The recent large-scale divestment by a major shareholder has sent ripples through the investment community, putting JAEYOUNG SOLUTEC stock under the microscope. On October 24, 2025, an official disclosure revealed that Murim Capital/Republic of Korea sold a significant portion of its holdings, raising critical questions about the company’s future. For current and prospective investors, understanding the implications of this move is paramount. What does this sale signal about the company’s health, and what is the strategic path forward for those with capital at stake?

This comprehensive JAEYOUNG SOLUTEC analysis will dissect the shareholder sale, evaluate the company’s underlying fundamentals, and provide a clear, actionable plan. We will explore both the immediate market reaction and the long-term strategic challenges, offering crucial insights to guide your investment decisions.

The Divestment Event: A Closer Look

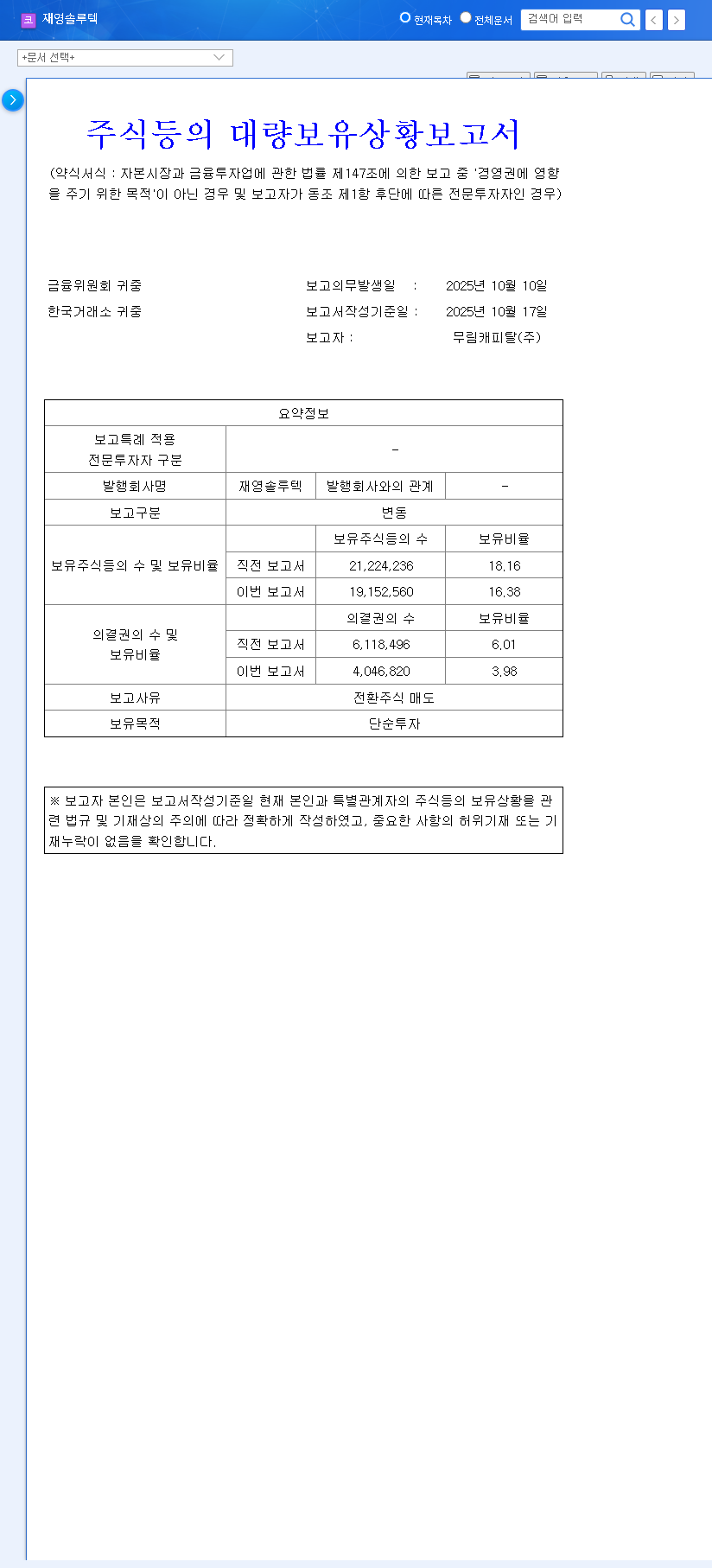

The pivotal event occurred when JAEYOUNG SOLUTEC’s major shareholder, ‘Murim Capital/Republic of Korea’, executed a significant sell-off. According to the Official DART Disclosure, the entity sold 4,046,820 common shares through open market transactions. These shares were newly converted from convertible bonds, a detail that adds another layer of complexity. This sale reduced their total stake in the company from 16.38% down to 12.92%. Such a large transaction from an informed party is a signal the market cannot ignore.

Company Fundamentals: The Core Business Under Pressure

To understand the context of the sale, we must examine the company’s financial and operational health. Based on the H1 2025 semi-annual report, JAEYOUNG SOLUTEC presents a mixed but concerning picture.

Profitability and Business Structure

While top-line revenue grew by a respectable 17.7% year-on-year, this growth did not translate to the bottom line. Operating profit saw a significant decline, pushing the company into a net loss. The strategic pivot to concentrate on the nano-optics division, which produces key actuators for smartphone cameras, is a high-stakes bet. The discontinuation and sale of the legacy mold business incurred one-off costs that have heavily impacted recent profitability metrics.

Financial Health and Debt

The company’s balance sheet is a key area of concern. Although the debt-to-equity ratio has improved slightly to 168.53%, it remains high for the industry. A significant overhang exists from outstanding convertible bonds, which can lead to future share dilution and financing costs. Investors considering a JAEYOUNG SOLUTEC investment must be aware of this financial burden. For more information on these complex financial instruments, read our guide on understanding convertible bonds.

A major shareholder sale, especially of shares converted from debt instruments, often signals a lack of confidence in the company’s near-term ability to generate cash flow and improve profitability.

Impact of the Shareholder Sale on JAEYOUNG SOLUTEC Stock

Short-Term: Heightened Stock Price Pressure

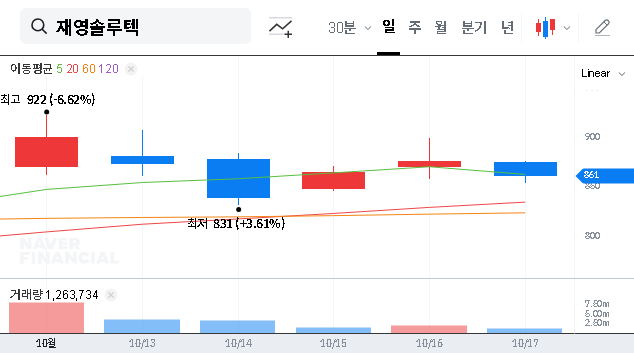

The immediate effect of this news is almost certainly negative. A large supply of shares hitting the market creates downward pressure on the JAEYOUNG SOLUTEC stock price. This is amplified by weakened investor sentiment, as the market interprets the sale as an insider’s bearish outlook. The fact that these were freshly converted shares suggests a desire to exit the position, raising concerns about further selling pressure in the near future.

Long-Term: Questions of Governance and Recovery

While the sale was by an investment association and not a core member of management, a reduced major shareholder stake can introduce uncertainty. The key long-term question is whether the company’s strategic focus on nano-optics can offset its financial weaknesses. The market will be watching closely to see if management can execute its turnaround plan and restore faith in the company’s fundamental competitiveness. A failure to do so could lead to a protracted decline.

Investor Action Plan & Strategic Outlook

Given the circumstances, a disciplined and cautious approach is essential. The JAEYOUNG SOLUTEC shareholder sale acts as a major red flag that must be weighed against any potential for future growth.

Investment Thesis & Key Monitorables

- •Short-Term (1-3 Months): A ‘Hold’ or ‘Sell’ rating is prudent. The risk of further price decline is high. Avoid new positions until the selling pressure subsides and a clear price floor is established.

- •Mid-to-Long-Term (6-18 Months): A cautious, ‘Wait-and-See’ approach is advised. Before considering an investment, look for tangible proof of a turnaround. This includes at least two consecutive quarters of positive operating profit and a measurable increase in market share for the nano-optics division.

Primary Risk Factors to Consider

- •Additional Divestments: The remaining 12.92% stake could be sold, creating another supply shock.

- •Competitive Pressure: The nano-optics market is highly competitive. Failure to innovate could erode margins.

- •Macroeconomic Headwinds: Global economic shifts can impact demand for smartphones, directly affecting JAEYOUNG’s core business. For context, see the latest market analysis from authoritative sources like Bloomberg.

- •Financial Instability: The high debt load and remaining convertible bonds pose an ongoing risk to financial stability.

In conclusion, while the potential for a turnaround exists within JAEYOUNG SOLUTEC’s focused strategy, the major shareholder sale is a significant bearish signal. Investors should prioritize capital preservation and demand clear evidence of fundamental improvement before committing to the stock.

Disclaimer: This analysis is for informational purposes only and is based on publicly available data. All investment decisions should be made with the consultation of a qualified financial advisor.

Leave a Reply