Protina’s $1.2 Billion Deal: Wings for Takeoff

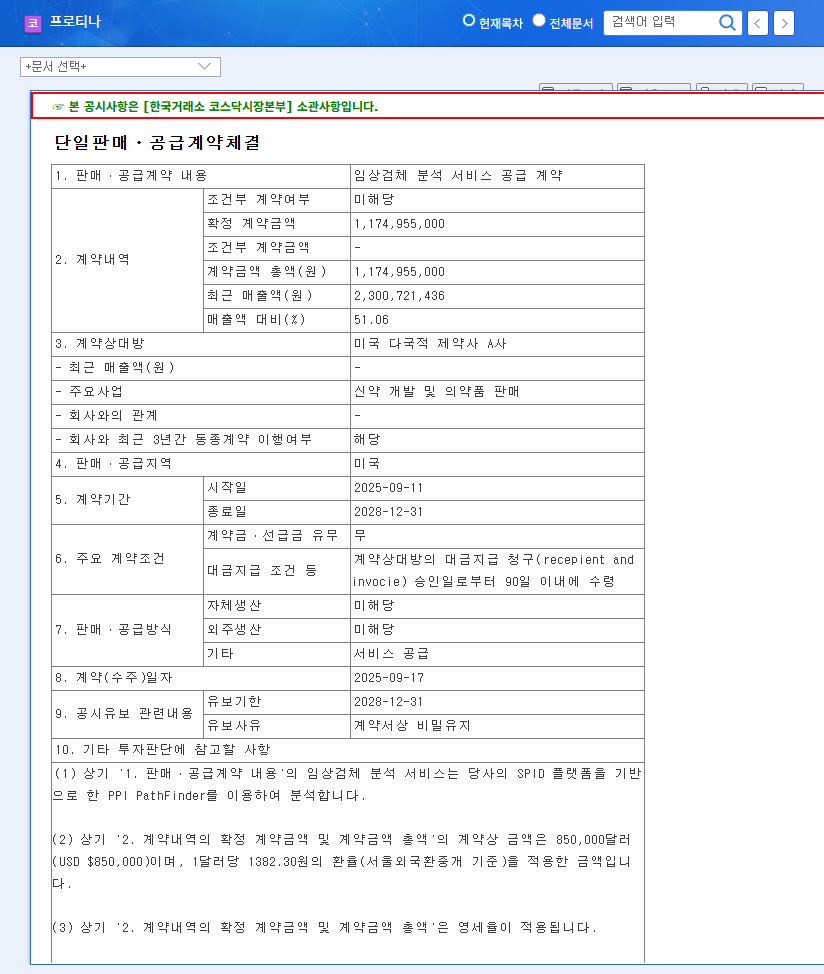

On September 17, 2025, Protina announced a substantial $1.2 billion contract with a leading US pharmaceutical company for the provision of clinical sample analysis services. The contract spans 3 years and 3 months, ending on December 31, 2028. This represents a significant portion (51.06%) of Protina’s first-half 2025 revenue ($2.025 billion) and is expected to contribute significantly to the company’s top-line growth.

Beyond the Deal: Strategic Implications

- Revenue Growth and Stability: The long-term $1.2 billion contract provides not only short-term revenue growth but also a stable revenue stream for the next three years.

- US Market Penetration: Partnering with a major US pharmaceutical player accelerates Protina’s entry into the lucrative US market and strengthens its brand recognition.

- Validation of SPID Platform: The deal serves as a strong validation of Protina’s core technology, the SPID platform, showcasing its competitiveness in the market.

- Positive Investor Sentiment: For a newly listed company, securing a large contract can boost investor confidence and create positive momentum for stock price appreciation.

Key Considerations for Investors

- Profitability: Investors should monitor whether the revenue growth translates into improved profitability.

- Currency Exchange Risk: Given the involvement of a US company, managing currency exchange rate fluctuations is crucial.

- Long-Term Growth Strategy: Assessing how this contract aligns with Protina’s overall long-term growth strategy is essential.

Protina: Poised for Global Bio Leadership?

This contract represents a pivotal moment for Protina, highlighting its significant growth potential. Continued monitoring of the company’s progress is warranted as it strives to become a global leader in the biopharmaceutical space.

Frequently Asked Questions

What is the value of the contract between Protina and the US pharmaceutical company?

$1.2 billion.

What is the duration of the contract?

3 years and 3 months, from September 11, 2025, to December 31, 2028.

Why is this contract significant for Protina?

It is expected to positively impact revenue growth, US market entry, technology validation, and investor sentiment.

What are the key investment considerations?

Investors should consider profitability improvements, currency exchange risks, and the company’s long-term growth strategy.

Leave a Reply