The outlook for Daehan Shipbuilding stock has received a significant boost following a major contract announcement that has captured investor attention. The company recently disclosed a substantial order for a crude oil tanker, a move that signals robust operational health and promising future revenue streams. This development is more than just a line item on an order book; it’s a critical indicator of the company’s competitive position and its potential for sustained growth in a dynamic global market.

This comprehensive analysis will dissect the specifics of this new contract, evaluate its direct impact on Daehan Shipbuilding’s financials, and explore the broader industry trends that create both opportunities and challenges. For anyone considering an investment in Daehan Shipbuilding, understanding these interconnected factors is essential for making an informed decision.

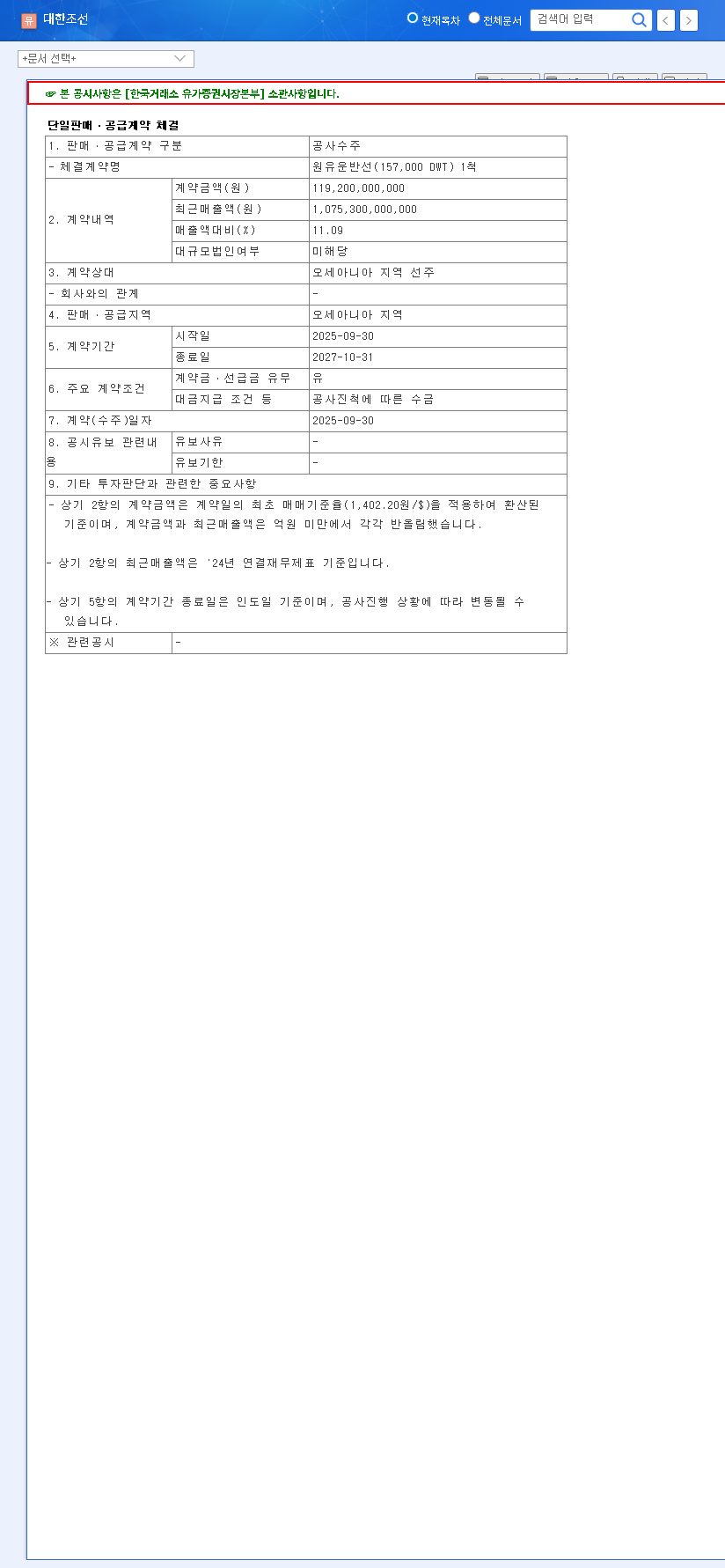

The Landmark KRW 119.2 Billion Crude Oil Tanker Order

On October 1, 2025, Daehan Shipbuilding officially announced a landmark single sales and supply contract with a prominent Oceania-based shipowner. The official filing provides transparent details of this pivotal agreement (Source: Official DART Report).

This contract for a 157,000 DWT crude oil tanker not only represents 11.09% of the company’s 2025 first-half revenue but also secures a stable production pipeline until late 2027, significantly enhancing revenue visibility.

Key Contract Details

- •Contract Value: KRW 119.2 billion.

- •Vessel Type: One 157,000 DWT (Suezmax) crude oil tanker, a core product for the company.

- •Contract Partner: An established shipowner based in the Oceania region.

- •Project Timeline: September 30, 2025, to October 31, 2027.

Why This Order Matters for Daehan Shipbuilding Stock

This order arrives at a time when Daehan Shipbuilding is demonstrating remarkable fundamental strength, further amplified by a favorable shipbuilding industry outlook. The synergy between internal health and external market conditions presents a compelling case for investors.

Strengthened Fundamentals: A Growth Story

The first half of 2025 was transformative for Daehan Shipbuilding. The company posted a staggering 129% year-over-year increase in operating profit, achieving an impressive 21.9% margin. This isn’t just a cyclical upswing; it’s the result of strategic financial management, including a successful KOSPI market listing in August 2025 that bolstered its capital base. With a manageable debt-to-equity ratio of 117.5%, the company is well-positioned to fund future growth and innovation, such as developing eco-friendly vessels powered by LNG, ammonia, and methanol.

Favorable Market & Macroeconomic Tailwinds

The global push for decarbonization is a powerful catalyst. Stricter IMO environmental regulations are accelerating the replacement cycle for older, less efficient vessels, creating sustained demand for modern ships. According to leading maritime analysts, this trend is expected to continue for the next decade. Furthermore, as an export-driven company, Daehan Shipbuilding benefits from a strong USD/KRW exchange rate, which enhances the value of its international contracts when converted to local currency. Lowering benchmark interest rates in the U.S. also helps reduce financing costs for new projects.

Investment Analysis: Potential vs. Risks

This crude oil tanker order is a clear positive catalyst. It ensures predictable revenue, improves cash flow, and solidifies the company’s reputation as a leader in the mid-size tanker market. However, a comprehensive investment analysis requires a balanced view of the potential risks.

Positive Investment Factors

- •Visible Earnings Growth: The new order provides a clear roadmap for revenue and profitability into 2027.

- •Solid Financial Footing: Strong H1 2025 performance and a healthy balance sheet provide a stable foundation.

- •Market Leadership: The order reinforces the company’s expertise in its core Suezmax and Aframax tanker segments.

- •Favorable Macro Environment: Strong exchange rates and demand for eco-friendly ships act as powerful tailwinds. For more context, see our complete guide to investing in the shipbuilding sector.

Key Risks to Monitor

- •Global Economic Volatility: A significant economic slowdown could dampen shipping demand and new order flows.

- •Cost Fluctuations: The price of steel and other raw materials, along with currency shifts, can impact profitability on long-term contracts.

- •Intense Competition: The shipbuilding industry is highly competitive, with pressure from other major players in Korea and abroad.

Conclusion: The KRW 119.2 billion order is a powerful validation of Daehan Shipbuilding’s strategy and capabilities. It provides a solid underpinning for the company’s stock value by enhancing earnings visibility and confirming its market leadership. While investors must remain vigilant of macroeconomic risks, the combination of strong fundamentals and favorable industry trends positions Daehan Shipbuilding stock as a compelling name to watch in the industrial sector.

Leave a Reply