixed reality. While long-term demand linked to the global EV transition remains a powerful tailwind, the short-term picture is challenging. An operating rate of just 58.6% in the first half of 2025 highlights issues of oversupply in the market, primarily from Chinese competitors, and a temporary slowdown in EV demand in certain regions. The expansion of its Poland plant is a strategic play for the European market, but investors will be looking for a clear plan during the SKC LTD Q3 2025 earnings call to improve utilization rates and manage production costs effectively.

2. Chemical Business (SK picglobal)

SKC’s chemical division, centered on Propylene Glycol (PG) and Propylene Oxide (PO), benefits from a competitive advantage with its eco-friendly HPPO manufacturing process. This has allowed it to maintain a high operating rate of 93.6%. However, the chemical industry is cyclical and currently facing sluggish global demand, which puts pressure on margins. This division’s underperformance acts as a drag on consolidated earnings, and analysts will be keen to hear about strategies for profitability improvement and market diversification.

3. Semiconductor Materials (ISC & SK Enpulse)

This segment is SKC’s brightest star. The explosive growth of the AI semiconductor market is a massive tailwind for ISC. As a leading producer of test sockets, which are critical components for testing high-performance chips like GPUs and AI accelerators, ISC is perfectly positioned. Its strong Q2 2025 performance was a direct result of this trend. Future growth is expected to accelerate with new supplies of module testers and test sockets. For a detailed view on market trends, check out our deep dive into the semiconductor industry. This division’s success is crucial to the overall SKC stock analysis and investment thesis.

Financial Health & Key Metrics to Watch

As of H1 2025, SKC’s financials tell a story of transition. While revenue increased year-over-year to KRW 9.06 trillion, the company posted an operating loss of KRW 144.6 billion. This highlights the core challenge: top-line growth isn’t yet translating to bottom-line profitability due to the struggles in battery materials and chemicals. Positively, the debt-to-equity ratio remains healthy at 76.93%, well below the company’s target of 200%, providing financial flexibility for strategic investments.

- •ISC Growth Rate: Investors will want to see continued double-digit growth and positive forward-looking statements.

- •SK Nexilis Operating Rate: Any tangible improvement or a clear roadmap to achieving higher utilization will be a major positive catalyst.

- •Profitability Margins: Look for updates on cost-cutting measures and margin improvement plans across all divisions.

- •Capital Expenditure Plans: Details on future investments, particularly in the semiconductor space, will signal long-term growth ambitions.

Investment Outlook: A Cautious ‘Hold’

SKC is a company with undeniable long-term potential, particularly through its exposure to the AI revolution via ISC. The commitment to restructuring and focusing on core strengths is commendable. However, the short-term profitability challenges in two of its three main businesses cannot be ignored. The market needs to see tangible proof that the turnaround is taking hold.

Therefore, a ‘Hold’ investment opinion is warranted pending the results and guidance from the SKC LTD Q3 2025 earnings call. While the long-term growth story is compelling, a cautious and watchful approach is prudent until stabilization and performance improvements are clearly demonstrated. A positive surprise in the battery materials segment or an even stronger-than-expected forecast for semiconductors could quickly change this outlook.

Leave a Reply