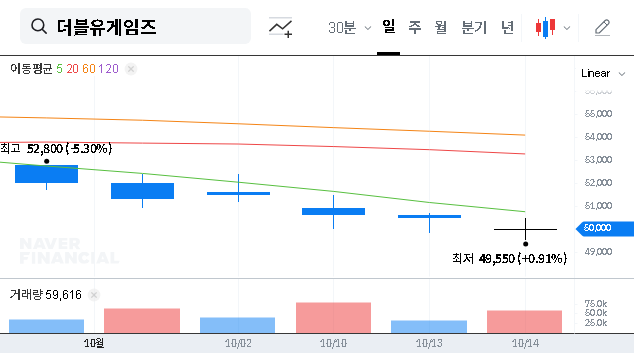

The latest DoubleUGames earnings report for Q3 2025 has sent a seismic shock through the investment community. On November 11, 2025, DoubleUGames Co., Ltd. (KRX: 192080) released preliminary results that drastically undershot market expectations, with both revenue and operating profit plummeting by over 70%. This unexpected downturn raises critical questions: Is this a temporary blip or a sign of a deep-rooted crisis? For holders of 192080 stock, this moment demands a thorough and clear-headed analysis.

This comprehensive deep dive will dissect the Q3 earnings shock, explore the underlying causes, evaluate the potential impact on the company’s fundamentals and stock price, and provide a strategic action plan for concerned investors. We will look beyond the headlines to understand the full picture of the challenges and potential opportunities facing DoubleUGames.

Deconstructing the Q3 2025 DoubleUGames Earnings Meltdown

The deviation from market consensus was not minor; it was a chasm. The preliminary Q3 2025 financial figures paint a stark picture of operational distress:

- •Revenue: Market expected KRW 186 billion, but the actual result was a mere KRW 43.3 billion, a shocking 77% decline.

- •Operating Profit: Analysts foresaw KRW 58.7 billion, while the company reported only KRW 14.1 billion, a 76% shortfall.

- •Net Profit: The expectation of KRW 48.2 billion was met with an actual figure of KRW 16.2 billion, a 66% miss.

After a period of relative stability in the first half of 2025, this abrupt cliff-edge drop suggests that the issues are not transient but potentially structural, stemming from deep-seated problems within the company’s core operations or strategic initiatives.

Why the Collapse? Analyzing the Root Causes

A performance drop of this magnitude is rarely due to a single factor. It’s likely a perfect storm of internal missteps and shifting market dynamics.

Core Business Under Siege in a Competitive Social Casino Market

DoubleUGames built its empire on the social casino market. However, this segment is facing maturation and increased competition. While the global mobile gaming market continues to expand, as noted in market analysis from sources like Statista, the social casino niche may be experiencing a slowdown. The Q3 results suggest that DoubleUGames’ existing IP and in-house capabilities were insufficient to fend off these pressures, leading to a significant drop in user engagement or monetization.

M&A Strategy Fails to Deliver Promised Growth

A key part of the company’s growth narrative was its expansion into casual gaming through the acquisition of Paxie Games and WHOW Games GmbH. Q3 2025 was the first period to fully reflect their contributions. The disastrous results indicate that the expected synergies and revenue boosts from these acquisitions have failed to materialize. Either the integration was poorly executed, or the acquired assets are significantly underperforming, unable to offset the steep decline in the legacy business.

This earnings report is a clear signal that the company’s M&A-driven growth strategy is under severe strain. Investors will now question the fundamental valuation and the leadership’s ability to execute a turnaround.

Outlook for 192080 Stock and Investor Strategy

The repercussions of this DoubleUGames investor analysis point to a challenging period ahead for the stock. Immediate, severe downward pressure on the stock price is expected as the market digests the news. Beyond the short-term reaction, a fundamental erosion of investor confidence is a major risk.

Key Points for Investors to Monitor

Navigating this situation requires caution and diligence. Rather than making rash decisions, investors should focus on the following critical areas:

- •Management’s Explanation & Turnaround Plan: The company must provide a transparent and credible explanation for the Q3 failure. Look for a detailed, actionable plan to stabilize revenue and cut unnecessary costs. Vague promises will not suffice.

- •Performance of Acquired Assets: Scrutinize future reports for specific performance data from Paxie Games and WHOW Games. Any signs of life or successful integration will be a crucial data point for recovery.

- •Financial Health & Shareholder Returns: The sharp drop in operating cash flow could impact the company’s ability to maintain its dividend and share buyback policies. Any change to the shareholder return program would be a major red flag.

- •Verify Official Filings: Always cross-reference analysis with the company’s official statements. The preliminary results can be viewed directly in the Official Disclosure on DART.

For those new to this type of situation, understanding how to properly analyze an earnings report is a critical skill. A cautious, wait-and-see approach is advisable until there is concrete evidence of a strategic correction.

Frequently Asked Questions (FAQ)

Why did the DoubleUGames Q3 2025 earnings miss expectations so badly?

The Q3 revenue and operating profit fell over 70% below forecasts. This is likely due to a combination of weakening competitiveness in its core social casino business, significant underperformance from newly acquired casual gaming companies, and potential unforeseen structural issues within its operations.

What is the likely impact on the 192080 stock price?

The severe earnings miss is expected to cause strong short-term downward pressure on the stock price due to widespread investor disappointment. In the long term, it could damage confidence in the company’s growth strategy and lead to a fundamental re-evaluation of its worth.

What should DoubleUGames investors do now?

A prudent approach is recommended. Avoid reactionary decisions like ‘bottom-fishing’. Instead, investors should wait for clear communication from management about the causes and their specific turnaround plan. Monitoring the performance of new acquisitions and any changes to financial policy is crucial before making new investment decisions.

Leave a Reply