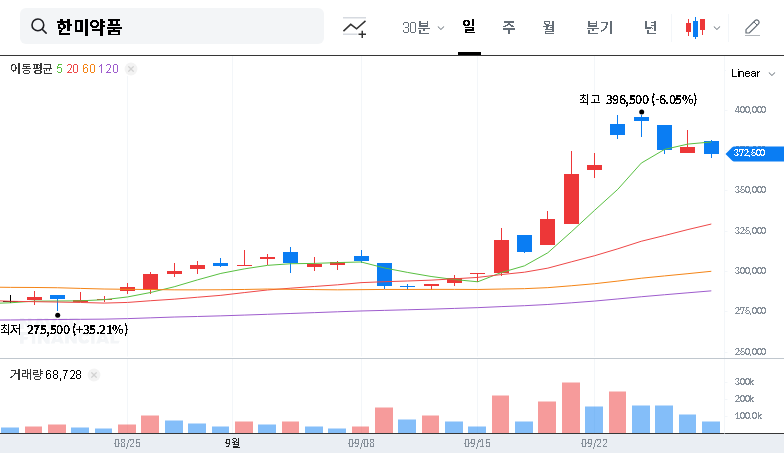

The pharmaceutical sector is buzzing with a significant development from Hanmi Pharmaceutical (128940). This in-depth analysis focuses on Hanmi Pharmaceutical HM11260C, a promising new drug for Type 2 Diabetes, which has officially entered the pivotal Phase 3 clinical trial stage. This move, confirmed by an application to the Ministry of Food and Drug Safety (MFDS), represents a critical milestone that could reshape the company’s future and presents a complex scenario for investors. For those following Hanmi Pharmaceutical stock, understanding the nuances of this HM11260C clinical trial is paramount.

This comprehensive guide will break down the implications of the Phase 3 trial, evaluate the market potential for this new Type 2 Diabetes treatment, and weigh the substantial opportunities against the inherent risks. We will provide expert-level insights to help you navigate this high-stakes development.

Phase 3 is the final and most expensive stage of drug development. Its success or failure will have a direct and significant impact on Hanmi Pharmaceutical’s valuation and strategic direction.

The Significance of the HM11260C Phase 3 Trial

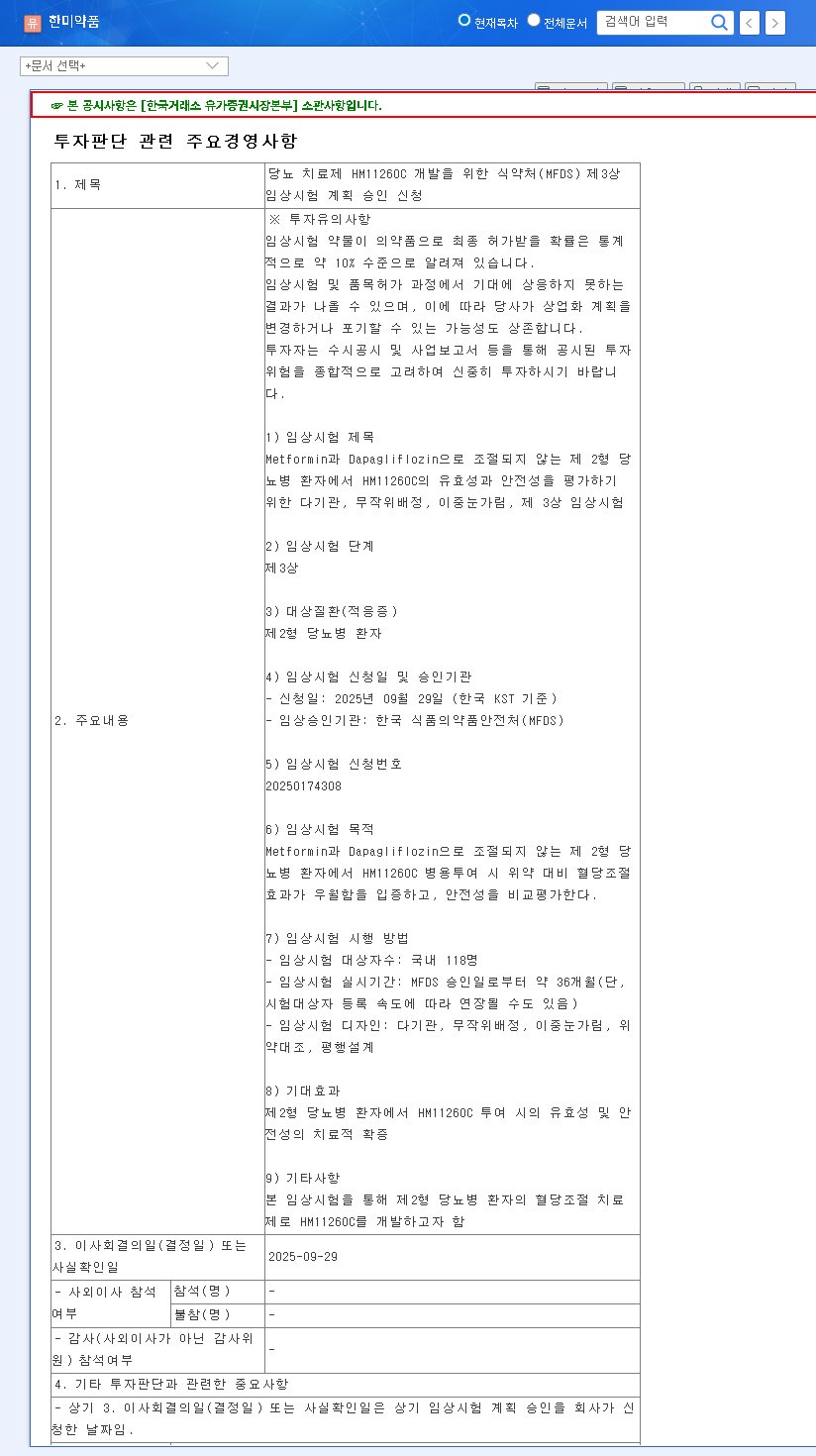

On September 30, 2025, Hanmi Pharmaceutical submitted its application for a multi-center, randomized, double-blind Phase 3 clinical trial. The study is designed to rigorously evaluate the efficacy and safety of Hanmi Pharmaceutical HM11260C in a specific patient population: individuals with Type 2 Diabetes whose blood sugar remains poorly controlled despite treatment with both Metformin and Dapagliflozin. This is a crucial step beyond earlier trials, moving from controlled testing to a larger, more diverse patient group to confirm its real-world effectiveness and safety profile needed for market approval.

Successfully completing a diabetes drug Phase 3 trial dramatically increases the probability of commercialization. This final hurdle is where many promising compounds fail, making Hanmi’s progress a closely watched event in the industry. For transparency and official details, investors should review the Official Disclosure (DART) filed by the company.

Market Potential & Competitive Landscape

Tapping into a Multi-Billion Dollar Market

The global market for Type 2 Diabetes treatment is enormous and continues to grow due to rising prevalence worldwide. According to market research from firms like Grand View Research, this market is valued in the tens of billions of dollars annually. There is a significant unmet need for more effective, safer, and convenient therapies, especially for patients who do not respond adequately to existing first- and second-line treatments. If Hanmi Pharmaceutical HM11260C can demonstrate superior glycemic control, a better safety profile (e.g., lower risk of hypoglycemia), or other benefits like weight loss or cardiovascular protection, it could capture a substantial share of this lucrative market.

The Competitive Arena

The diabetes market is highly competitive, dominated by major pharmaceutical players with blockbuster drugs like GLP-1 receptor agonists (e.g., Ozempic, Trulicity) and SGLT2 inhibitors (e.g., Jardiance, Farxiga). For HM11260C to succeed, it must carve out a unique position. Its target patient population—those uncontrolled on Metformin and Dapagliflozin (an SGLT2 inhibitor)—suggests it could be positioned as a powerful third-line add-on therapy. Its success will depend on clinical data that proves it’s not just another option, but a superior one.

Investor Analysis: Balancing Opportunity and Risk

For investors evaluating Hanmi Pharmaceutical stock, this development is a classic high-risk, high-reward scenario. A clear-eyed assessment of both the upside and downside is essential. To learn more about this type of analysis, you can read our guide on how to evaluate biotech stocks.

The Bull Case (Potential Upside)

- •Pipeline Validation: A successful trial validates Hanmi’s R&D capabilities, potentially boosting investor confidence across their entire drug pipeline.

- •Blockbuster Potential: A differentiated and effective new diabetes drug has the potential to achieve blockbuster status (over $1 billion in annual sales), which would fundamentally increase corporate value.

- •Market Leadership: Success could establish Hanmi as a key player in the global diabetes treatment market, creating a long-term revenue stream.

The Bear Case (Key Risks to Monitor)

- •High Failure Rate: Historically, drugs entering Phase 3 trials still face a significant risk of failure (around 40-50%). A negative outcome could lead to a sharp decline in stock price.

- •Financial Drain: Phase 3 trials are incredibly expensive, consuming hundreds of millions of dollars. Investors must monitor Hanmi’s cash flow and R&D expenditures to ensure the company can sustain the cost without compromising its financial stability.

- •Sub-par Data: Even if the trial succeeds, the drug may only show modest benefits. If the data isn’t compelling enough to convince doctors and payers, market adoption could be slow, limiting its commercial success.

Conclusion: Cautious Optimism is Warranted

The initiation of the Hanmi Pharmaceutical HM11260C Phase 3 trial is undeniably a positive catalyst, signaling strong potential for long-term growth. The event may generate short-term positive sentiment for the stock. However, long-term value will be dictated entirely by the clinical data. Investors should adopt a strategy of ‘cautious optimism,’ recognizing the immense potential while remaining keenly aware of the binary risks involved. Continuous monitoring of clinical trial updates, competitor moves, and the company’s financial health will be the key to making an informed investment decision.

Leave a Reply