DAEMO Engineering Co., Ltd., a renowned manufacturer of specialized excavator attachments, has recently captured significant market attention. Two pivotal events—an increased share purchase by CEO Lee Won-hae and a remarkable financial turnaround in the first half of 2025—are sending strong signals to investors. This comprehensive analysis will delve into the implications of these developments, examine the company’s fundamental health, and provide a strategic outlook on DAEMO Engineering stock for potential investors.

A Bullish Signal: Decoding CEO Lee Won-hae’s Increased Stake

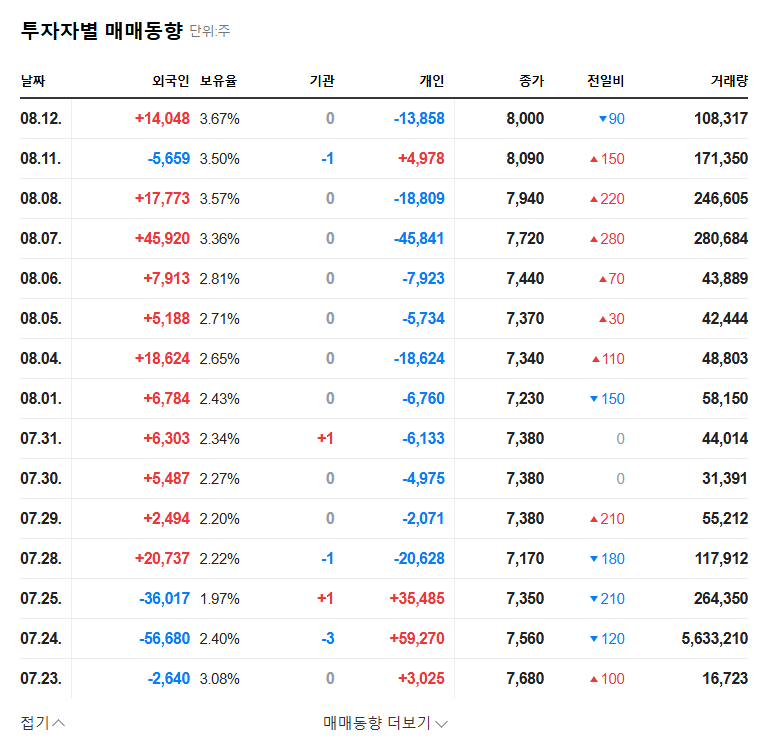

On November 12, 2025, a significant disclosure revealed that CEO Lee Won-hae acquired an additional 15,000 shares of DAEMO Engineering via open market purchases. According to the Official Disclosure, this transaction increased his total shareholding from 28.72% to 28.90%. While a 0.18% increase may seem modest, the context is critical. This move, stated to be for enhancing ‘management influence,’ is a powerful vote of confidence from the person with the most intimate knowledge of the company’s operations and future prospects.

When a CEO invests their own capital into the company they lead, it transcends a simple financial transaction. It signals unwavering belief in the company’s trajectory, a commitment to long-term value creation, and a move to align leadership’s interests directly with those of shareholders.

For the market, this action boosts investor trust by demonstrating that management is personally invested in the company’s success. It strengthens management stability and underscores a deep-seated confidence in the future growth potential of DAEMO Engineering.

Inside the Numbers: DAEMO Engineering’s H1 2025 Financial Turnaround

The CEO’s bullish move is underpinned by exceptional financial performance. DAEMO Engineering executed a spectacular turnaround in the first half of 2025, transforming its balance sheet and setting a positive tone for the future. This success wasn’t accidental; it was driven by strategic execution and favorable market conditions.

Record-Breaking Profitability and Global Reach

The most striking figure is the consolidated operating profit, which surged an astonishing 1,423% year-on-year to KRW 2.51 billion. This turnaround was fueled by robust overseas sales, which grew by 19.2%, showcasing the company’s global competitiveness in the excavator attachments market. Efficient cost management and a strategic shift towards higher-margin products were key internal drivers. Furthermore, the company maintains a very sound financial structure, with a low debt-to-equity ratio of 30.76%, providing a stable foundation for future growth. For more industry context, you can review our complete analysis of the construction equipment market.

Key Risk Factors to Monitor

Despite the positive momentum, investors must remain vigilant of potential headwinds. Domestic revenue saw a significant decline of 47.1%, a trend that requires careful analysis and strategic correction. Due to its large proportion of foreign currency transactions, DAEMO Engineering is also sensitive to exchange rate volatility; a 10% shift could impact pre-tax profit by approximately KRW 1.15 billion. Finally, underperformance in its Chinese and Indian subsidiaries and the company’s inherent sensitivity to the cyclical nature of the global construction industry remain important risk factors to consider, as noted in reports by outlets like the Financial Times.

Investment Outlook & Strategic Plan

Considering all factors, the investment appeal for DAEMO Engineering stock has increased significantly from a medium to long-term perspective. The combination of a proven financial turnaround and a clear demonstration of responsible management from DAEMO CEO Lee Won-hae creates a compelling narrative.

Here is a summary of the core considerations for your investment thesis:

- •Positive Driver: Massive profitability improvement signals strong earnings potential.

- •Positive Driver: The CEO’s stake increase enhances management transparency and trust.

- •Positive Driver: Growing overseas sales provide a sustainable engine for growth.

- •Risk Factor: Weakness in the domestic market needs to be addressed.

- •Risk Factor: Profitability is exposed to exchange rate and commodity price volatility.

Recommended Investment Strategy

From a short-term perspective, a dramatic stock price surge is not guaranteed, as the stake increase was incremental. Investors should monitor for further disclosures and sustained positive sentiment. From a medium to long-term perspective, the strategy should focus on the company’s ability to continue its overseas growth, successfully commercialize new products like forestry equipment and smart breakers, and effectively manage macroeconomic risks. A cautious, phased approach to building a position is prudent.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. All investment decisions should be made based on personal research and risk tolerance.

Leave a Reply