KOMIPHARM INTERNATIONAL CO., LTD. recently announced a pivotal development that has caught the attention of investors monitoring KOMIPHARM stock. The company secured a $6.1 million supply contract for its flagship Foot-and-Mouth Disease (FMD) vaccine, PRO-VAC FMD, with South Korea’s Public Procurement Service. This deal, representing over 10% of recent semi-annual revenue, raises critical questions: Is this the catalyst needed to reverse declining revenues and ignite sustainable growth? This analysis will dissect the contract’s implications for the company’s fundamentals, its stock price, and the long-term investment thesis.

This contract is more than just a revenue boost; it’s a validation of KOMIPHARM’s technology and a stabilizing force as the company navigates the high-stakes world of human drug development.

Deconstructing the $6.1 Million KOMIPHARM Contract

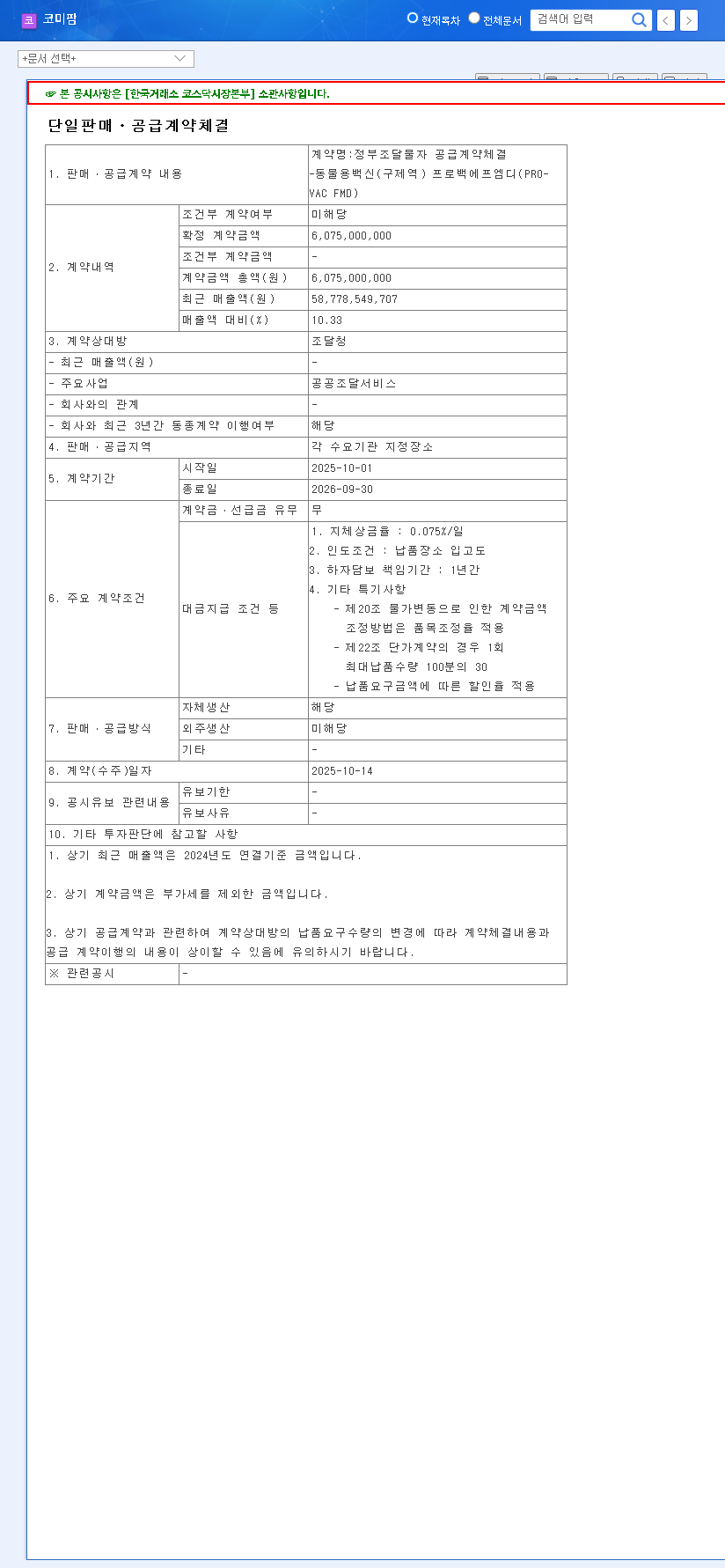

On October 14, 2025, KOMIPHARM formalized a significant agreement to supply its PRO-VAC FMD vaccine. This development was confirmed in an Official Disclosure filed with the Financial Supervisory Service. The contract, valued at approximately $6.1 million, extends for one year, from October 1, 2025, to September 30, 2026. The counterparty, the Public Procurement Service, is a centralized government agency, making this a prestigious and reliable revenue stream. Foot-and-Mouth Disease is a severe and highly contagious viral disease affecting livestock, with significant economic consequences, making robust vaccine programs a national priority. For more information on FMD, you can consult authoritative sources like the World Organisation for Animal Health.

Fundamental Impact: A Two-Pronged Analysis

1. Immediate Financial Fortification

The financial implications of this KOMIPHARM contract are direct and positive. Against the backdrop of a 13% year-over-year revenue decline in H1 2025, this injection of $6.1 million is a welcome development. It provides a much-needed boost to the top line and is expected to enhance both profitability and operating cash flow.

- •Revenue Stabilization: The contract represents 10.33% of H1 2025 revenue, directly counteracting recent downward trends and ensuring a stable sales foundation from a flagship product.

- •Profitability Boost: The animal pharmaceuticals division is already a profitable segment for KOMIPHARM. This high-volume government contract is likely to carry healthy margins, contributing positively to the bottom line.

- •Improved Cash Flow: Predictable revenue from a government entity strengthens the company’s cash position, which is crucial for funding ongoing R&D operations.

2. Strategic Business & Market Positioning

Beyond the numbers, this contract solidifies KOMIPHARM’s reputation and market leadership in the animal pharmaceuticals space. Winning a competitive government tender validates the quality and efficacy of the PRO-VAC FMD vaccine. This enhances brand credibility, which can be leveraged for further domestic and international expansion. This stable revenue base also provides crucial, non-dilutive funding for the company’s more ambitious—and riskier—ventures in human therapeutics.

The Long-Term Growth Engine: KomiNOX (PAX-1)

While the FMD vaccine contract is excellent news, the ultimate trajectory of KOMIPHARM stock hinges on its human new drug pipeline, specifically ‘KomiNOX’ (PAX-1). This candidate is being investigated as a novel cancer therapy. The success or failure of KomiNOX represents a binary event that could either trigger exponential growth or lead to significant investor disappointment. The stable income from the animal health division acts as a financial bridge, allowing the company to pursue this high-reward research without excessive reliance on capital markets. Investors interested in this area should explore our guide to investing in clinical-stage biotech companies.

Investment Outlook & Key Risks

This contract is expected to provide a short-term positive lift to investor sentiment and the stock price. However, a comprehensive KOMIPHARM investment thesis must balance this operational win with the broader risk profile.

Key Considerations for Investors

- •Positive Tailwinds: Secured revenue, enhanced credibility, and a temporary buffer against recent financial weakness.

- •Significant Headwinds: The immense clinical and regulatory uncertainty surrounding KomiNOX remains the primary risk. The high cost of R&D continues to be a major cash drain.

- •Macro-Economic Factors: Fluctuations in currency exchange rates and the cost of raw materials can impact profit margins and must be monitored.

In conclusion, the $6.1M contract is a solid operational victory that strengthens KOMIPHARM’s foundation. It provides short-term stability and reinforces its market leadership in animal vaccines. However, investors must recognize that the company’s long-term valuation is inextricably linked to the high-risk, high-reward development of its human drug pipeline. This contract makes the journey safer, but the destination remains uncertain.

Frequently Asked Questions (FAQ)

Q1: How significant is the $6.1M contract for KOMIPHARM’s revenue?

A1: It is quite significant, representing about 10.33% of the company’s H1 2025 revenue. It provides a direct and immediate boost to the top line and helps stabilize sales after a period of decline.

Q2: How does this deal affect the KOMIPHARM stock price outlook?

A2: In the short term, the news is a positive catalyst that can improve investor sentiment. However, the long-term stock performance will likely be driven more by progress and clinical trial results for its human drug candidate, KomiNOX.

Q3: What are the main risks for a KOMIPHARM investment?

A3: The primary risk is the high degree of uncertainty associated with the development of its human new drug, KomiNOX, coupled with the substantial R&D costs. Macroeconomic factors like currency and material cost volatility are secondary risks.

Leave a Reply