The market is buzzing with news surrounding ECOPRO BM, a key player in the secondary battery market. The company’s largest shareholder, Ecopro, has divested a significant portion of its stake, raising questions among investors about the stock’s future. This move comes at a challenging time, with the electric vehicle (EV) market experiencing a slowdown and investor sentiment already subdued. Is this a sign of trouble, or a strategic maneuver by the parent company?

This comprehensive ECOPRO BM stock analysis unpacks the entire situation. We will dissect the specifics of the shareholding change, re-evaluate the company’s fundamentals based on its latest financial reporting, and explore the broader macroeconomic pressures at play. Our goal is to provide a clear, data-driven perspective to help you navigate both the short-term market volatility and the long-term growth potential of ECOPRO BM.

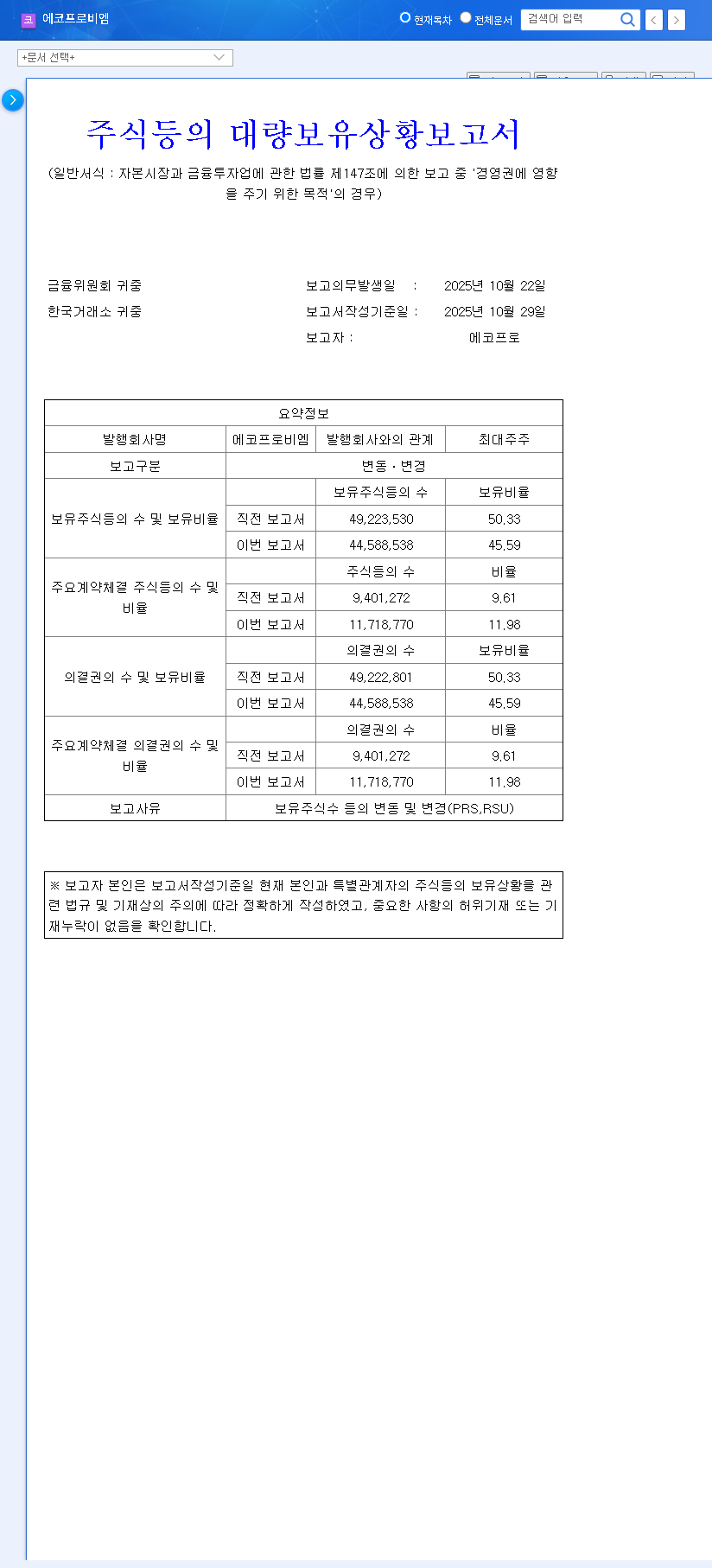

The Share Sale: What Exactly Happened?

The catalyst for recent market concern was a filing on October 29, 2025. According to the ‘Report on the Status of Large Shareholdings, etc. (General)’, Ecopro, the parent company and largest shareholder of ECOPRO BM CO.,LTD., confirmed a reduction in its ownership stake. The holding decreased from 50.33% to 45.59%, a notable drop of 4.74 percentage points. The full details are available in the Official Disclosure (DART).

Key Details of the Transaction:

- •Primary Reporter: Ecopro (as the largest shareholder)

- •Ownership Change: A decrease of 4.74%p, from 50.33% down to 45.59%.

- •Reason for Change: The filing cited open market sales by Ecopro (4,634,992 shares) and minor changes due to RSU grants for executives.

- •Purpose of Holding: Remains ‘Influence over management rights,’ indicating no change in control.

Why It Matters: Analyzing the Impact on ECOPRO BM

A major shareholder selling a large block of shares naturally creates ripples. However, it’s crucial to separate short-term market noise from long-term fundamental implications for any ECOPRO BM investment analysis.

While the optics of a major shareholder selling are rarely positive, discerning investors must look beyond the headline to assess the underlying health and long-term strategy of ECOPRO BM. The ‘why’ behind the sale is more important than the sale itself.

Decoding Ecopro’s Strategic Move

The sale is likely not a vote of no-confidence in ECOPRO BM’s fundamentals. Instead, it appears to be a strategic financial decision by the parent Ecopro group. The funds raised could be earmarked for group-wide investments, debt reduction, or securing capital for other ventures. While this creates a supply overhang and short-term price pressure on ECOPRO BM stock, it doesn’t inherently signal a flaw in its core business. Furthermore, with a 45.59% stake, Ecopro’s control over management remains firmly intact.

A Fresh Look at ECOPRO BM’s Fundamentals

Setting the share sale aside, the company’s semi-annual report for 2025 paints a mixed but revealing picture. For more on this, you can review our guide on how to analyze corporate financial statements.

- •Revenue Challenges: First-half sales stood at 1,409.5 billion KRW, a sharp 49% decline year-over-year. This reflects the broader EV market slowdown and heightened competition, as reported by sources like Bloomberg.

- •Profitability Picture: Operating profit returned to black at 51.271 billion KRW. While an improvement from a loss, this figure is substantially lower than historic highs, indicating margin pressure.

- •Strategic Investments: The company’s debt ratio has increased, driven by crucial CAPEX for overseas expansion in Hungary and North America. This is a classic growth-phase trade-off: sacrificing short-term cash flow (-260.1 billion KRW) for long-term production capacity and market share.

Navigating Macroeconomic Headwinds

No company operates in a vacuum. ECOPRO BM faces a complex macroeconomic environment that directly impacts its bottom line.

- •Currency Volatility: A high KRW/USD exchange rate (1,431.30) increases the cost of imported raw materials like nickel and lithium, squeezing profit margins.

- •High Interest Rates: Sustained high policy rates in the US (4.25%) and Korea (2.50%) raise the cost of capital, making it more expensive to finance the company’s ambitious global expansion plans.

- •Raw Material Prices: While falling oil prices may help with logistics, the volatility in key battery metals remains a significant variable affecting production costs and profitability.

Investor Action Plan & Final Verdict

The Short-Term Outlook: Caution is Key

In the short term, the large volume of shares sold by Ecopro will likely create downward pressure on the ECOPRO BM stock price. Investors should brace for volatility and monitor market sentiment closely. The key is to watch for communications from the Ecopro Group regarding the use of proceeds from the sale.

The Long-Term Thesis: Growth Drivers to Watch

The long-term investment case for ECOPRO BM hinges on its ability to execute its growth strategy. The fundamental driver will be the recovery of the global EV market and the successful ramp-up of its new production facilities. The expansion into next-generation materials (single crystal, LFP) is a critical pillar for future growth and higher margins.

In conclusion, while the shareholder divestment creates short-term headwinds, the core investment thesis remains tied to ECOPRO BM’s ability to navigate the current industry downturn and capitalize on the eventual rebound. A patient, fundamentals-focused approach is required. Investors should weigh the immediate risks against the company’s strategic positioning for the next wave of EV adoption.

Leave a Reply