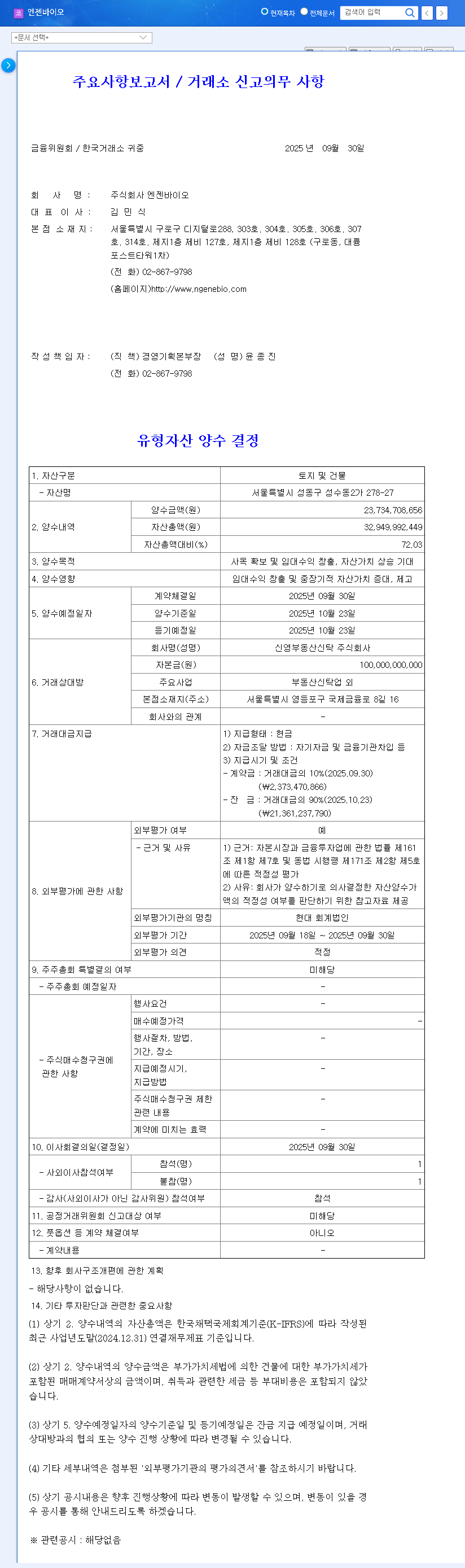

The recent EngeneBio HQ acquisition has sent ripples through the investment community. On September 30, 2025, the precision diagnostics company announced a monumental ₩23.7 billion deal for a new headquarters in the trendy, high-growth district of Seongsu-dong, Seoul. For a company navigating financial headwinds, this move is far more than a simple real estate transaction; it’s a bold declaration of intent. But does it represent a strategic masterstroke for long-term growth or a perilous gamble that could strain its resources to the breaking point?

This comprehensive analysis delves into the fundamentals of EngeneBio, dissects the potential impacts of this massive investment, and outlines the critical factors every investor must consider. We will explore whether this acquisition can truly secure a stable future or if it’s a financial burden in disguise.

The Landmark Deal: What We Know

EngeneBio (KOSDAQ: 354200) formalized its decision to acquire land and a building in Seongsu-dong 2-ga, Seongdong-gu, Seoul. The stated purpose is threefold: to establish a stable operational headquarters, generate ancillary rental income, and capitalize on the long-term appreciation of real estate assets in one of Seoul’s most coveted districts. According to the Official Disclosure (DART), the transaction is valued at ₩23.7 billion. The payment structure involves a 10% deposit paid upfront, with the remaining 90% due on October 23, 2025, funded through a combination of company capital and loans from financial institutions.

This acquisition represents a staggering 72.03% of EngeneBio’s total assets, a figure that underscores the magnitude of this commitment and the associated financial risks.

EngeneBio’s Financial Health: A High-Stakes Context

To understand the gravity of the EngeneBio HQ acquisition, one must examine the company’s current financial landscape. As of the first half of 2025, the company reported sales of ₩3.84 billion against an operating loss of ₩4.73 billion and a net loss of ₩9.12 billion. This persistent unprofitability highlights a core challenge: EngeneBio is a research-intensive firm with high R&D costs but has yet to achieve sustainable profitability. The company has actively raised capital through rights issues and convertible bonds to fuel its expansion, making this large, debt-financed acquisition a particularly noteworthy event. For more context on biotech financials, you can review market trends on platforms like Bloomberg.

A Double-Edged Sword: Potential Upsides vs. Downsides

This strategic move presents a classic risk-reward scenario. The potential benefits and drawbacks must be weighed carefully.

Positive Impacts (The ‘Masterstroke’ Argument)

- •Asset Value Appreciation: Seongsu-dong is a premier Seoul location, often compared to trendy, high-tech hubs globally. The long-term appreciation of this asset could significantly bolster EngeneBio’s balance sheet.

- •Operational Stability & Cost Savings: Owning headquarters eliminates rental volatility and provides a permanent base of operations, which can improve morale and long-term planning.

- •Enhanced Corporate Image: A prestigious address in Seongsu-dong enhances corporate credibility, potentially attracting top-tier talent and fostering stronger partnerships.

- •New Revenue Stream: Leasing unused space can generate a stable rental income, partially offsetting the acquisition’s cost and diversifying revenue sources.

Negative Impacts (The ‘Risky Gamble’ Argument)

- •Severe Financial Strain: The ₩23.7 billion price tag is a heavy burden for a loss-making company. Increased debt and interest payments could severely impact profitability and cash flow.

- •Opportunity Cost in R&D: This capital could have been invested directly into core R&D projects, such as its promising NGS-based diagnostics or AI drug discovery platforms. This diversion of funds could slow innovation. You can read our previous analysis of EngeneBio’s R&D pipeline here.

- •Cash Flow Deterioration: A large capital expenditure can deplete cash reserves needed for day-to-day operations, potentially forcing further capital raises under less favorable terms.

- •Macroeconomic Risks: The company becomes more exposed to interest rate hikes (affecting loan payments) and fluctuations in the commercial real estate market.

Investment Implications: What Investors Must Watch

The EngeneBio HQ acquisition fundamentally alters the company’s risk profile. Investors must shift their focus to monitor not just its biotech advancements but also its performance as a real estate asset manager. Key points to monitor include:

- •Funding Plan Execution: Scrutinize the final terms of the loans. A high interest rate could be crippling.

- •Rental Income Realization: Track how quickly EngeneBio secures tenants for excess space and at what rates. This is crucial for validating the financial model of the acquisition.

- •Core Business Performance: The company’s precision diagnostics and R&D pipelines must continue to advance. Any slowdown could indicate that the acquisition is distracting from the core mission.

- •Management’s Strategy: Pay close attention to leadership’s commentary on balancing real estate management with its primary biotech objectives.

In conclusion, EngeneBio’s bold move into Seongsu-dong is a pivotal moment. If executed flawlessly, it could provide a stable foundation and significant asset growth. However, given the company’s financial state, the margin for error is razor-thin. Investors should approach this with cautious optimism, demanding clear evidence that this significant financial risk will translate into tangible, long-term value for the company and its shareholders.

Leave a Reply