The recent announcement of the Withtec contract with Samsung Electronics has sent ripples through the market. Valued at a staggering ₩12.4 billion, this deal represents a monumental win for Withtec (KOSDAQ). However, this victory arrives amidst pressing concerns about the company’s declining profitability. For investors, this creates a critical question: is this contract a genuine turning point towards sustainable growth, or a temporary boost that masks deeper financial issues? This comprehensive Withtec stock analysis will delve into the contract details, the company’s financial health, and provide a strategic outlook for potential investors.

Unpacking the Landmark Samsung Electronics Contract

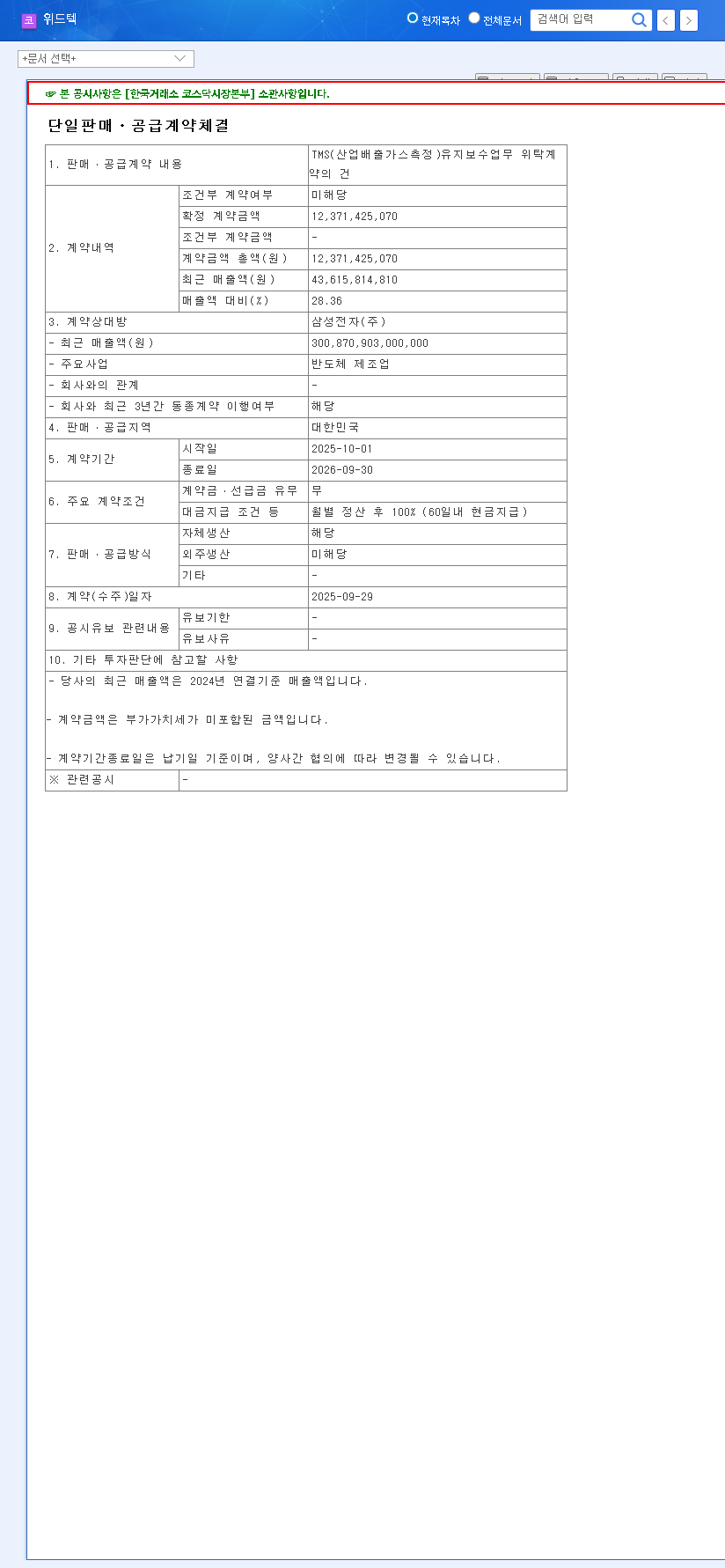

On September 30, 2025, Withtec officially disclosed the signing of a ₩12.4 billion agreement with Samsung Electronics. This is not a small feat; the figure accounts for a massive 28.36% of Withtec’s recent annual revenue. The contract is for TMS (Total Measurement System for Industrial Emission Gas) maintenance services and will run for one year, from October 1, 2025, to September 30, 2026. TMS systems are vital for large-scale manufacturers like Samsung to monitor and control gas emissions, ensuring environmental compliance and operational efficiency. Securing such a critical maintenance contract with a global leader provides a significant and stable revenue stream. This information is based on the company’s public filing. (Official Disclosure: DART).

While the revenue injection is substantial, the core challenge for Withtec remains translating top-line growth into bottom-line profit. The company’s underlying cost structure and operational efficiency are now under the microscope.

Withtec’s Financial Health: A Tale of Two Tapes

To understand the true impact of the Samsung deal, we must analyze Withtec’s financial state leading up to it. The first half of 2025 painted a mixed picture, highlighting both growth and significant operational strain.

Revenue Growth vs. Worsening Profitability

Withtec’s H1 2025 sales reached ₩19.22 billion, a respectable 16% year-over-year increase. However, this growth was overshadowed by an operating loss of ₩590 million—a staggering 219% drop in operating profit. This signals a severe Withtec profitability problem, driven by rising costs that outpaced revenue growth.

Key Financial Strengths and Weaknesses

- •Positive Signal: The sales share of higher-margin in-house products grew to 32.6%, and an improved debt-to-equity ratio suggests better long-term financial stability.

- •Red Flag: Soaring cost of sales, increased R&D spending, and higher financial costs crushed margins.

- •Red Flag: Declining liquidity ratios and negative operating cash flow raise concerns about Withtec’s ability to meet short-term obligations without external financing. To learn more, see this guide on corporate liquidity from a leading financial authority.

Investment Strategy & Future Outlook

The Withtec contract with Samsung Electronics is a major catalyst, but a prudent investment approach is required. The key is whether this revenue can be converted into sustainable profit while the company navigates macroeconomic challenges and nurtures new ventures like its nuclear decommissioning analysis business.

For Short-Term Traders

The contract news provides positive short-term momentum. However, traders should be cautious. The stock price (PBR of 0.75x) is in undervalued territory, but without confirmed profitability improvements, the rally could be short-lived. Monitor trading volumes and be wary of profit-taking near previous resistance levels.

For Long-Term Investors

Long-term success hinges on fundamental improvements. Investors should focus on the following in upcoming quarterly reports:

- •Contract Margin Analysis: Scrutinize the cost structure associated with the TMS maintenance contract to see if it genuinely improves overall company margins.

- •Operational Efficiency: Look for evidence of cost control in Selling, General & Administrative (SG&A) expenses.

- •New Business Progress: Monitor for updates on the nuclear decommissioning venture, as this represents a key long-term growth driver. For more details, review our guide to analyzing small-cap growth stocks.

Frequently Asked Questions (FAQ)

Q1: What is the size and scope of the Withtec-Samsung contract?

A1: Withtec secured a ₩12.4 billion contract for TMS (Total Measurement System) maintenance with Samsung Electronics, running for one year. It represents 28.36% of Withtec’s recent revenue.

Q2: How does this contract affect Withtec’s business?

A2: It provides a significant and stable revenue stream, enhancing business stability. The partnership with a prestigious client like Samsung also boosts Withtec’s credibility in the market, potentially opening doors for future contracts.

Q3: What is the main concern in this Withtec stock analysis?

A3: The primary concern is Withtec’s profitability. Despite revenue growth in H1 2025, the company posted an operating loss due to rising costs. The key question is whether this new contract carries a high enough margin to reverse this negative trend.

Leave a Reply