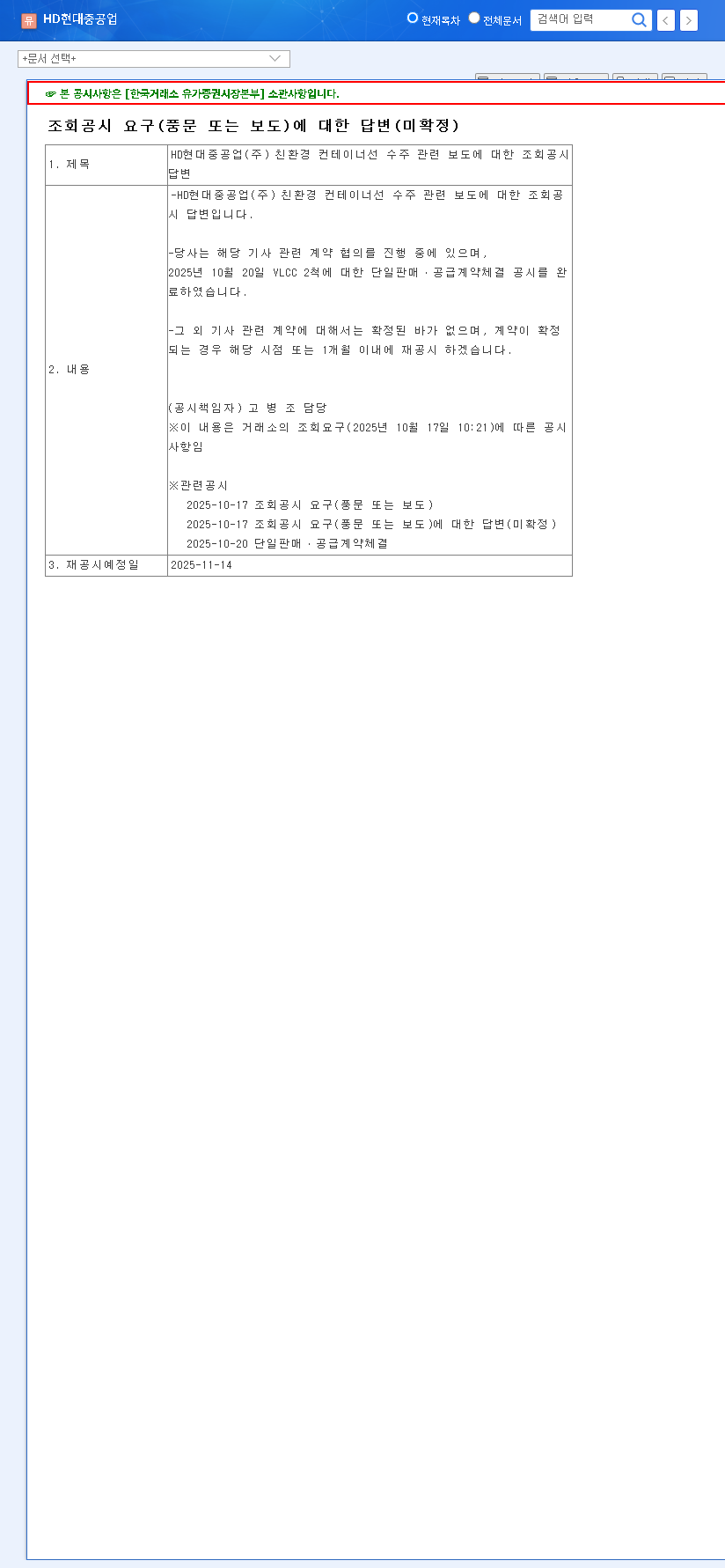

On November 3, 2025, the global investment community will turn its attention to HD HYUNDAI HEAVY INDUSTRIES CO.,LTD. (329180) as it holds its pivotal Investor Relations (IR) conference for the Q3 2025 management performance. This event is far more than a simple financial report; it offers a critical look into the company’s future. The upcoming HD Hyundai Heavy Industries Q3 earnings announcement will reveal crucial details about its strategies for navigating global economic headwinds and persistent shipping market volatility. For investors, this is an essential opportunity to gauge the health and direction of one of the world’s shipbuilding giants.

The central question is whether the company can sustain its trend of improving profitability, even as revenues have faced downward pressure. This deep-dive HD HHI investment analysis will dissect the key factors shaping Q3 performance and outline what stakeholders must watch for during the IR presentation. You can view the Official Disclosure (DART) for preliminary information.

Analyzing the HD Hyundai Heavy Industries Q3 Earnings Preview

Scheduled for November 3, 2025, at 2 PM KST, the IR conference will consist of an earnings presentation and a Q&A session. This direct line to management is invaluable for investors seeking clarity on corporate strategy and operational performance. The first half of 2025 set a complex stage: while revenue declined 44.6% year-on-year, operating profit impressively rose by 28.4%, signaling a strategic focus on profitability over pure volume.

The key narrative for the Q3 earnings report will be the sustainability of this profitability improvement. Can HD Hyundai Heavy Industries continue to enhance margins by prioritizing high-value, eco-friendly vessel orders against the backdrop of a potential global slowdown in new shipbuilding contracts?

Performance Deep-Dive by Business Segment

To form a complete picture, a granular look at each of the company’s core divisions is necessary. Each segment faces unique challenges and opportunities that will collectively shape the Q3 results.

Shipbuilding: The Engine of Growth and Profit

The demand for eco-friendly vessels, such as those powered by LNG, methanol, and ammonia, remains a significant tailwind. This trend, combined with the need to replace aging global fleets, provides a solid foundation. However, the dip in new orders seen in H1 could impact Q3 figures. Investors should focus on how effectively the company is translating its robust order backlog into recognized revenue and whether the margins on these advanced ships are holding strong.

Offshore Plant & Renewable Energy

The Offshore Plant division’s return to profitability is a major positive. More importantly, its strategic expansion into renewable energy—particularly floating offshore wind platforms—represents a vital long-term growth driver. This diversification reduces reliance on the cyclical shipbuilding market and positions the company to capitalize on the global energy transition. For a broader view, read about the trends shaping the global offshore energy sector.

Engine & Machinery: A Stable Foundation

This division provides a stable revenue stream thanks to its competitive advantage in eco-friendly and alternative fuel engines. As maritime regulations tighten, the demand for engines that can run on cleaner fuels will only increase, solidifying this segment’s importance to the company’s overall financial health and market leadership.

Financial Health & Macroeconomic Headwinds

While operational performance is key, the company’s financial structure and the external market environment are equally critical. A high debt ratio continues to be a point of concern for investors, though the significant improvement in the interest coverage ratio (a measure of a company’s ability to handle its debt payments) is a reassuring sign. The Q3 announcement should provide clear details on debt management and future funding strategies.

External factors add another layer of complexity. As detailed by financial experts at authoritative sources like Bloomberg, variables such as currency exchange rates, interest rate policies, and raw material costs (like steel) can significantly impact profitability. Furthermore, shipping freight indices, which have recently shown weakness, could dampen sentiment and affect new vessel orders.

Investor Action Guide: 5 Key Indicators for the IR Call

When analyzing the HD Hyundai Heavy Industries Q3 earnings report, investors should critically evaluate the following five points to make an informed decision about the HD Hyundai Heavy Industries stock:

- •Revenue Trajectory: Are there signs of revenue stabilization or a rebound? Look for specifics on construction schedules and order conversion.

- •Profitability Strength: Is the company maintaining or improving operating margins? Assess the impact of cost controls and the high-value order mix.

- •New Business Progress: What are the tangible results and future outlook for high-growth areas like offshore wind and Small Modular Reactors (SMRs)?

- •Future Order Outlook: What is management’s forecast for the global shipbuilding market, and what is their strategy to win new contracts?

- •Financial Deleveraging: Are there concrete plans to reduce the high debt ratio and strengthen the balance sheet?

In conclusion, while the ‘Neutral’ investment opinion reflects a balance of strong positive factors (market leadership, diversification) and significant risks (economic slowdown, high debt), the upcoming IR is a moment of truth. A thorough analysis of the company’s performance against these key indicators will be essential for any investor looking to make a strategic move.

Leave a Reply