In a challenging market for the construction sector, the recent DongshinEngineering&Construction contract announcement has stirred significant discussion among investors. The company secured a substantial ₩7.5 billion public works project, a development that appears as a beacon of hope against the backdrop of its deeply troubled H1 2025 financial performance. This comprehensive analysis will dissect the contract’s details, evaluate the company’s precarious financial state, and provide a clear outlook for investors weighing the potential risks and rewards.

We will explore whether this single contract is a genuine lifeline capable of initiating a turnaround or merely a temporary reprieve from more profound systemic issues plaguing the company’s fundamentals.

Is this ₩7.5 billion contract a genuine turning point for DongshinEngineering&Construction, or just a temporary bandage on a deeper financial wound? The answer lies in the details.

The Landmark ₩7.5 Billion Contract Details

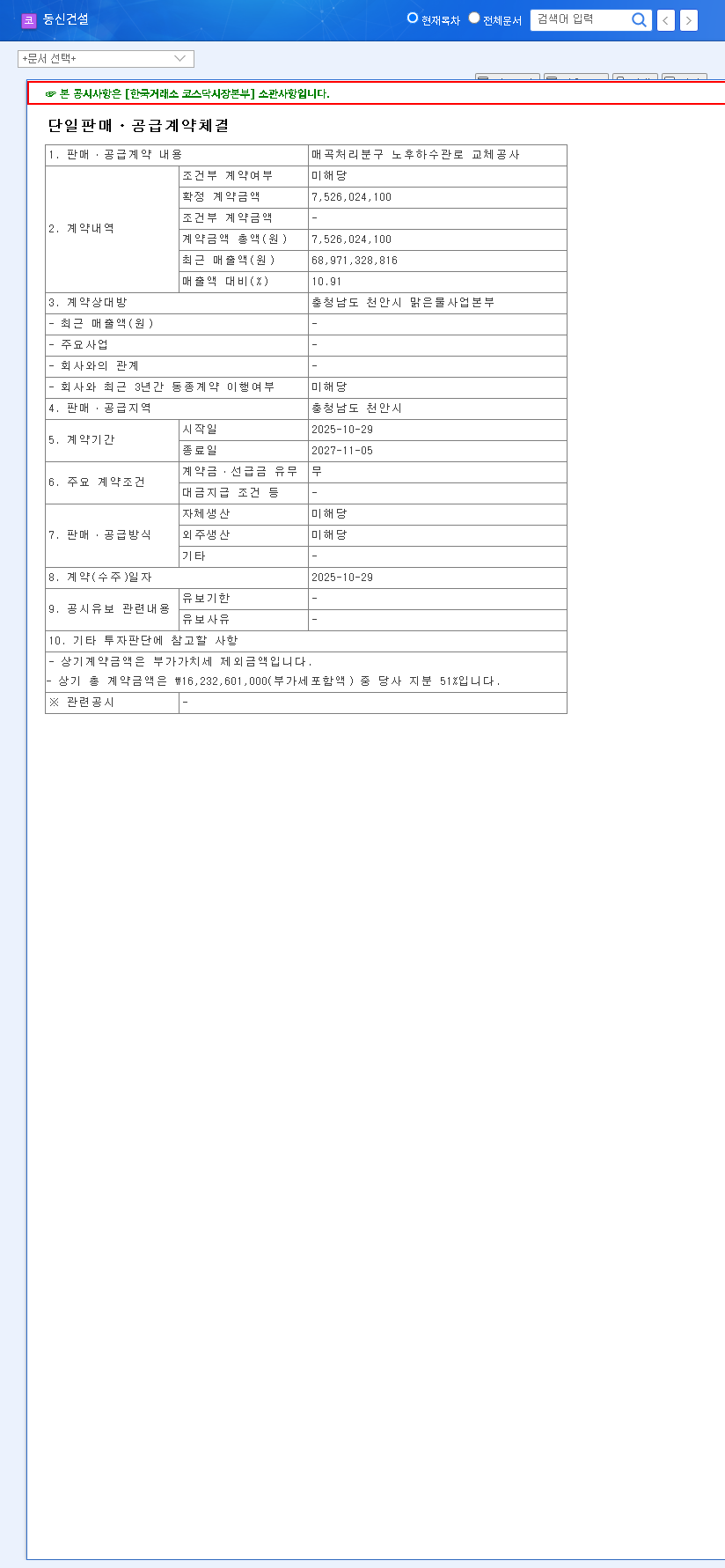

On October 29, 2025, DongshinEngineering&Construction formally announced the procurement of a single sales and supply contract with the Clean Water Business Headquarters of Cheonan City, Chungcheongnam-do. The project, officially titled the ‘Maegok Treatment District Old Sewage Pipeline Replacement Project,’ is valued at exactly ₩7,502,770,000. The details of this agreement were confirmed in an Official Disclosure filed on DART.

This figure is not trivial; it represents a significant 10.91% of the company’s total revenue from the 2024 fiscal year. The contract’s duration is set for approximately two years, commencing on October 29, 2025, and scheduled for completion by November 5, 2027. This timeline suggests a steady, albeit modest, revenue stream over the next 24 months, which is crucial for a company in its current position.

A Deep Dive into DongshinEngineering&Construction’s Financials

H1 2025 Performance: A Company in Distress

To understand the true weight of this new contract, one must first examine the dire state of DongshinEngineering&Construction’s financials as of its H1 2025 report. The numbers paint a grim picture of a company facing severe operational and market headwinds:

- •Revenue: Plummeted to ₩14.74 billion, a staggering 53.9% decrease year-on-year.

- •Operating Profit: Swung to a loss of ₩673.57 million, a dramatic reversal from a profit in the same period last year.

- •Net Profit: Dropped to ₩724.92 million, marking a 64.9% decrease year-on-year.

This sharp downturn is not an isolated event but a result of a perfect storm: the broader construction industry downturn, fierce competition for fewer public projects, and soaring raw material prices. Compounding these issues is a significant drop in new order intake and the looming financial risk from ongoing lawsuits, which could further strain the company’s balance sheet.

Strategic Analysis: Lifeline or Temporary Respite?

The Bull Case: Positive Catalysts

Despite the bleak financial context, this contract provides several tangible benefits. Firstly, it offers a direct injection into the revenue stream, which can partially offset the H1 decline and improve future earnings reports. Secondly, winning a public infrastructure bid from Cheonan City reaffirms the company’s technical competence and competitiveness, a crucial signal to the market. Finally, in a depressed market, any news of a new contract can provide a much-needed positive momentum for the DongshinEngineering&Construction stock and boost investor morale.

The Bear Case: Lingering Risks and Limitations

It would be imprudent to believe this single ₩7.5 billion deal can single-handedly reverse the company’s fortunes. Its scale is simply insufficient to cover the massive revenue shortfall and operating losses from the first half of the year. True recovery requires a consistent pipeline of larger projects combined with aggressive internal cost management. The uncertainty of future orders remains the primary risk. Furthermore, external macroeconomic pressures like high interest rates and fluctuating material costs could erode the profitability of this very contract.

Investor Outlook and Actionable Insights

Given the balance of factors, a cautious and watchful approach is strongly advised for investors. While the DongshinEngineering&Construction contract is a positive step, it is just one step on a long road to recovery. Before committing capital, investors should closely monitor the following key indicators, which might be covered in our quarterly construction sector report:

- •Future Order Pipeline: Are more large-scale contracts being secured?

- •Profitability Management: What strategies are being implemented for cost control?

- •Financial Health: How is the company addressing its balance sheet weaknesses and the outcome of pending litigation?

- •Macroeconomic Impact: How are changes in interest rates and commodity prices affecting operations?

In conclusion, this contract is a welcome development but not a panacea. Diligent monitoring of the company’s subsequent actions and the broader market environment is essential for making an informed investment decision.

Leave a Reply