The recent activity surrounding Eco Volt stock presents a classic investor’s dilemma: a significant vote of confidence from its largest shareholder clashing with deeply troubling financial results. While major shareholder Osung Advanced Materials signals a stronger commitment, Eco Volt’s 2025 half-year report reveals critical red flags that demand scrutiny. This comprehensive Eco Volt financial analysis will dissect these conflicting signals to provide a clear, actionable perspective for current and potential investors.

Can this insider buying truly steer the company towards recovery, or is it merely a defensive move in the face of a deepening crisis? Let’s explore what investors need to know before making their next move.

A Tale of Two Signals: Shareholder Confidence vs. Financial Reality

On one hand, we have a clear, bullish signal. On the other, the numbers paint a grim picture. Understanding both is crucial when evaluating the future of Eco Volt stock.

Osung Advanced Materials Doubles Down: A Strategic Power Play

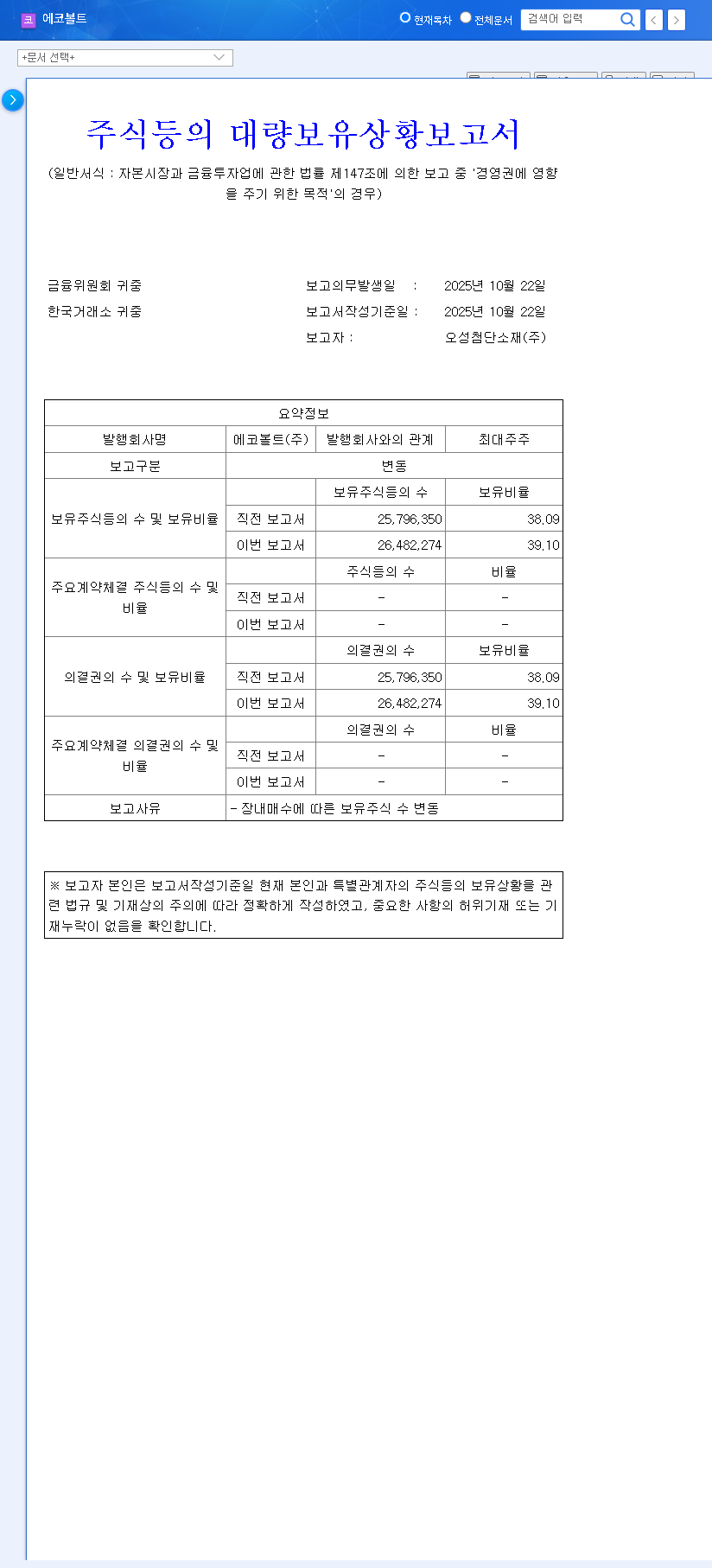

On October 28, 2025, Eco Volt’s largest shareholder, Osung Advanced Materials, acquired an additional 482,000 shares on the open market. This transaction increased its total ownership from 39.10% to 39.81%. The stated purpose, as per the Official Disclosure, was to strengthen its influence over management rights. This is a significant move, suggesting that Osung believes in the long-term potential of the company and is willing to invest more capital to guide its strategy. For the market, this can be interpreted as a vote of confidence from the party with the most insight into the company’s operations.

Unpacking the 2025 Half-Year ‘Earnings Shock’

Contrasting sharply with the shareholder’s optimism are Eco Volt’s alarming fundamentals. The 2025 half-year report was nothing short of a disaster, revealing deep-seated issues across the business.

- •Revenue Collapse: Consolidated revenue plummeted by a staggering 48.6% year-over-year, falling to KRW 115.7 billion. This wasn’t isolated to one division; the core automotive lighting, electrical equipment, and pharmaceutical wholesale segments all struggled simultaneously.

- •Profitability Erased: The company swung to an operating loss of KRW -7.3 billion. A key driver was an out-of-control surge in Selling, General, and Administrative (SG&A) expenses, which ballooned by an incredible 119.7%. The net loss widened to KRW -16.4 billion.

- •Deteriorating Financial Health: Total equity shrank by 11.5%. More alarmingly, the debt-to-equity ratio skyrocketed from a negligible 0.72% to a concerning 4.63%, signaling a rapid increase in financial risk.

While a major shareholder’s backing can provide a floor for a stock price, it cannot defy the gravity of deteriorating business fundamentals indefinitely. The key question for anyone investing in Eco Volt is whether the new management influence can orchestrate a genuine turnaround.

Investor Action Plan: A Conservative Approach is Prudent

Given the powerful negative momentum from the earnings report, the positive impact of the shareholder’s move is likely to be muted in the short term. A sustained rally in Eco Volt stock is highly improbable without tangible proof of a fundamental business recovery. Therefore, a cautious and observational stance is recommended.

Investors should shift their focus from the shareholding change to the underlying operational issues. To properly assess the situation, it’s helpful to learn more about analyzing company financial statements to understand these metrics deeply. Furthermore, the company’s fate is tied to the broader automotive market, and staying informed on industry trends from authoritative sources like leading financial news outlets is essential.

Key Factors to Monitor Moving Forward:

- •Q3 and Q4 Performance: Is there any sign of a revenue rebound in the automotive division or stabilization in other segments?

- •Cost Control Measures: What specific actions is management taking to rein in the explosive growth of SG&A expenses? Look for announcements on restructuring or efficiency programs.

- •Strategic Direction from Osung: Does the increased management control lead to new strategies, asset sales, or partnerships that could change the company’s trajectory?

Frequently Asked Questions (FAQ)

Why did Eco Volt’s major shareholder, Osung Advanced Materials, increase its stake?

Osung increased its stake to strengthen its influence over management rights. This move aims to enhance management stability and directly guide the company’s strategic decisions, signaling a long-term commitment despite poor recent performance.

How bad were Eco Volt’s recent financial results?

The financial results for the first half of 2025 were extremely poor. Revenue declined by nearly 50%, the company posted significant operating and net losses, and administrative costs soared over 119%. This indicates severe operational and financial distress.

What is the likely short-term impact on Eco Volt stock?

The shareholder purchase may provide some short-term price support or a minor rebound. However, the ‘earnings shock’ is a more powerful force and will likely create significant downward pressure, limiting any potential upside until fundamental improvements are evident.

Leave a Reply