A significant institutional sell-off can send ripples through the market, leaving investors to question the future of a company. This is the exact scenario facing DongKook Pharmaceutical stock after VIP Asset Management, a major institutional investor, drastically reduced its stake. This move has understandably raised concerns, but it also prompts a critical question: Is this a red flag signaling fundamental weakness, or a golden opportunity to invest at a more attractive valuation? This comprehensive DongKook Pharmaceutical stock analysis will dissect the event, evaluate the company’s core fundamentals, and provide a clear, actionable investment outlook for 2025 and beyond.

The Catalyst: Unpacking the VIP Asset Management Sell-Off

On October 27, 2025, market participants took notice as VIP Asset Management filed a mandatory disclosure revealing a substantial change in its holdings of DongKook Pharmaceutical Co., Ltd. The report detailed a significant ownership reduction of 1.90 percentage points, taking their stake from 7.71% down to 4.81%. This disposition involved the market sale of 170,051 shares between October 21 and October 24, 2025. Such a large-scale sale by a respected asset manager is a material event that warrants close scrutiny. For full transparency, you can view the Official Disclosure (DART).

Why the Sudden Move? Potential Reasons Behind the Stake Reduction

An institutional sell-off is rarely based on a single factor. It’s typically a calculated decision stemming from a combination of company-specific performance, portfolio strategy, and broader market conditions.

1. Concerns Over Recent Corporate Fundamentals

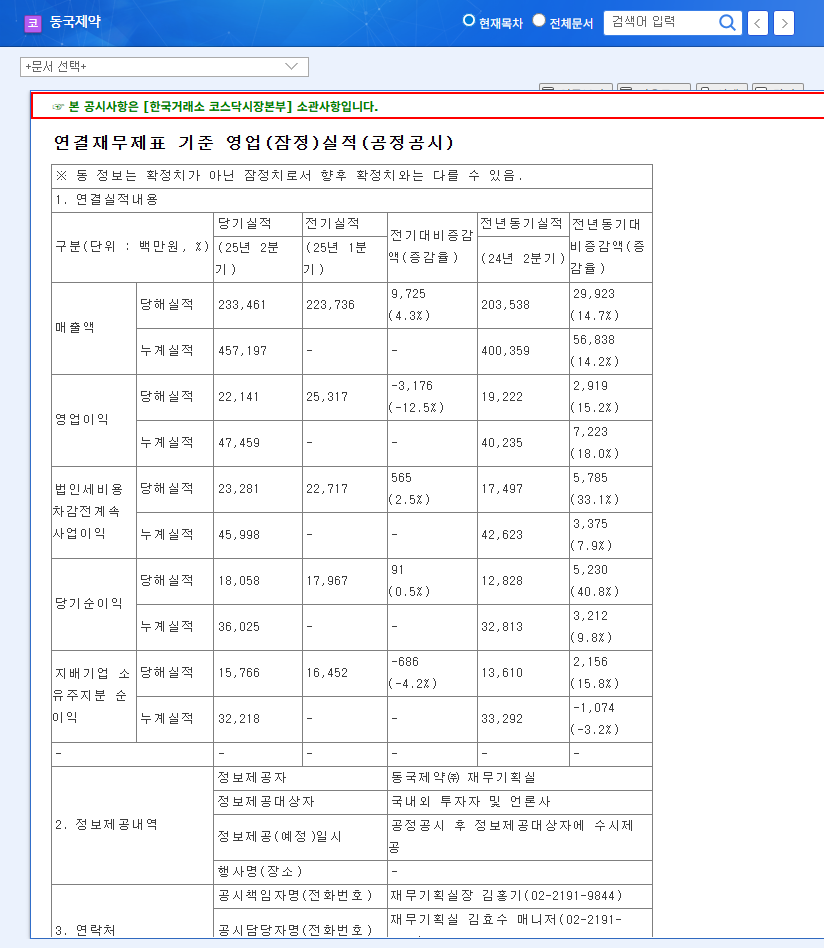

The most immediate concern is the company’s recent performance. DongKook Pharmaceutical’s first-half 2025 report revealed a revenue of 442.2 billion KRW, a sharp 45.6% decrease year-over-year. This downturn was primarily linked to sluggish exports in its intravenous fluid sector. Such a significant revenue drop could have been a key trigger for VIP Asset Management’s decision, signaling short-term growth challenges.

2. Strategic Portfolio Rebalancing

It’s also crucial to consider that the sale might be less about DongKook Pharmaceutical’s failures and more about VIP’s internal strategy. Asset managers constantly rebalance their portfolios to lock in profits, manage risk, or reallocate capital to sectors they believe have higher growth potential. The VIP Asset Management sell-off could simply be a prudent move to adjust their exposure within the healthcare industry.

3. Macroeconomic Headwinds

The broader economic climate cannot be ignored. Rising interest rates in major economies, as reported by sources like Reuters, increase borrowing costs and can dampen corporate investment. Furthermore, volatility in the USD/KRW and EUR/KRW exchange rates directly impacts the profitability of DongKook’s overseas operations, adding another layer of risk to the investment thesis.

“For investors, the key is to separate the signal from the noise. Is the VIP sell-off a predictive signal of long-term decline, or is it market noise that creates an entry point for those focused on the underlying value?”

Deep Dive: DongKook Pharmaceutical Stock Fundamentals

To form a sound investment opinion, we must look past the headline event and analyze the core business segments and financial health of DongKook Pharmaceutical.

Business Segment Performance

- •Over-the-Counter (OTC) Drugs: This remains a fortress for the company. Iconic brands like ‘Insadol’ and ‘Madecassol’ boast powerful brand equity and a loyal customer base, providing a stable revenue stream.

- •Ethical (Prescription) Drugs: While the intravenous fluid sector is currently a pain point, the company is actively pursuing growth through new drug development. Recovery in this segment is a key catalyst to watch.

- •Healthcare Division: The ‘Centellian24’ cosmetics brand is the star performer, showing robust growth and acting as a primary driver towards the company’s ambitious goal of 1 trillion KRW in total sales.

Financial Health & R&D Investment

Financially, the company maintains a solid foundation with consistently increasing total equity. However, there are yellow flags: rising accounts receivable and inventories could put pressure on cash flow. Despite the revenue downturn, DongKook has commendably maintained its investment in R&D. This commitment to innovation is a crucial positive sign, demonstrating a focus on securing future growth engines, a key topic in our guide to pharmaceutical stock investing.

Investment Outlook & Final Verdict (Hold)

Considering the short-term headwinds from the institutional sell-off and weak H1 2025 earnings, immediate upward momentum for DongKook Pharmaceutical stock seems unlikely. However, the company’s long-term potential remains intact due to its diversified business, strong brands, and R&D pipeline. Therefore, a ‘Hold’ rating is appropriate.

- •Positive Factors: Dominant OTC brands, high-growth healthcare division, continuous R&D investment, and sound financial base.

- •Negative Factors: Weakened investor sentiment, H1 revenue decline, potential cash flow pressures, and macroeconomic uncertainty.

Investors should closely monitor H2 2025 earnings for a recovery in the intravenous fluid sector, track any further stake changes by VIP Asset Management, and watch for progress in the company’s R&D pipeline.

Leave a Reply