The recent divestment by the National Pension Service (NPS) has sent shockwaves through the market, directly impacting the DL E&C share price and prompting investors to question their positions. When a financial titan like the NPS, South Korea’s largest institutional investor, significantly reduces its holdings in a major company, it’s more than just a transaction—it’s a powerful signal to the entire investment community. This move can influence market sentiment, trigger further selling, and raise critical questions about the company’s future prospects.

This comprehensive analysis goes beyond the headlines to dissect what the NPS’s stake reduction in DL E&C truly means for you. We will explore the reasons behind the sale, evaluate DL E&C’s current financial health, and provide a strategic playbook to help you navigate your DL E&C investment in this volatile environment.

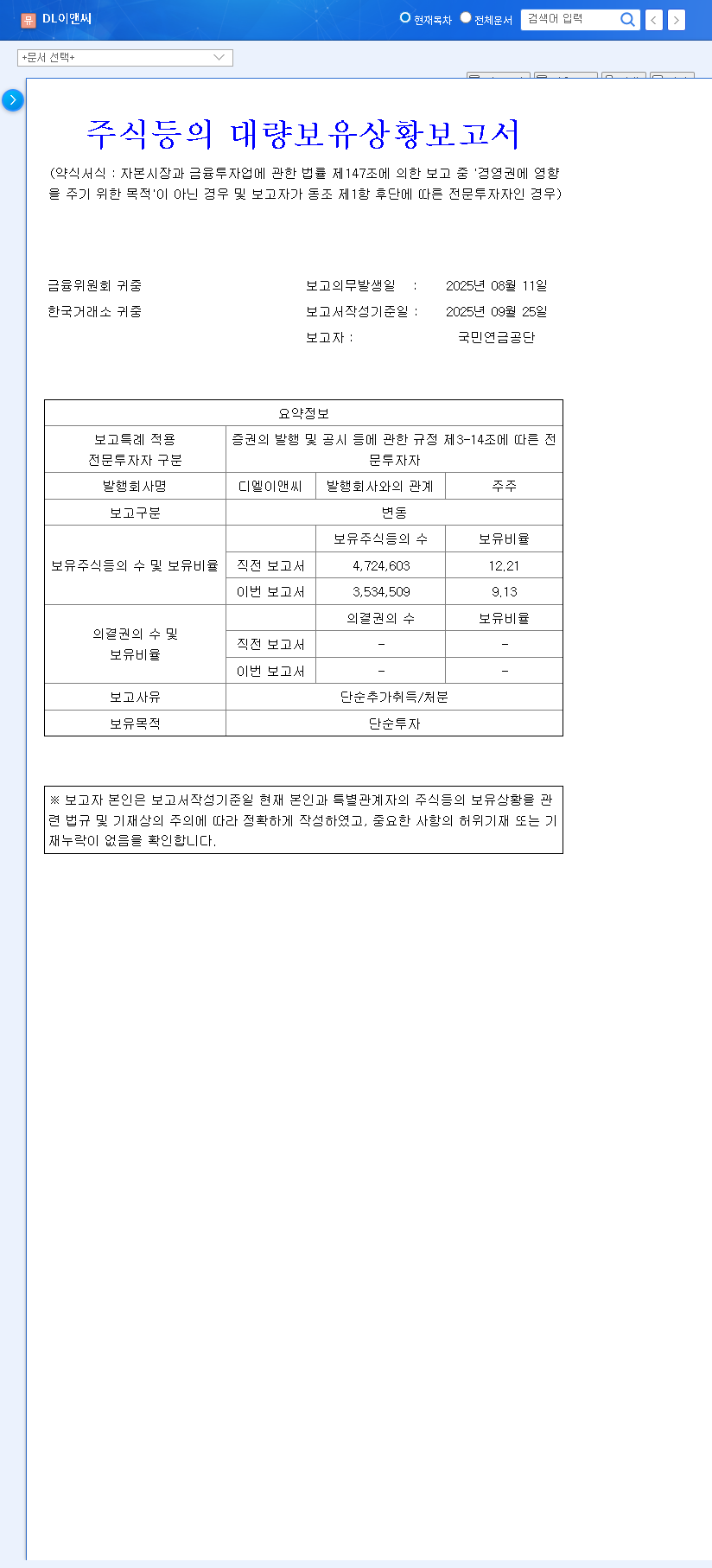

The Event: NPS Trims Its DL E&C Holdings

On October 1, 2025, the National Pension Service officially disclosed a significant reduction in its stake in DL E&C. This move, detailed in the ‘Report on the Status of Large Shareholdings,’ confirmed that the NPS’s position has been substantially downsized. While the stated purpose of the holding was ‘simple investment,’ such a large-scale disposal points towards a strategic re-evaluation of the DL E&C stock‘s attractiveness.

According to the Official Disclosure (DART), the NPS stake in DL E&C was reduced from 12.21% to 9.13%, representing a net decrease of approximately 3.08%. This is a substantial divestment that the market cannot ignore.

Decoding the NPS Divestment Strategy

Understanding why the NPS decided to sell is key to forecasting the future DL E&C share price. The decision was likely not based on a single factor but a combination of fundamental concerns, macroeconomic pressures, and portfolio management strategies.

A Closer Look at DL E&C’s Fundamentals (FY2024)

An examination of DL E&C’s 2024 financial performance reveals a mixed but concerning picture that may have influenced the NPS DL E&C investment committee:

- •Revenue Growth vs. Profit Squeeze: Revenue grew a respectable 4.10% to 8.32 trillion KRW. However, operating profit plummeted by 18.06% to 270.9 billion KRW, a significant red flag indicating margin compression.

- •Rising Liabilities: Total liabilities increased by 6.37%, but more concerning was the 22.44% jump in non-current liabilities, signaling an increase in long-term debt burdens.

- •Stable but Tenuous Equity: The debt-to-equity ratio remains stable at 100.4%, but the rapid rise in debt could challenge this stability if profitability does not recover.

- •Positive Net Profit: On a brighter note, net profit increased by 13.38%. This suggests effective non-operating financial management but doesn’t mask the core operational challenges.

The Shadow of Macroeconomic Headwinds

The construction sector is highly sensitive to the broader economic climate. Factors such as those reported by leading outlets like Bloomberg likely played a crucial role in the NPS’s decision. Persistently high interest rates increase borrowing costs for new projects, while inflation drives up the price of raw materials like steel and concrete. Combined with a volatile real estate market, these factors create a challenging operational environment and dampen the outlook for profitability, thus affecting the perceived value of DL E&C stock.

Impact on DL E&C Share Price and Investor Sentiment

The immediate impact of the NPS sale is likely to be negative for the DL E&C share price. The sudden increase in the supply of shares can create short-term downward pressure. More importantly, it acts as a negative signal, eroding investor confidence. Other institutional and retail investors may follow the NPS’s lead, fearing that the pension giant has insights they lack. This can create a domino effect of selling, further depressing the stock price regardless of the company’s underlying fundamentals.

Investor Playbook: How to Approach Your DL E&C Investment

This event calls for a cautious and strategic approach. Instead of a panic sale, investors should conduct a thorough re-evaluation. For more context on the sector, consider reading our Guide to Investing in the South Korean Construction Sector. Here are key factors to monitor:

- •Institutional Flow: Keep a close eye on the trading patterns of other major institutional investors. Is this an isolated move by the NPS, or the beginning of a broader institutional exit?

- •Profitability Strategy: Look for clear communication from DL E&C’s management on how they plan to tackle rising costs and improve their core operating profit margins.

- •Order Book Health: A strong and growing pipeline of new orders is the lifeblood of any construction company. Assess the quality and profitability of new contracts being secured.

- •Growth in New Ventures: Evaluate the progress of DL E&C’s investments in future-facing sectors like renewable energy and carbon capture. Success in these areas could offset cyclical downturns in traditional construction.

In conclusion, the National Pension Service DL E&C stake sale is a significant development that warrants careful consideration. While it casts a shadow over the stock in the short term, it also presents an opportunity for diligent investors to assess whether the market’s reaction has created a buying opportunity or validated underlying weaknesses. All investment decisions should be made with careful judgment and personal responsibility.

Leave a Reply