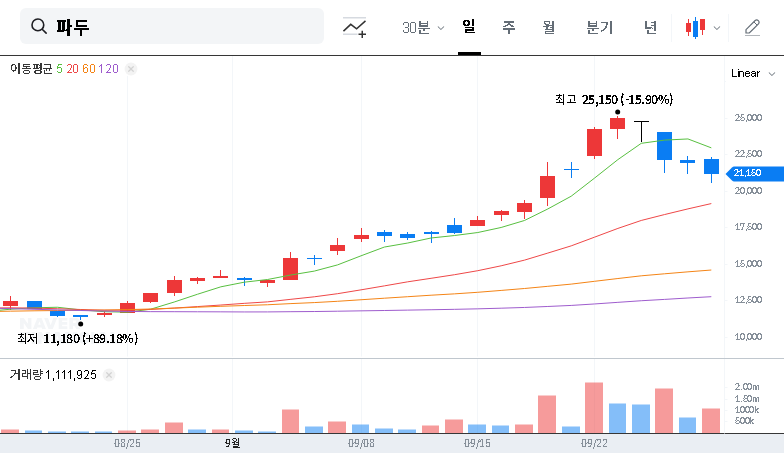

The recent trajectory of FADU stock has become a significant concern for investors, triggered by a substantial stock sale from a major shareholder. In late September 2025, RFC Forward, a key stakeholder, divested a large portion of its shares, compounding the already severe profitability crisis plaguing the company. This move has created a perfect storm of negative sentiment, leaving many to question the company’s future viability and long-term corporate value.

This comprehensive FADU stock analysis delves into the core reasons behind RFC Forward’s sell-off, examines the company’s precarious financial health, and provides a strategic roadmap for both current and potential investors navigating this turbulent period.

A major shareholder’s exit, especially when coupled with fundamental weakness, is a critical red flag. It signals a loss of confidence from those with deep insight into the company’s operations, demanding immediate and careful scrutiny from the market.

The Catalyst: RFC Forward’s Shareholding Change

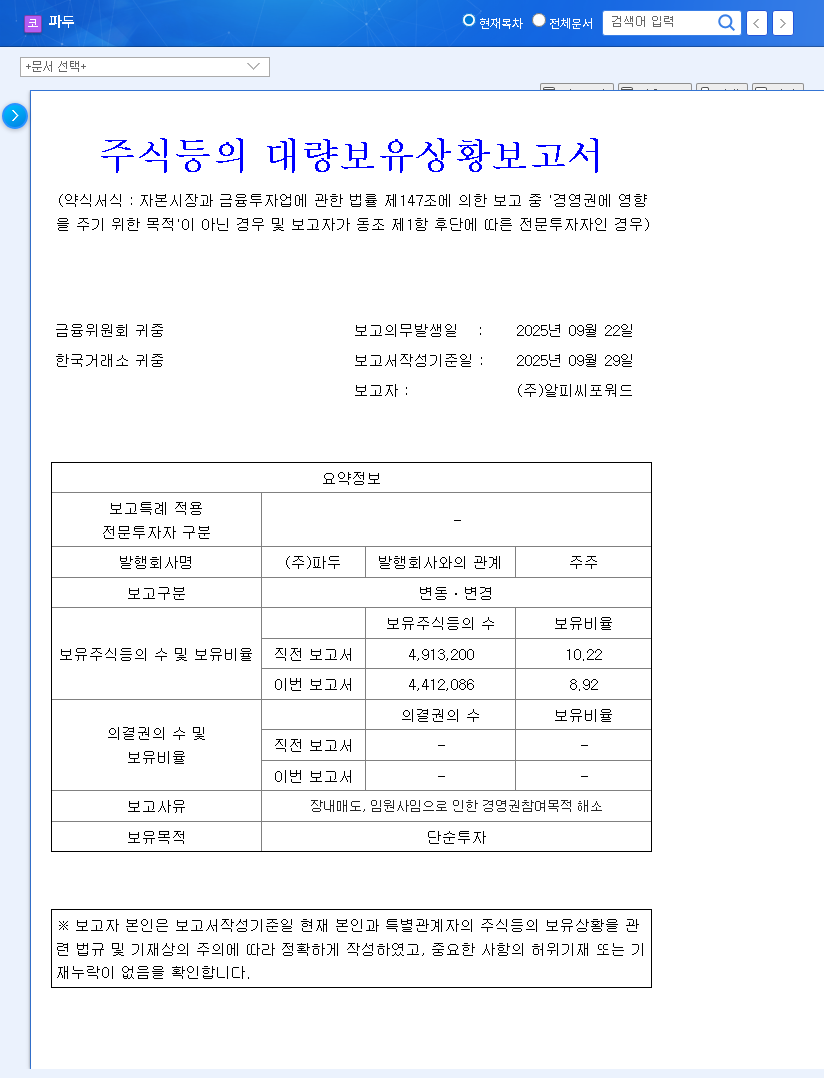

On September 29, 2025, the market was jolted by a disclosure from RFC Forward outlining a significant change in its FADU holdings. The official filing revealed critical details about this move, which has since amplified concerns among FADU investors.

- •Stake Reduction: RFC Forward’s ownership stake was reduced from 10.22% to 8.92%, a notable 1.3 percentage point drop.

- •Stated Rationale: The sale was attributed to open market transactions and, more importantly, the ‘termination of management participation objectives’ following an executive’s resignation. This signals a strategic retreat from active involvement.

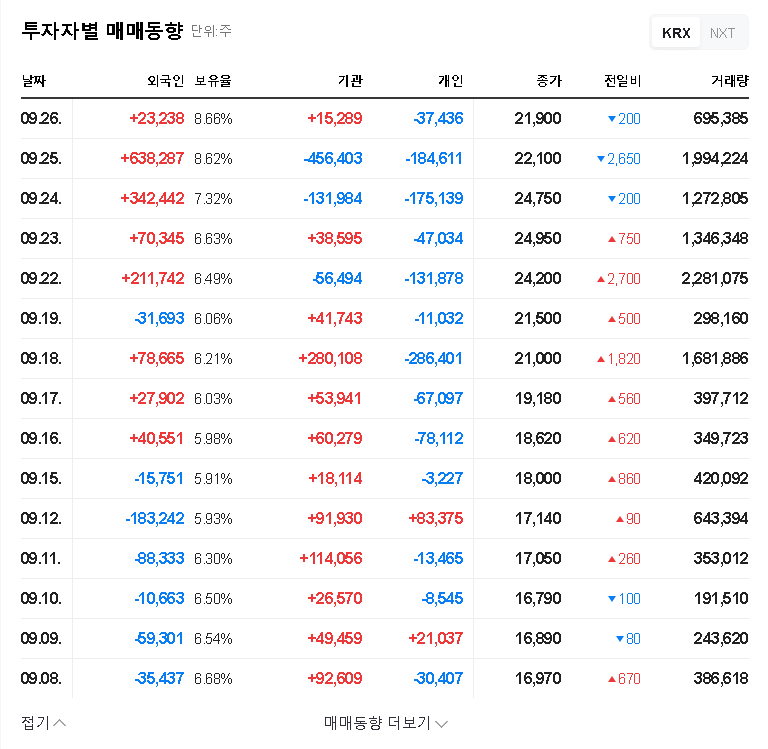

- •Concentrated Selling Period: The bulk of the shares were sold between September 22 and September 25, 2025, exerting intense, direct pressure on the stock price during that window.

- •Official Disclosure: The complete details of this transaction are documented in the official regulatory filing. Source: DART Report.

FADU’s Fundamental Crisis: A Deeper Look

RFC Forward’s sell-off did not happen in a vacuum. It occurred against a backdrop of deeply troubling financial performance and instability, which magnifies the sale’s negative impact.

Severe Profitability Deterioration

The company’s financial statements paint a grim picture of its operational health. Revenue plummeted from KRW 56.4 billion in 2022 to just KRW 22.5 billion in 2023. Worse, FADU swung from a modest operating profit of KRW 1.5 billion to a staggering operating loss of KRW -58.6 billion in 2023. Projections for 2024 suggest this loss could deepen to KRW -95.0 billion, indicating that the core business is bleeding cash at an alarming rate. This highlights a critical failure in the company’s FADU profitability model.

Plummeting Shareholder Value and High Valuation

Return on Equity (ROE), a key measure of shareholder return, collapsed from a high of 380.21% in 2022 to -50.20% in 2023, with a further decline to -64.47% expected. This means the company is actively destroying shareholder value. Despite this, the stock maintains a high Price-to-Book Ratio (PBR) projected at 7.69x for 2024. A high PBR can sometimes be justified for high-growth companies, but for a business with such severe losses, it suggests the FADU stock is significantly overvalued relative to its net asset value. For more on valuation metrics, you can read this guide on PBR from Investopedia.

Strategic Guidance for FADU Investors

Given the heightened uncertainty and substantial risk, investors must adopt a cautious and strategic approach.

For Existing Shareholders

The immediate priority is risk management. With significant short-term selling pressure and a lack of positive catalysts, the potential for further price declines is high. It is prudent to consider loss-limiting strategies and avoid increasing your position until there are clear, verifiable signs of a fundamental turnaround. Monitor quarterly earnings reports and management communications closely for any evidence of a credible recovery plan.

For Potential New Investors

Initiating a new position in FADU stock at this juncture is an extremely high-risk endeavor. A falling stock price does not automatically make it a bargain. Before considering an investment, a thorough analysis is required. Wait for concrete evidence of improved profitability, a clear and executable strategic vision from leadership, and stabilization in the company’s shareholder base. To learn more about evaluating such situations, review our guide on analyzing high-risk tech stocks.

Conclusion: A Critical Turning Point for FADU

The convergence of a major shareholder’s exit and a severe financial crisis has placed FADU at a critical crossroads. The company’s management is now under immense pressure to restore market confidence. This will require more than just promises; it demands a clear, transparent strategy to return to profitability, secure long-term growth drivers, and communicate effectively with all stakeholders. For investors, the message is clear: proceed with extreme caution. The risks are substantial, and a tangible, evidence-based turnaround must materialize before FADU can be considered an attractive investment opportunity again.

Disclaimer: This analysis is based on publicly available information and is intended for informational purposes only. It does not constitute a direct recommendation for investment. Investors are solely responsible for their own investment decisions.

Leave a Reply