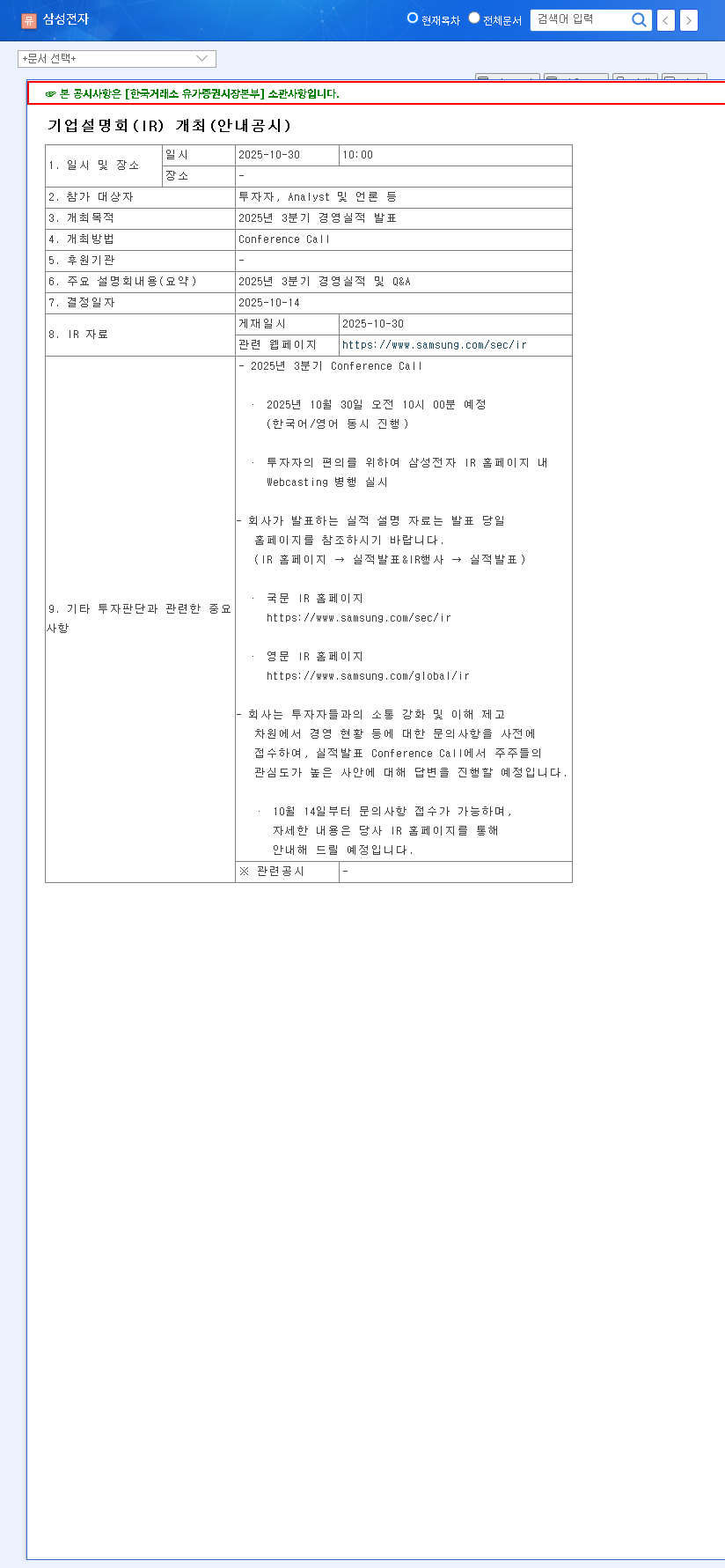

The entire tech world is holding its breath for the upcoming Samsung Q3 2025 earnings announcement on October 30, 2025. This isn’t just another financial report; it’s a critical barometer for the health of the global semiconductor industry and a definitive test of Samsung’s strategy in the burgeoning AI era. After a challenging first half of the year, investors, analysts, and competitors are all asking the same question: can Samsung’s dominance in AI chips and mobile technology spark a powerful turnaround?

This comprehensive preview delves into the key factors shaping Samsung’s performance, analyzing its divisional strengths and weaknesses, the macroeconomic headwinds, and the potential scenarios that could unfold. Our analysis is based on market data and the company’s official semi-annual report. You can view the Official Disclosure on DART for source data.

The core narrative for Samsung’s Q3 earnings hinges on a single, crucial battle: Can the explosive growth in the AI-focused Device Solutions (DS) division overcome the persistent global economic uncertainties and propel the company back to its expected profitability?

Recap: A Challenging First Half in 2025

To understand the stakes for the Samsung Q3 2025 earnings report, we must first look at the preceding period. The first half of 2025 painted a mixed picture. While overall revenue saw a modest increase of 5.3% year-over-year to KRW 153.7 trillion, the bottom line told a different story. Operating profit plummeted by 33.2% to KRW 11.36 trillion. The primary culprit was the Device Solutions (DS) division—the semiconductor powerhouse—which saw its operating profit collapse by a staggering 86.7%.

Despite this profitability crunch, Samsung’s financial foundation remains solid, with total assets of KRW 504.8 trillion and a stable debt-to-equity ratio of 26.4%. However, the sharp decline in earnings per share (EPS) by 61.1% highlights the urgent need for a turnaround, placing immense pressure on the upcoming Q3 results.

Deep Dive: Business Division Performance & Outlook

Samsung’s future is a tale of several distinct business units, each with its own set of opportunities and challenges. Here’s what we’re watching for in the Q3 report.

DS (Device Solutions): The Engine for AI-Powered Recovery

This is the division everyone is focused on. Its performance will make or break the Samsung earnings preview. The key lies in high-value-added memory products.

- •Memory Chips: Demand for HBM3E (High Bandwidth Memory) and high-capacity DDR5 is surging, thanks to massive investments in AI servers and data centers by tech giants. Samsung’s ability to ramp up production and capture market share for these premium Samsung AI chips is the single most important growth driver. This is a crucial element in the wider semiconductor recovery narrative.

- •Foundry & System LSI: The push into advanced 2nm processes and the expansion into automotive semiconductors are positive long-term trends. However, geopolitical tensions, especially the US-China tech rivalry, could create demand uncertainty.

DX (Device eXperience): Stability Through Innovation

The DX division, which includes mobile phones and home appliances, provides crucial stability. While less volatile than the DS division, its performance is still vital.

- •Mobile: With 14 years as the global shipment leader, the Galaxy brand is a formidable force. The success of Galaxy AI features and the continued leadership in foldable devices are key to fending off intensifying competition in a stagnating market.

- •TVs & Appliances: Samsung’s 19-year reign in the TV market is set to continue with a focus on premium, super-large screens and AI integration. The home appliance segment faces headwinds from rising costs but benefits from a push towards eco-friendly, high-efficiency products.

Potential Scenarios for the Q3 Earnings Release

The Samsung Q3 2025 earnings announcement could lead the market in several directions depending on the results and forward guidance.

- •Bullish Scenario: Earnings significantly beat expectations. This would be driven by a faster-than-anticipated recovery in the DS division, with soaring HBM sales and strong pricing power. Combined with solid sales from the latest Galaxy devices, this could signal a powerful profit recovery for the rest of the year.

- •Neutral Scenario: Results land within the consensus range. This would indicate a gradual recovery is underway, but macroeconomic pressures and competition are preventing a breakout performance. The market may react calmly as this is largely priced in.

- •Bearish Scenario: A miss on revenue or profit guidance. This could be caused by a slower-than-expected rebound in semiconductor demand or weak consumer spending hitting the DX division. Such a result would raise concerns about the timeline of the semiconductor recovery.

Investor Takeaway: What to Watch For

For those conducting a Samsung stock analysis, the Q3 report and subsequent conference call will be filled with critical data points. Beyond the headline revenue and profit numbers, focus on:

- •DS Division Margins: Are profit margins in the semiconductor business improving? This is the clearest sign of a healthy recovery.

- •HBM & AI Chip Sales Commentary: Listen for management’s commentary on sales volume and future demand for their premium AI-related products.

- •Forward Guidance for Q4 and 2026: The outlook provided by the management team will be just as important as the Q3 results themselves, setting the tone for months to come.

- •Capital Expenditure Plans: Investment plans can signal confidence in future growth, particularly in building out advanced foundry capacity. For more background, review our guide on how to analyze tech earnings reports.

Ultimately, Samsung’s deep technological expertise and market leadership position it well for long-term growth. The Q3 2025 earnings will be a crucial checkpoint, offering the first clear glimpse into whether the AI-fueled recovery has truly taken hold.

Leave a Reply