The recent management stabilization at Youngone Trade Holdings represents a pivotal moment for the company and its investors. A significant shift in shareholding has solidified control, but this development arrives amidst a complex financial landscape. While H1 2025 saw impressive revenue growth, underlying profitability issues, particularly within the SCOTT business unit, pose significant questions. This comprehensive investment analysis will dissect these events, offering a clear perspective on the future trajectory of Youngone Trade Holdings and what it means for your investment strategy.

With newfound management stability, Youngone Trade Holdings has a clear runway for strategic execution. The key question for investors is whether this stability can translate into a tangible turnaround for its underperforming segments.

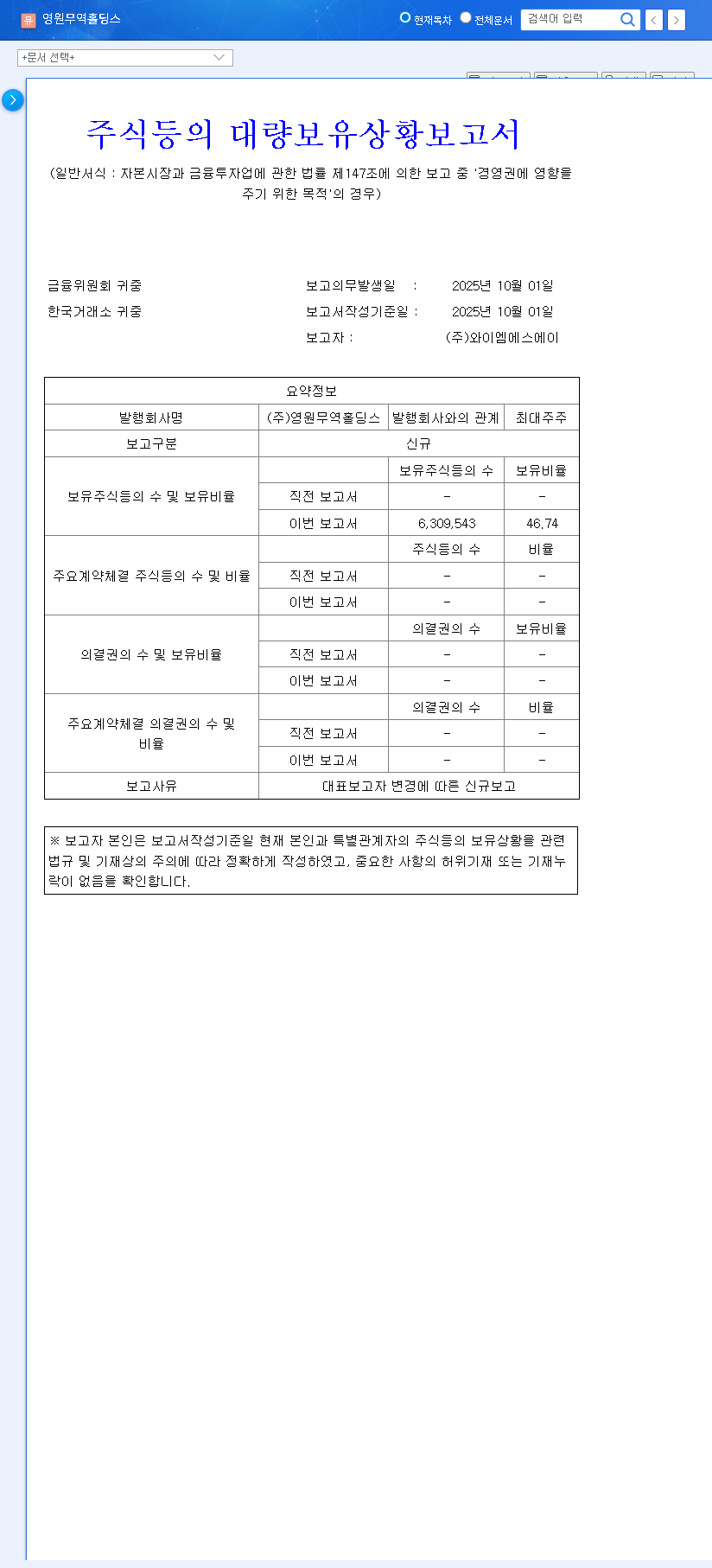

The Catalyst: Solidifying Management Control

On October 1, 2025, a significant corporate filing signaled a new era of governance for the company. The ‘Report on Large Shareholding Status’ officially confirmed that YMSA Co., Ltd., along with key related parties, now collectively holds a 46.74% stake with the clear intent to influence management. This was officially detailed in the company’s disclosure. (Official Disclosure: DART). This move effectively ends speculation about leadership uncertainty and consolidates power, creating a more stable foundation for long-term strategic planning and decisive action.

H1 2025 Performance: A Tale of Two Stories

To fully appreciate the context of the management stability event, a close examination of Youngone Trade Holdings’ H1 2025 performance is essential. The results paint a picture of top-line strength undermined by bottom-line pressures.

- •Impressive Revenue Growth: Consolidated revenue soared to KRW 2.1835 trillion, an 18.2% year-on-year increase. This was primarily fueled by the consistent performance of its core manufacturing OEM business and a partial recovery in other segments.

- •Profitability Under Pressure: Despite the revenue surge, operating profit fell by 5.4% to KRW 295 billion. This decline is almost entirely attributable to significant operational challenges in one specific area.

- •Stable Holding Company Operations: On a separate basis, the holding company itself performed well, with operating revenue up 20.6%, showcasing a solid dividend income base.

The SCOTT Business Unit: A Drag on Profitability

The primary source of the profitability decline was a staggering operating loss of KRW 54.5 billion from the SCOTT business unit. This division has been grappling with a growing inventory burden (up 8.3%) and rising accounts receivable, which continue to impact cash flow and overall performance. The market is now keenly focused on whether the newly consolidated management will implement a decisive turnaround strategy for the SCOTT business unit.

Impact Analysis of Management Stabilization

The shift towards strengthened control has multi-faceted implications for Youngone Trade Holdings. Investors should consider the potential effects across governance, finance, and market perception.

1. Governance and Operational Efficiency

With a near-majority stake, the leadership can now act with greater speed and conviction. This enhanced stability is expected to streamline decision-making for major investments, business restructuring, and strategic pivots. The firm resolve of the controlling shareholder reduces internal friction and aligns the company towards singular, long-term goals, such as enhancing overall shareholder value. For a deeper look at similar corporate governance shifts, see our analysis on industry leadership trends.

2. Financial and Strategic Outlook

While the event has no direct, immediate financial impact, it significantly increases the likelihood of bold future moves. This could include new M&A activities, a reshuffling of the business portfolio, or, most critically, an aggressive and well-funded strategy to fix the profitability issues within the SCOTT business unit. The market will be watching for signs of fresh capital allocation and new operational leadership in this segment.

3. Market Sentiment and Investor Confidence

Predictability is prized by the market. By reducing governance uncertainty, this event is likely to foster positive investor sentiment. As leading market analysts at Reuters often note, stability is a precursor to valuation growth. A clear plan to address the company’s challenges, driven by a newly empowered leadership, could act as a powerful catalyst for stock price appreciation, provided the strategy is credible and execution follows.

Investment Thesis & Actionable Insights

The investment analysis for Youngone Trade Holdings now hinges on execution. The foundation for a turnaround has been laid, but sustainable value creation depends on tangible performance improvements.

Key Monitorables for Investors:

- •SCOTT Turnaround Plan: Watch for announcements regarding new leadership, inventory management initiatives, and a clear path to profitability for this unit. Progress here is the single most important catalyst.

- •New Investment Synergies: Monitor how new strategic initiatives, like the YOH CVC Fund 2 investment, integrate with the core business and contribute to growth.

- •Macroeconomic Headwinds: Keep an eye on global economic conditions and currency fluctuations (e.g., KRW/USD exchange rate), as these external factors remain a significant risk.

In conclusion, while the management stabilization is a clear positive, prudent investors should remain focused on concrete business results. The potential for upside is significant if leadership can successfully translate its newfound control into operational excellence, particularly at the SCOTT division. Continuous monitoring of quarterly earnings and strategic announcements will be crucial.

Leave a Reply