In a challenging climate for the construction industry, Nam Hwa Construction Company, Limited has delivered a significant piece of positive news that has caught the attention of investors. The company recently announced it has secured a major ₩7.7 billion contract, a move that could signal a pivotal turnaround. This development, coupled with signs of improving financial fundamentals, warrants a closer look. This in-depth analysis will explore the ripple effects of this new contract on Nam Hwa Construction stock, its corporate value, and its position within the broader construction market outlook.

This new contract is more than just a number; it’s a testament to Nam Hwa Construction’s resilience and capability. For investors, it represents a critical data point in evaluating the company’s trajectory in a volatile market.

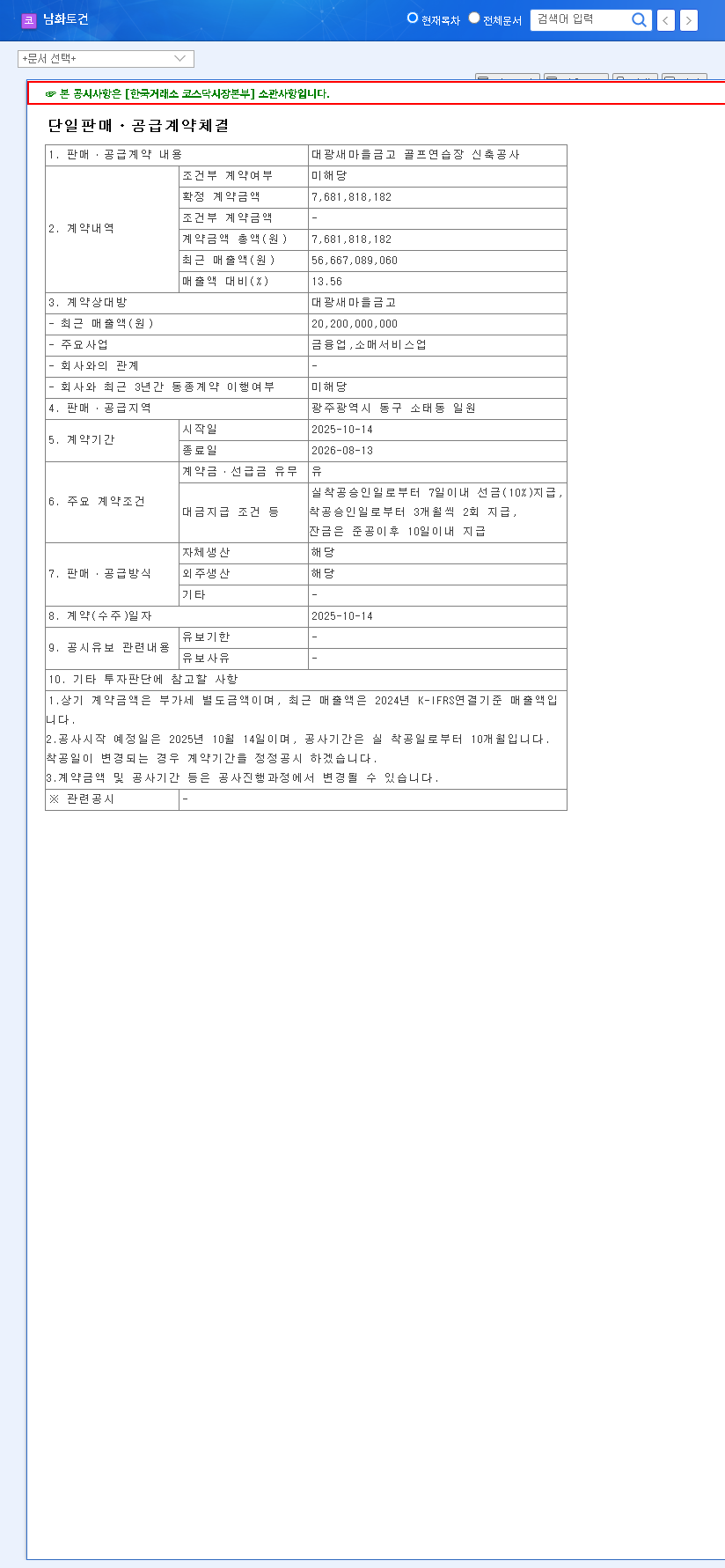

Unpacking the ₩7.7 Billion Golf Driving Range Contract

The cornerstone of this analysis is the new ‘Golf Driving Range Construction Project’ contract signed with Daegwang Saemaul Geumgo. Valued at precisely ₩7.7 billion, this project is not a minor win. It represents a substantial 13.56% of the company’s 2024 annual revenue and an even more impressive 26.4% of its first-half 2025 revenue. The project is set to run for approximately 10 months, from October 14, 2025, to August 13, 2026. For verification and further details, the company’s Official Disclosure (DART Report) provides complete transparency. This golf driving range contract diversifies their portfolio into the leisure and recreation sector, a potentially resilient area of construction.

Financial Health: A Deep Dive into Nam Hwa Construction’s Fundamentals

Profitability Amidst Revenue Headwinds

According to its latest semi-annual report, Nam Hwa Construction posted consolidated revenue of ₩29.156 billion for H1 2025, a decrease from the prior year. However, the more crucial story is the successful pivot to profitability. The company reported an operating profit of ₩198.59 million, a significant achievement that showcases improved operational efficiency and cost management. This ability to generate profit even with lower revenue is a strong indicator of a well-managed enterprise. For a deeper understanding of such metrics, investors can review our guide on Analyzing Construction Company Financials.

Stellar Financial Stability

A company’s ability to weather economic storms is often reflected in its balance sheet. Here, Nam Hwa Construction shines. Its debt-to-equity ratio has been on a steady decline, reaching a very stable 12.52% by the end of 2024. This low leverage means the company is less vulnerable to interest rate hikes and has greater flexibility to finance future growth without taking on excessive risk. This robust financial footing provides a solid foundation for taking on new, ambitious projects.

The Broader Construction Market Outlook

No company operates in a vacuum. The broader construction market outlook presents both challenges and opportunities for Nam Hwa Construction.

- •Market Slowdown: The sector has been grappling with a slowdown in orders and investments since 2023. While some analysts, like those at leading economic institutes, project a potential recovery in late 2025, risks from reduced government SOC (Social Overhead Capital) budgets remain a concern.

- •Material & Currency Volatility: A fluctuating KRW/USD exchange rate can impact the cost of imported raw materials. While Nam Hwa’s limited overseas exposure mitigates direct currency risk, global oil price shifts can still affect domestic transportation and material costs.

- •Interest Rate Environment: The prospect of future interest rate cuts by central banks in both the U.S. and Korea is a significant tailwind. Lower rates would reduce financing costs for new projects, potentially stimulating investment across the entire construction sector.

Investment Thesis: Evaluating the Nam Hwa Construction Stock

The announcement of this contract could act as a powerful short-term catalyst for Nam Hwa Construction stock. When combined with the fundamental strength shown by the profit turnaround, it’s likely to boost investor sentiment. However, a prudent investor must look beyond the immediate headlines.

The long-term growth story depends on several factors:

- •Execution Excellence: Successfully delivering the golf driving range project on time and within budget is paramount to reinforcing the company’s reputation.

- •Sustained Order Flow: This single contract, while significant, cannot single-handedly reverse the broader revenue trend. The company must demonstrate an ability to consistently win new, high-quality projects.

- •Market Recovery: The company’s performance will ultimately be tied to the health of the overall construction industry. A market tailwind would provide a substantial lift.

Conclusion: An Action Plan for Investors

The ₩7.7 billion contract secured by Nam Hwa Construction is an unequivocally positive development, reinforcing its business continuity and operational strength. It serves as a beacon of potential in a murky market. However, investors should maintain a balanced perspective, weighing this single win against the broader industry uncertainties. Moving forward, the key to unlocking long-term value will be the company’s ability to build on this momentum, manage project profitability, and navigate the macroeconomic landscape. Astute investors should keep a close watch on future contract announcements and quarterly earnings reports to track the company’s progress.

Leave a Reply