The pharmaceutical landscape is buzzing with anticipation as Hanmi Science, a major player in the biotech industry, announced that its promising new diabetes drug, HM11260C, has received approval to enter a pivotal Phase 3 trial. This milestone represents a significant step forward not only for the company but also for millions of patients with Type 2 diabetes seeking more effective treatment options. For investors, this development signals a critical inflection point, warranting a closer look at the potential rewards and inherent risks.

This article provides a detailed analysis of the HM11260C Phase 3 trial, its implications for Hanmi Science’s market valuation, the competitive landscape of Type 2 diabetes treatments, and a strategic investment thesis for those monitoring the biotech sector.

The Landmark Announcement: HM11260C’s Path to Phase 3

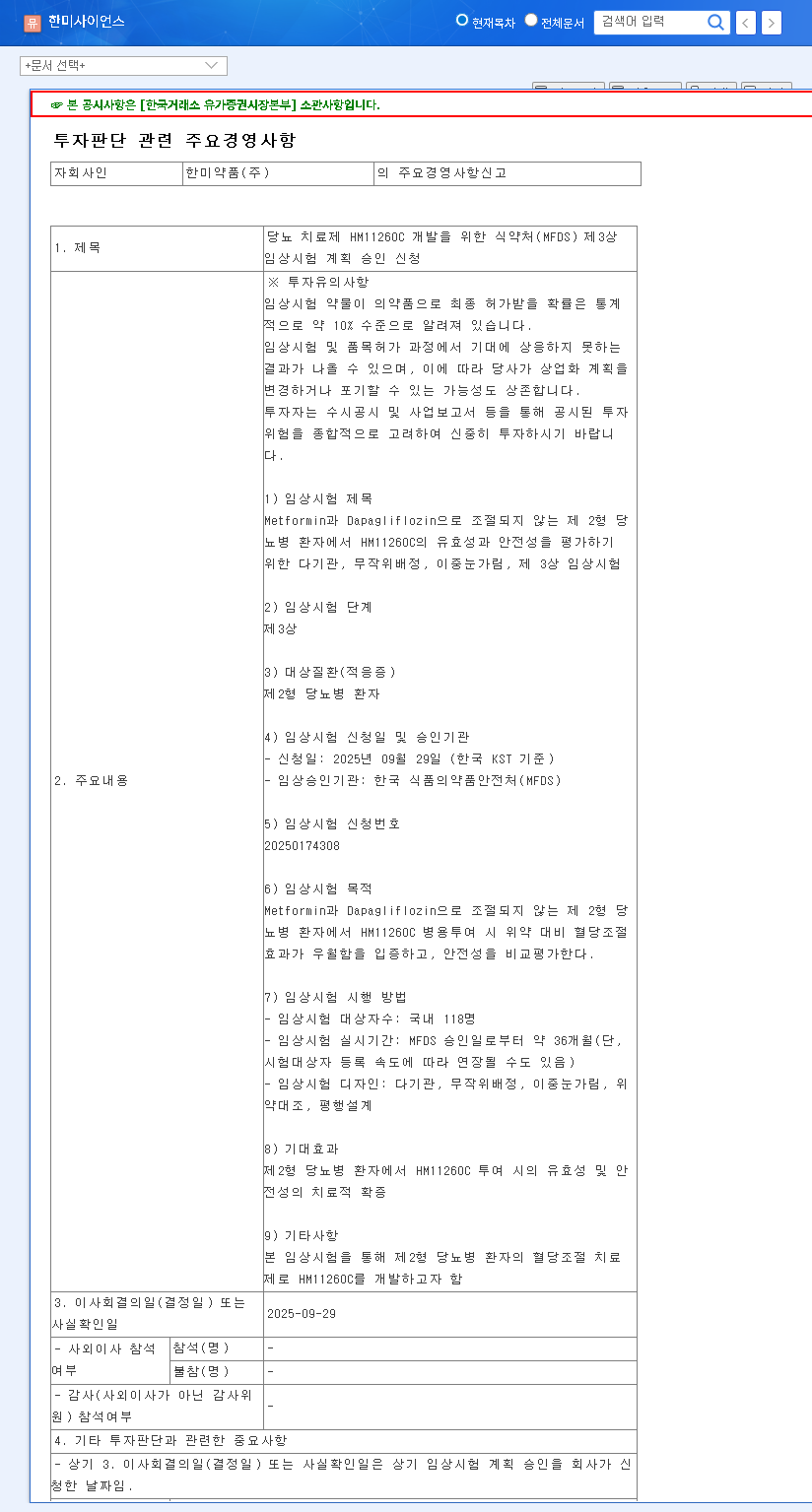

On September 30, 2025, Hanmi Pharm, a key subsidiary of Hanmi Science, submitted its application to the Ministry of Food and Drug Safety (MFDS) for the Phase 3 clinical trial of HM11260C. The company’s official disclosure, available via the DART system, confirms the initiation of this crucial late-stage study. You can view the full details in the Official Disclosure. This multicenter, randomized, double-blind trial is designed to rigorously evaluate the efficacy and safety of the drug in patients with Type 2 diabetes whose condition is not adequately managed by existing metformin and dapagliflozin therapies.

Key Details of the Clinical Trial:

- •Target Indication: Type 2 Diabetes Mellitus

- •Clinical Phase: Phase 3

- •Primary Objective: To demonstrate superior glycemic control of HM11260C compared to a placebo, while thoroughly assessing its safety profile.

Market Impact and Corporate Value Proposition

For any pharmaceutical company, advancing a novel drug candidate to a Phase 3 trial is a massive catalyst. It validates years of R&D and brings the product one critical step closer to commercialization. The global market for Type 2 diabetes treatments is enormous and continues to grow, driven by lifestyle changes and an aging population. According to the World Health Organization (WHO), diabetes is a major global health issue, creating a persistent demand for innovative and more effective therapies. A successful outcome for HM11260C could unlock billions in potential revenue for Hanmi Science.

Fundamental Strengths of Hanmi Science (H1 2025)

Beyond the pipeline, Hanmi Science’s fundamentals provide a degree of stability. In the first half of 2025, the company posted an operating profit margin of 9.2%. While its pharmaceutical wholesale segment faced headwinds, robust performance in its holding and healthcare divisions provided a crucial offset. This diversification can help cushion the financial burden of a long and expensive Phase 3 trial, which can often take over 36 months to complete. A stable financial structure, with a debt-to-equity ratio of 58.9%, further strengthens its position to fund ongoing R&D initiatives.

A Balanced View: Potential Upsides vs. Inherent Risks

While the initiation of the HM11260C Phase 3 trial is overwhelmingly positive, prudent investors must weigh the potential against significant risks. Drug development is a high-stakes endeavor, and the final hurdle is often the most difficult to clear.

Positive Factors for Investors

- •Enhanced Pipeline Visibility: This trial significantly de-risks the asset and validates Hanmi’s R&D capabilities, attracting market attention.

- •Future Growth Engine: If successful, HM11260C could become a blockbuster drug, securing a long-term revenue stream for the company.

- •Diversified Business Model: The stability of other business segments provides a financial cushion to absorb R&D costs.

Risks and Considerations

- •Clinical Trial Uncertainty: Historically, the success rate for Phase 3 trials is far from guaranteed. Statistically, only about 58% of drugs that enter Phase 3 ultimately gain approval. Failure to meet primary endpoints would be a major setback.

- •Financial Commitment: These trials are incredibly expensive and lengthy, representing a continuous drain on capital resources until the drug is commercialized.

- •Macroeconomic Headwinds: Factors like interest rates, currency fluctuations, and market sentiment can impact funding and overall business operations.

Investor Action Plan and Strategic Outlook

Investing in a biotech company on the cusp of a Phase 3 readout requires a strategy that balances optimism with caution. The journey for HM11260C is far from over. Investors should adopt a long-term perspective, as significant value inflection will likely coincide with clinical data announcements.

A prudent approach involves closely monitoring trial progress and any interim data releases. Furthermore, understanding the company’s broader financial health is essential. For those looking to manage risk, a strategy of dollar-cost averaging or building a position in stages aligned with key milestones could be effective. It is also wise to diversify investments, as explored in our complete guide to biotech investing, to avoid overexposure to a binary clinical outcome.

In conclusion, Hanmi Science’s progress with its diabetes drug HM11260C is a compelling development. While the potential upside is substantial, the path to approval is fraught with challenges. A cautious but optimistic stance, backed by thorough due diligence, is the recommended course of action.

Leave a Reply