The recent SK Square 11st divestment has sent ripples through the investment community, signaling a major strategic pivot for the South Korean investment holding company. SK Square Co., Ltd. has officially announced the sale of its entire stake in the e-commerce platform 11st for KRW 660.7 billion. This isn’t just a simple asset sale; it’s a calculated move to shed a loss-making subsidiary and double down on high-growth core businesses, most notably the semiconductor powerhouse, SK Hynix. For investors, this raises critical questions: What does this mean for the future of SK Square stock, and is now the right time to invest? This comprehensive analysis will explore the motives, financial implications, and long-term strategy following this landmark decision.

The Landmark Decision: Unpacking the 11st Sale

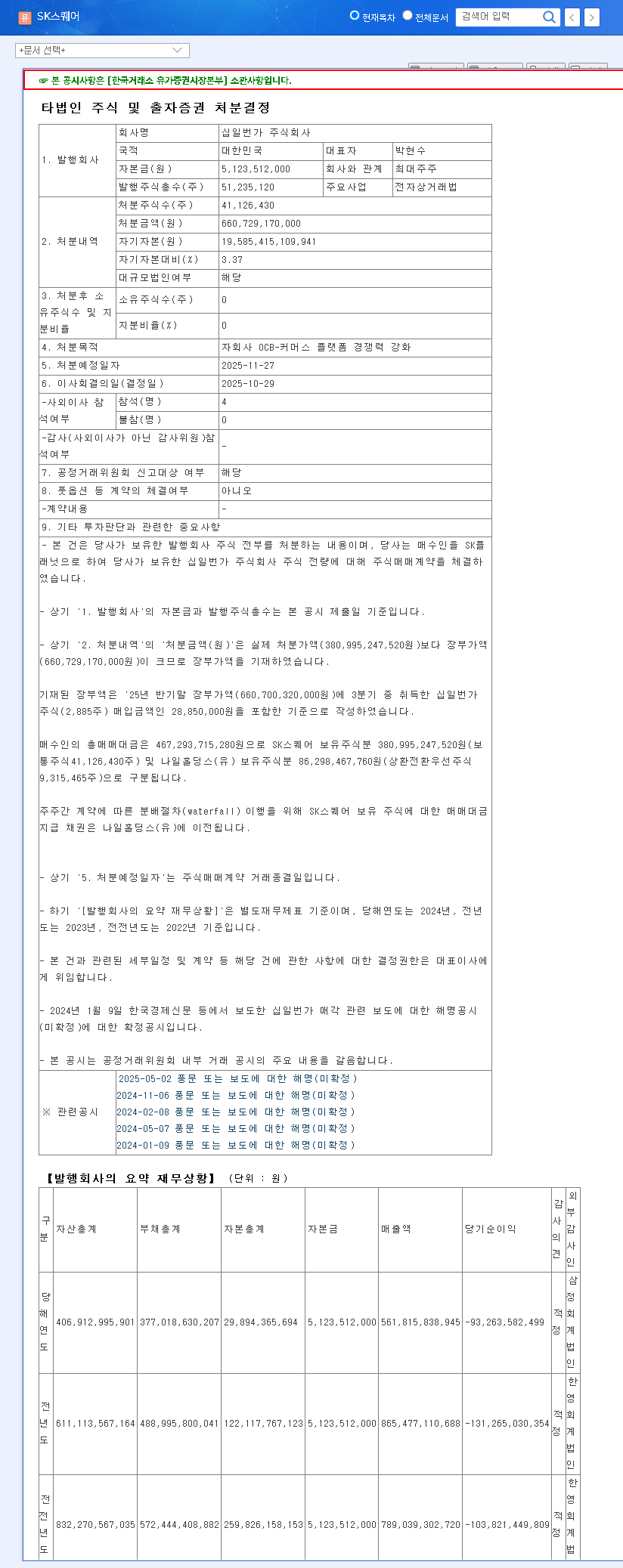

SK Square has confirmed its decision to dispose of its full KRW 660.7 billion stake in 11st, effectively reducing its ownership to 0%. This concludes an approximately seven-year journey with the e-commerce platform. The company’s stated purpose, according to the official disclosure, is to “enhance the competitiveness of the OCB-Commerce platform,” a clear indication of its intent to streamline operations and reallocate capital more efficiently. You can view the complete filing here: Official Disclosure (Source).

Why Divest Now? A Tale of Two Markets

The decision to proceed with the 11st sale is a direct result of two diverging realities. On one hand, the South Korean e-commerce market has become a hyper-competitive battleground. The dominance of players like Coupang and the aggressive market entry of Chinese platforms like AliExpress and Temu have squeezed margins and made profitability for platforms like 11st increasingly difficult. In the first half of 2025 alone, 11st recorded an operating loss of KRW 19.906 billion, continuing a trend of financial underperformance.

On the other hand, SK Square’s core holdings are thriving. The company’s consolidated operating profit surged to KRW 3.0534 trillion in H1 2025, largely driven by the stellar performance of SK Hynix. The global recovery in the memory semiconductor market, fueled by the insatiable demand for AI technologies, has positioned SK Hynix as a critical growth engine. This contrast made the decision clear: cut losses from the underperforming e-commerce arm to fuel the high-performing technology core.

Financial Impact and Future Strategy

The financial implications of the SK Square 11st divestment are overwhelmingly positive in the short term. The injection of KRW 660.7 billion in cash provides a massive boost to the company’s liquidity and strengthens an already healthy balance sheet, which boasts a low debt ratio of just 9.84%. By removing a chronically loss-making subsidiary, SK Square is poised to see a significant improvement in its consolidated profitability.

This strategic divestment is not just about stopping the bleeding; it’s about sharpening the company’s focus and reallocating capital to areas with the highest potential for exponential growth and shareholder value creation.

Redirecting Capital for Maximum Growth

The key question for investors is where this newfound capital will be deployed. The primary focus will undoubtedly be on strengthening its portfolio of high-growth technology assets. This includes:

- •Bolstering SK Hynix: Further investment in semiconductor R&D and production capacity, particularly in high-demand areas like High Bandwidth Memory (HBM) for AI applications. You can learn more about this trend from industry reports on the global semiconductor market.

- •Cultivating Other Subsidiaries: Accelerating the growth of other promising ventures like One Store (app market), Tmap Mobility (navigation and mobility services), and ADT Caps (security services).

- •Shareholder Returns: Continuing shareholder-friendly policies, such as the previously announced treasury stock cancellation, to directly enhance shareholder value.

SK Square Investment Analysis: A ‘Buy’ Opportunity?

With the divestment news, our SK Square investment analysis points towards a ‘Buy’ rating, but with key considerations. The mid-to-long-term success of SK Square stock will hinge on the flawless execution of its new, more focused strategy.

The Bull Case (Positive Factors)

- •Strengthened Financials: Profit turnaround, enhanced liquidity, and a cleaner balance sheet post-sale.

- •Laser Focus on Core Tech: Capital allocation is now directed towards the high-margin, high-growth semiconductor sector via SK Hynix. Check out our deep dive into SK Hynix’s AI dominance.

- •Improved Profitability: The removal of 11st’s consistent losses is expected to boost overall consolidated profit margins.

The Bear Case (Risks & Considerations)

- •Over-Reliance on SK Hynix: The company’s fortunes are now even more tightly linked to the volatile semiconductor market.

- •Execution Risk: Success depends on the wise investment of the proceeds and the ability to grow its other subsidiaries to profitability.

- •Subsidiary Performance: Other key holdings like One Store and Tmap Mobility are still facing intense competition and are not yet consistently profitable.

Conclusion: A Promising New Chapter

The SK Square 11st divestment is a decisive and logical move that positions the company for a more focused, tech-driven future. While risks remain, the strategic realignment to capitalize on the strength of SK Hynix and streamline the business portfolio is a compelling narrative for investors. The key will be to monitor how management deploys its new war chest and whether it can translate this strategic clarity into sustained earnings growth and long-term shareholder value.

Leave a Reply