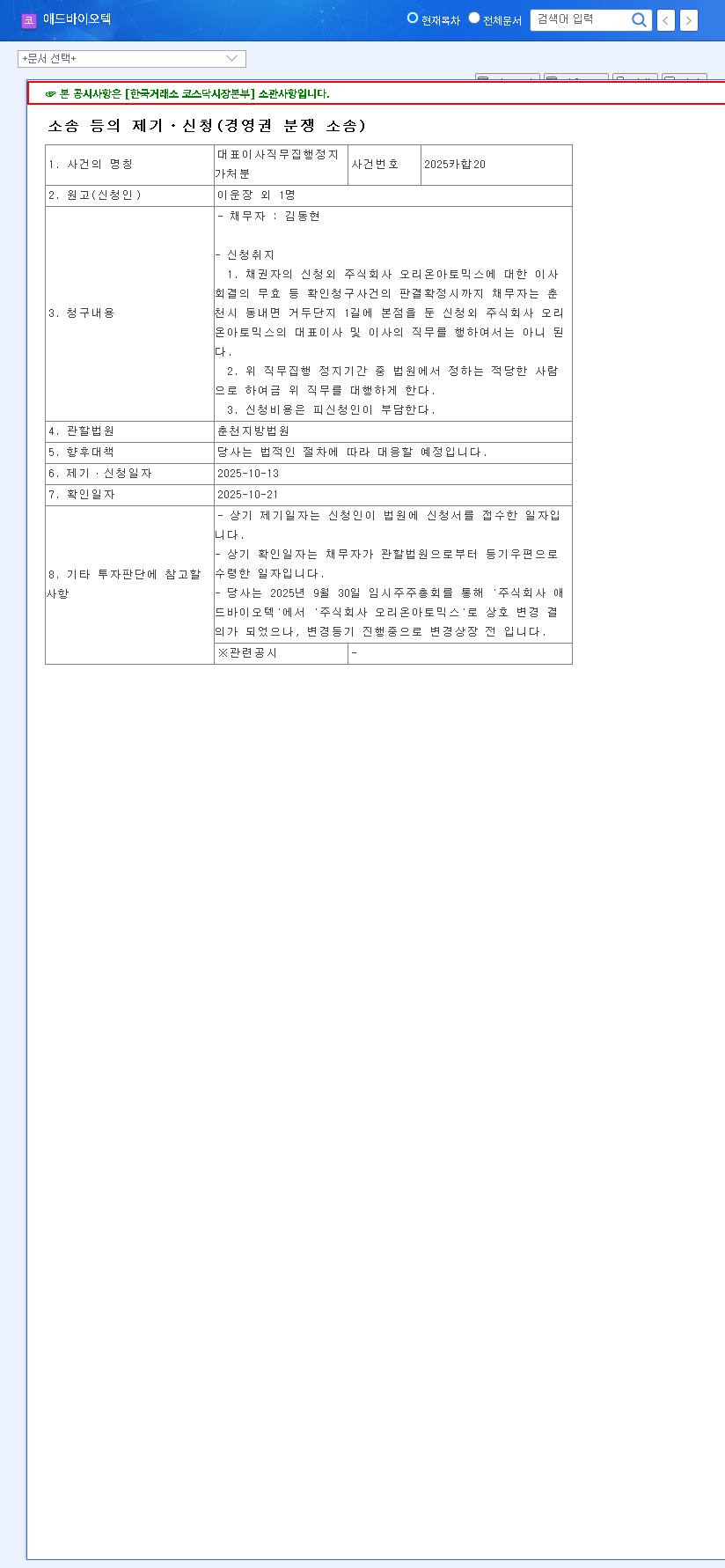

ADBIOTECH Capital Increase: Turning Crisis into Opportunity?

On October 27, 2025, ADBIOTECH Co.,Ltd. (179530) announced a significant, large-scale ADBIOTECH capital increase, capturing the immediate attention of the market. For a company grappling with severe financial deterioration and persistent operating losses, this move is a critical juncture. This comprehensive analysis will dissect the intricacies of this decision, evaluating its potential to steer the company out of crisis and its profound implications for current and prospective investors. We will meticulously examine the core motivations, from improving financial structure to fueling new business ventures and navigating a pivotal change in management control.

Is this capital injection the lifeline ADBIOTECH needs to innovate and grow, or will it merely dilute shareholder value and postpone an inevitable reckoning? Let’s dive into the details.

The Anatomy of the Deal: A Closer Look

The company detailed the rights offering in a major disclosure report. The move is designed to raise approximately 16.566 billion KRW through a third-party allotment, a method often used to bring in strategic investors. The full details can be verified in the Official Disclosure (DART Source).

Key Details of the ADBIOTECH Capital Increase

- •Shares Issued: 6,152,988 common shares

- •Issue Price: 2,693 KRW per share

- •Issue Ratio: Approximately 49% of existing shares, indicating significant dilution.

- •Key Investors: BK Partners Investment Fund 1 & 2

- •Key Dates: Payment on December 17, 2025, with an expected listing on January 2, 2026.

Crucially, this capital raise is intertwined with a change in the largest shareholder and a management rights transfer agreement. This is not just a financial maneuver; it’s a fundamental reset of the company’s trajectory.

Drivers Behind the Decision: Survival and Strategy

The decision stems from a dual need: immediate financial survival and long-term strategic repositioning. Understanding these drivers is key to performing a thorough ADBIOTECH stock analysis.

1. Addressing an Acute Financial Crisis

The company’s financial health is precarious. As of H1 2025, its debt-to-equity ratio stood at an alarming 877.68%, a figure that signals extreme financial leverage and risk. For context, a healthy ratio is typically below 2.0 (learn more about debt-to-equity ratios on Investopedia). Coupled with continuous operating losses and accumulated deficits, the capital increase was an unavoidable move to shore up the balance sheet and avoid insolvency.

2. Funding Future Growth Engines

Beyond survival, the funds are earmarked for growth. The capital is intended to fuel the development of promising new pipelines, such as IgY immune egg yolk antibodies and VHH antibodies (nanobodies). These technologies have significant potential in animal and human health markets. The funds will support critical R&D and both domestic and international clinical trials, securing a pathway to future revenue streams.

3. Facilitating a Management Overhaul

The capital increase is the mechanism for a change in control. By bringing in BK Partners as the new largest shareholder, the company is signaling a strategic pivot. This is more than just fundraising; it’s an effort to install a new management team with a fresh vision and, presumably, a more effective strategy for turning the company around.

Potential Impacts: The Bull vs. Bear Case

For investors, the ADBIOTECH capital increase presents a classic case of high risk and potential reward. It’s essential to weigh the positives against the significant negatives.

The Bull Case (Positive Impacts)

- •Improved Financial Stability: The ~16.5 billion KRW infusion will immediately reduce the crippling debt ratio and solve liquidity issues, providing a foundation for recovery.

- •Accelerated R&D and Growth: Secured capital can fast-track development and commercialization of new pipelines, unlocking long-term value for the company.

- •Vote of Confidence: The participation of a new financial investor like BK Partners can be seen as a positive signal, suggesting they see untapped value and a viable path to profitability.

The Bear Case (Negative Impacts & Risks)

- •Severe Share Dilution: Issuing new shares equivalent to ~49% of the existing float will significantly dilute the value of each existing share. This is the most immediate and certain negative impact for current shareholders.

- •Execution Risk: A capital injection is only a temporary fix. The ultimate success depends on the new management’s ability to execute a turnaround strategy and achieve profitability, which is far from guaranteed.

- •Price Pressure: The issue price of 2,693 KRW represents a ~19.8% discount to the recent price, which could create downward pressure on the stock as the market absorbs the new shares.

Investor Outlook & Key Factors to Monitor

For investors considering an ADBIOTECH stock position, a wait-and-see approach may be prudent. Long-term value recovery hinges on several critical factors that must be closely monitored in the coming months.

Pay close attention to the new management’s stated business plan and their execution capabilities. Are their profitability targets realistic? Watch for progress reports on R&D milestones for the IgY and VHH antibody pipelines. Successful clinical data or commercial partnerships would be powerful catalysts. Finally, keep an eye on the broader macroeconomic environment, as high interest rates can continue to pressure highly-leveraged companies. For more on this sector, you can read our Guide to Biotech Investing.

Disclaimer: This analysis is for informational purposes only and is not investment advice. All investment decisions should be made based on your own research and judgment.

Leave a Reply