The latest ABLE C&C quarterly dividend announcement has captured the market’s attention, signaling a commitment to shareholder returns. However, for savvy investors, this news is just the tip of the iceberg. Below the surface of a 76 KRW per share payout lies a complex financial landscape shaped by declining revenue, strategic cost-cutting, and a volatile macroeconomic environment. This comprehensive ABLE C&C stock analysis will dissect the H1 2025 report to uncover whether this dividend is a sign of genuine strength or a short-term gesture amid long-term challenges.

Is the dividend a reward for robust performance, or a strategic move to bolster investor confidence? We peel back the layers to provide a clear, actionable perspective on ABLE C&C’s future.

The Dividend Decision: Key Details

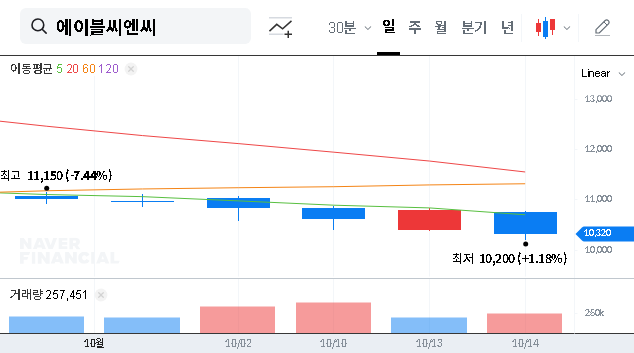

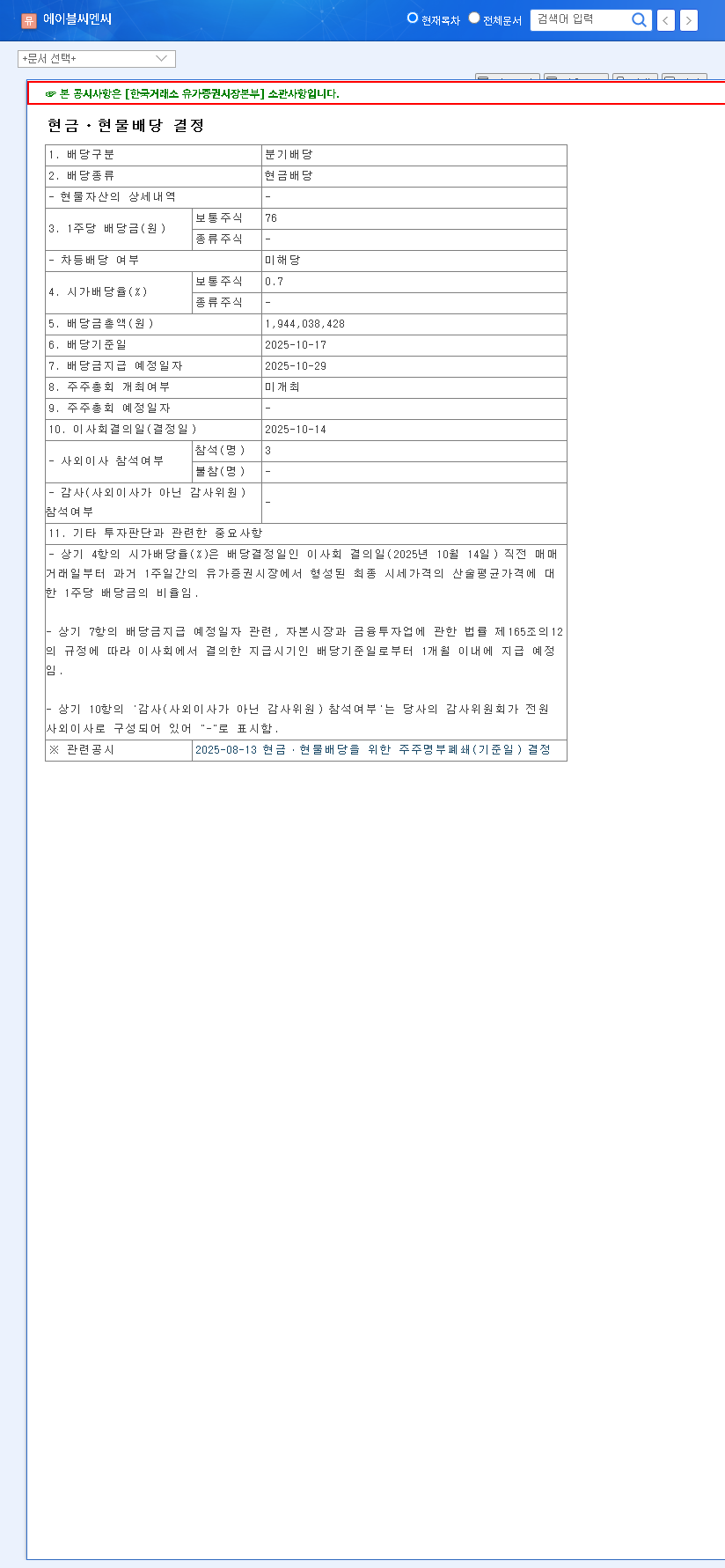

On October 14, 2025, ABLE C&C (078520) confirmed a quarterly dividend of 76 KRW per common share. Based on the stock price of 10,790 KRW at the time of announcement, this represents a dividend yield of approximately 0.7%. While modest, this consistent return of capital is a positive signal. The full details of this announcement were made public in an official filing. (Source: Official DART Disclosure)

In-Depth Fundamental Analysis (H1 2025)

To understand the true implications of the ABLE C&C quarterly dividend, we must analyze the company’s underlying financial and operational health. The H1 2025 report reveals a mixed but telling picture.

Financial Status: A Tale of Two Metrics

The most striking paradox in ABLE C&C’s financials is the divergence between revenue and profit. H1 2025 revenue fell by 3.4% year-on-year to 127.977 billion KRW, a direct result of a cooling global beauty market and fierce competition. However, operating profit surged by an impressive 21.1% to 12.428 billion KRW. This profitability boost stems from aggressive cost management and efficiency improvements, not top-line growth. While commendable, it raises questions about long-term sustainability.

Deeper financial health indicators warrant caution. The debt-to-equity ratio sits at 70.22%, a level that requires careful management, especially as borrowing increases. For a detailed explanation, you can review Investopedia’s guide on the Debt-to-Equity ratio. Furthermore, a declining current ratio (185.40%) and slowing inventory turnover (2.5 times) suggest potential pressures on short-term liquidity and operational efficiency.

Business Environment and Strategic Pivots

ABLE C&C is not standing still. The company is actively seeking new growth avenues, such as entering the medical device sales and leasing market. It’s also strengthening its digital presence and distribution through H&B stores and platforms like Daiso to capture the crucial MZ generation (Millennials & Gen Z). Globally, expansion continues, but a strategic diversification away from the uncertain Chinese market is paramount. These moves, combined with a focus on ESG management, are positive steps toward building a more resilient business model. For more on company strategies, you can explore our internal guide on competitive analysis.

Macroeconomic Headwinds and Stock Performance

The 078520 stock price has reflected these underlying tensions, fluctuating between 6,000 and 8,000 KRW in H1 2025. This performance is influenced by several external factors. A strengthening KRW/USD exchange rate could boost the value of overseas earnings, but persistent high interest rates increase borrowing costs and can dampen investor sentiment. Additionally, rising oil and commodity prices threaten to inflate raw material and logistics costs, potentially squeezing the profit margins that the company has worked so hard to improve.

Investment Thesis: A Balanced Outlook for ABLE C&C

The quarterly dividend is a positive gesture, but the core investment thesis for ABLE C&C hinges on its ability to navigate significant challenges. Historically, periods of revenue decline have correlated with stock price drops, a pattern that warrants close observation.

- •Positive Catalysts: Continued operational efficiency, successful penetration of new markets (both geographic and product-based), and favorable currency movements could drive profitability and improve sentiment.

- •Significant Risks: Failure to reverse the revenue decline is the primary risk. Worsening financial health metrics, uncertainty in new business ventures, and a sustained high-interest rate environment pose substantial threats to the company’s bottom line.

Frequently Asked Questions (FAQ)

Q1: What is the real impact of ABLE C&C’s dividend on my investment?

The dividend signals a commitment to shareholders and can provide a small, regular return. However, at a ~0.7% yield, its direct financial impact is minimal. Its true value is as a confidence signal, which must be weighed against the fundamental challenges outlined in this ABLE C&C stock analysis.

Q2: What is the biggest red flag in the ABLE C&C financial status?

The biggest red flag is the combination of declining revenue with worsening liquidity ratios (e.g., the current ratio). Profit growth driven solely by cost-cutting is not sustainable if sales continue to fall. This pressure on both the top line and the balance sheet is the most critical area to monitor.

Q3: What should I watch for in the coming quarters?

Focus on revenue trends above all else. Look for signs of stabilization or growth from new product launches, online channel expansion, and overseas performance. Additionally, track any improvements in the debt-to-equity ratio and inventory turnover, as these will indicate better financial and operational management.

Leave a Reply