The potential SLL Central divestment has sent ripples through the market, placing its parent company, ContenTree Central (036420), at a critical crossroads. This move could either be a strategic masterstroke to heal its finances and unlock new growth or the loss of a vital growth engine that weakens its long-term competitive edge in the bustling K-content landscape. For investors, understanding the nuances of this situation is paramount.

This comprehensive ContenTree Central analysis will dissect the context of the proposed sale, evaluate the company’s current financial health, and explore the potential positive and negative impacts on the 036420 stock price. Our goal is to provide the detailed insights you need for informed investment decisions.

The Divestment Proposal: What’s on the Table?

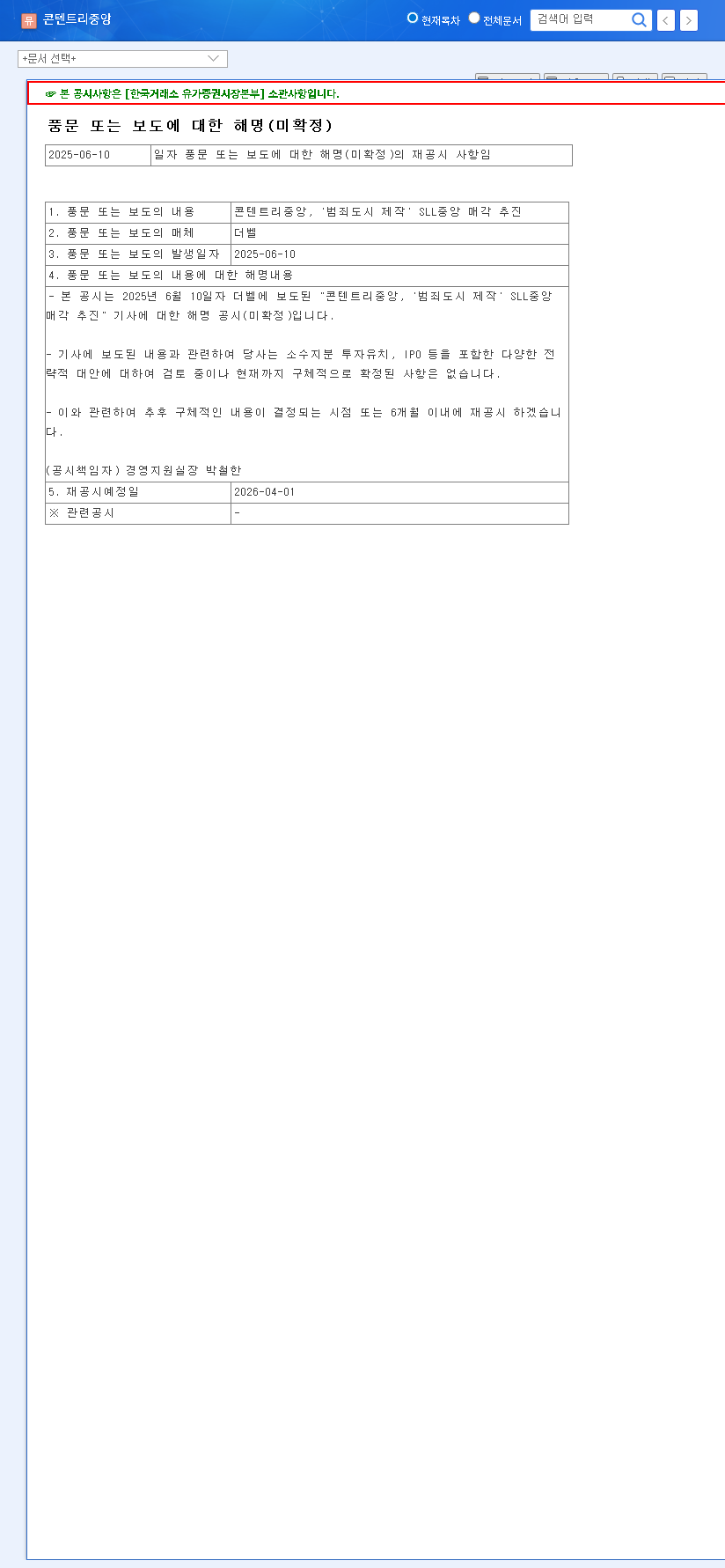

The news first broke on June 10, 2025, when reports suggested that ContenTree Central was actively pursuing the sale of SLL Central, the powerhouse production studio behind massive hits like the ‘The Outlaws’ series. This subsidiary is widely seen as a crown jewel in the company’s content portfolio.

In response, ContenTree Central issued a public disclosure, clarifying that while various strategic options—including attracting investment or pursuing an IPO for the subsidiary—were being considered, nothing had been finalized. The company has set a re-disclosure date of April 1, 2026, leaving the market in a state of anticipation. You can view the Official Disclosure (Source: DART) for their formal statement.

ContenTree Central Analysis: A Company Under Pressure

To understand why the SLL Central divestment is being considered, we must look at ContenTree Central’s current financial standing. While the company impressively achieved a turnaround to an operating profit of KRW 1.6 billion in H1 2025, significant underlying financial challenges remain.

Key Financial Health Indicators (H1 2025)

- •Soaring Debt Ratio: The company’s debt-to-equity ratio has climbed to a concerning 434.24%. While partly due to a decrease in capital rather than new borrowing, this high level signals significant financial risk.

- •Capital Erosion: A net loss of KRW 84.8 billion in the first half of the year has reduced total capital, further weakening the balance sheet.

- •Rising Financial Costs: Financial costs surged by 81.9% year-on-year, placing a heavy burden on profitability and cash flow, a trend exacerbated by the current high-interest-rate environment. For more context, see a recent report from Bloomberg on global interest rate impacts.

The Impact of the SLL Central Divestment

The sale of SLL Central is a double-edged sword, presenting both substantial opportunities and significant risks for the 036420 stock.

The Bull Case: A Path to Recovery

- •Financial Restructuring: A successful sale would inject a significant amount of cash, allowing the company to pay down debt, strengthen its balance sheet, and reduce crippling financial costs.

- •Strategic Refocus: Shedding a major subsidiary could allow management to concentrate resources on its core spatial business (like Megabox cinemas) and other strategic content ventures.

- •Value Revaluation: If SLL Central fetches a premium price, it could lead to a positive revaluation of ContenTree Central’s overall corporate worth, boosting investor confidence.

The Bear Case: Losing the Growth Engine

- •Weakened Competitiveness: SLL Central is a cornerstone of the company’s K-content production. Selling it could severely hamper its ability to compete in the global content arena, a key factor in K-content investment appeal. You can learn more in our guide to investing in the K-content industry.

- •Execution Risk: The deal is far from certain. A failed sale or a lower-than-expected valuation could crush investor sentiment and leave the company in a worse position.

- •Profitability Concerns: The divestment would create short-term profitability gaps and volatility as the company restructures its business segments.

Given the high degree of uncertainty surrounding the SLL Central divestment and its profound potential impact, a “Neutral” stance is warranted. Close monitoring of official disclosures and financial performance is critical for all current and prospective investors.

Investor FAQ: Key Questions Answered

Why is ContenTree Central considering selling SLL Central?

The primary driver is financial pressure. The company is grappling with a high debt ratio (434.24%), eroding capital, and soaring financial costs. Selling SLL Central is a strategic option to raise cash, pay down debt, and improve its overall financial stability.

How could this sale impact the 036420 stock price?

The impact could be significant in either direction. A successful, high-value sale could boost the stock on expectations of a healthier balance sheet. Conversely, uncertainty, a failed deal, or concerns over losing a core asset could lead to increased volatility and a negative price trend.

What are the key risks if the sale doesn’t happen?

If the deal falls through, ContenTree Central will still face its existing financial burdens. Investor confidence would likely drop, and the company would miss a crucial opportunity to de-leverage and secure funds for future growth, potentially leading to a negative re-rating of the stock.

Disclaimer: This analysis is for informational purposes only and is based on publicly available data. It does not constitute investment advice. All investment decisions should be made at the investor’s own discretion and responsibility.

Leave a Reply