Investors in PSK stock (319660) are on high alert after a significant portfolio adjustment by one of South Korea’s largest institutional investors. The National Pension Service (NPS) recently announced a reduction in its holdings of the semiconductor equipment specialist, sending ripples through the market. This move prompts critical questions: Is this a routine portfolio rebalancing, or does it signal underlying concerns about the company’s future? This analysis will dissect the NPS stake reduction, examine PSK’s current fundamentals, and provide a clear outlook for investors.

The Disclosure: NPS Reduces PSK Stake

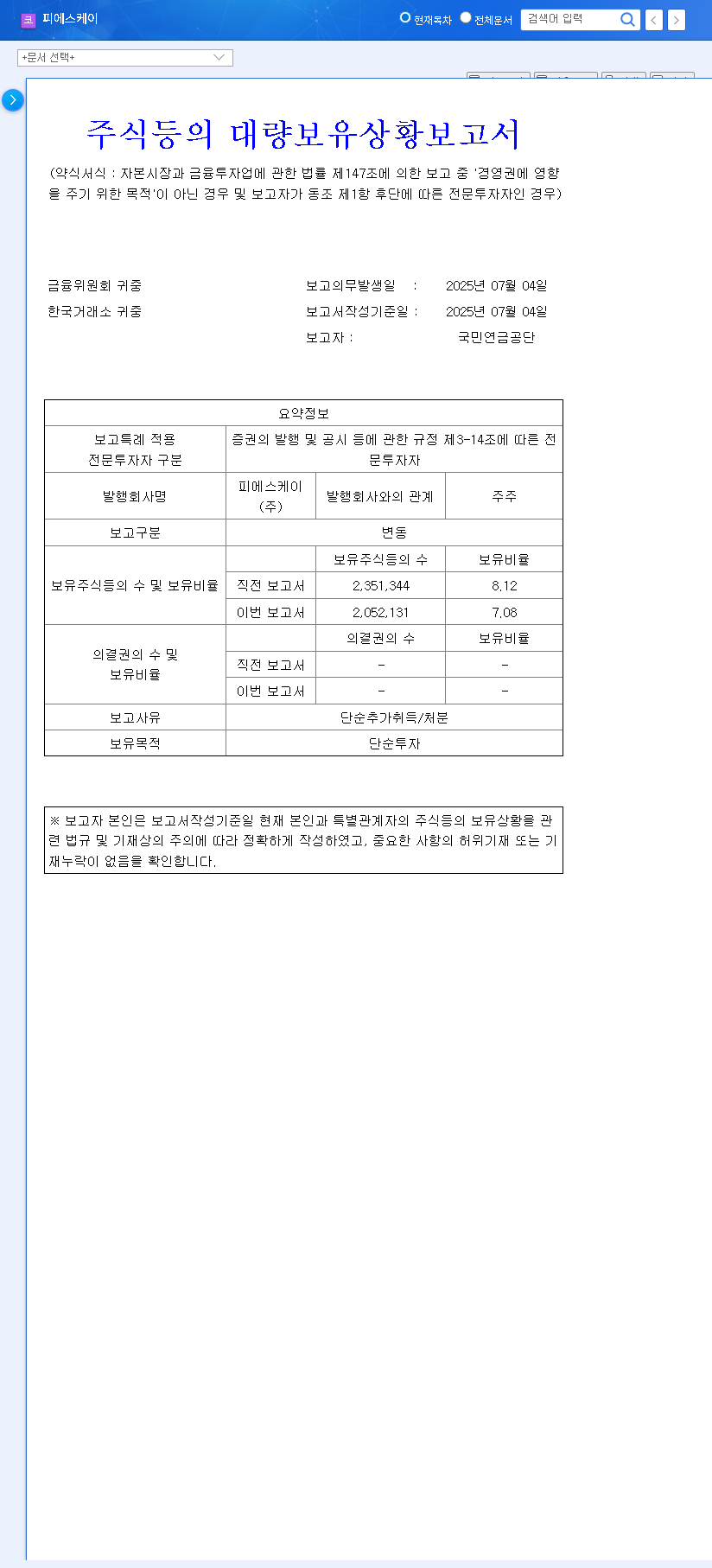

On October 1, 2025, an official disclosure revealed that the National Pension Service had decreased its ownership in PSK from 8.12% to 7.08%, a net reduction of 1.04%. According to the filing, the reason cited was a “simple investment purpose, resulting from additional acquisitions/disposals.” You can view the filing directly from the source: Official Disclosure. While the stated reason appears neutral, any reduction in holdings by a major entity like the NPS is scrutinized by the market and can act as a catalyst for selling pressure and heightened volatility for PSK stock.

Analyzing the ‘Why’: PSK’s Fundamentals and Market Headwinds

To understand the potential rationale behind the NPS stake reduction, we must look beyond the disclosure and evaluate PSK’s internal health and the external environment it operates in.

1. A Look at Corporate Fundamentals

PSK’s recent financial performance presents a mixed picture. The 2025 half-year report indicated a significant downturn, with revenue dropping by 47% and operating profit by 48.5% year-over-year. This slump was primarily attributed to weaker sales in non-semiconductor process equipment and rising administrative costs. However, the company’s financial foundation remains solid. Its debt-to-equity ratio is a healthy 19.93%, and a notable increase in operating cash flow suggests efficient core operations. Furthermore, PSK continues to invest heavily in its future, with R&D expenditures accounting for 8.2% of revenue—a crucial factor for staying competitive in the fast-evolving semiconductor equipment industry.

While the top-line numbers are concerning, PSK’s strong balance sheet and commitment to R&D provide a buffer and a potential springboard for future growth once the industry cycle turns positive.

2. Macroeconomic and Industry Context

No company operates in a vacuum. Rising interest rates in the U.S. and Korea increase the cost of capital, potentially dampening corporate investment and investor sentiment. Simultaneously, exchange rate volatility poses both a risk and an opportunity. For PSK, with more USD-denominated assets than liabilities, a stronger dollar can boost profits. However, this factor is a double-edged sword that requires careful risk management. On a brighter note, the long-term outlook for the semiconductor industry remains robust. According to industry analysis from authoritative sources like Gartner, the demand for advanced chips continues to grow, which will inevitably drive investment in sophisticated semiconductor equipment.

3. Known Risk Factors

Investors must also weigh an ongoing patent infringement lawsuit with competitor Lam Research. An unfavorable outcome could have a material impact on PSK’s financial statements and market position. This existing legal risk, combined with the news of the NPS sale, could compound investor caution and create headwinds for the PSK stock price.

Investor Action Plan: Navigating the Uncertainty

In light of the NPS’s move and the company’s current state, a measured approach is crucial. The short-term outlook for PSK stock is likely to be choppy, with downward pressure from the stake sale. However, the mid-to-long-term trajectory will depend on fundamental improvements and industry tailwinds. Here are key areas for investors to monitor:

- •Quarterly Performance: Watch for a recovery in revenue and operating profit. A clear sign of a turnaround, tied to the broader semiconductor cycle, will be the most powerful bullish catalyst.

- •Patent Litigation Updates: Stay informed on any developments in the Lam Research lawsuit. A settlement or favorable ruling could remove a significant overhang from the stock.

- •Institutional Investor Flow: Monitor whether other major institutions follow the NPS’s lead or if they use the price dip as a buying opportunity. This will provide clues about broader market sentiment.

- •Industry Investment Trends: Track capital expenditure plans from major chipmakers like TSMC, Samsung, and Intel. Increased spending by these giants is a direct leading indicator for equipment suppliers like PSK. For more on this, see our guide on how to analyze semiconductor stocks.

Conclusion: Signal or Noise?

The National Pension Service‘s stake reduction is a significant event that introduces short-term risk and uncertainty for PSK stock. However, it may ultimately be more noise than a definitive signal about the company’s long-term demise. PSK’s solid financial health, technological edge, and the structural growth of the semiconductor industry remain compelling long-term positives. Prudent investors should proceed with caution, weigh the risks against the potential rewards, and base their decisions on the fundamental developments in the coming quarters.

Leave a Reply