The latest HAESUNG DS Q3 2025 earnings report has sent a strong positive signal across the semiconductor industry. HAESUNG DS Co.,Ltd. (195870), a pivotal South Korean semiconductor component manufacturer, announced preliminary results that not only recovered from a sluggish second quarter but decisively surpassed market expectations. This performance suggests more than a simple rebound; it could herald a broader semiconductor market recovery and ignite new growth momentum for the company.

This comprehensive analysis will unpack the significance of this earnings surprise, exploring the underlying financial and business factors. We will examine what these robust results mean for investors and how they might shape future stock prices and investment strategies. Join us as we explore the current valuation and future potential of HAESUNG DS.

HAESUNG DS Q3 2025 Earnings: A Decisive Beat

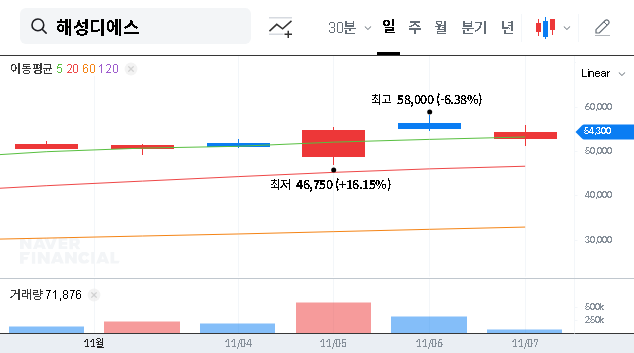

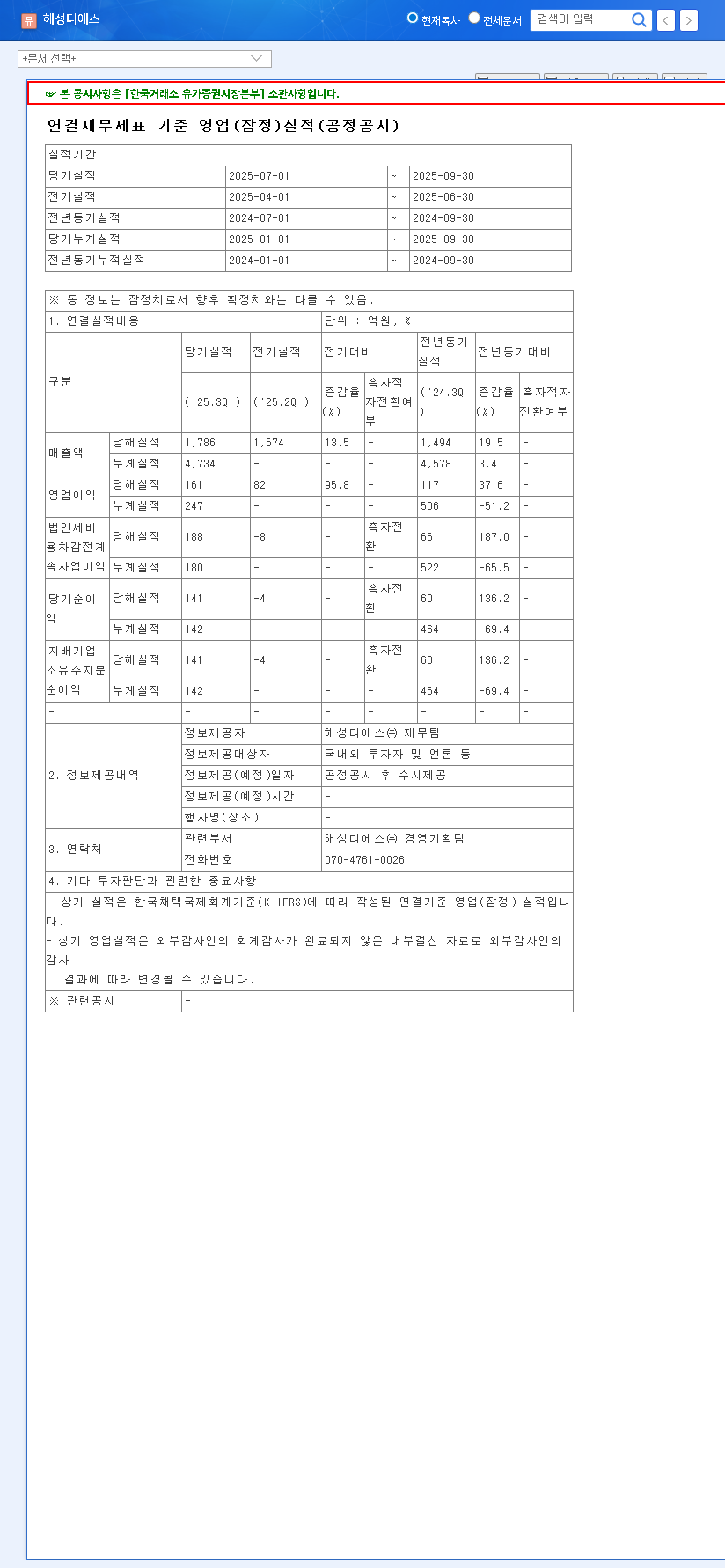

HAESUNG DS announced its preliminary Q3 2025 results, showcasing a remarkable recovery that significantly outperformed consensus estimates. According to their Official Disclosure, the figures point to a successful turnaround from the slowdown experienced in the previous quarter.

Key Financial Highlights:

• Sales Revenue: 178.6 billion KRW (+3% vs. estimate of 174.2B KRW)

• Operating Profit: 16.1 billion KRW (+18% vs. estimate of 13.6B KRW)

• Net Profit: 14.1 billion KRW (+26% vs. estimate of 11.2B KRW)

The double-digit beats in operating and net profit are particularly noteworthy, signaling a profound improvement in profitability that goes beyond mere revenue growth. This suggests strong operational efficiency and a successful strategic focus.

Core Drivers Behind the Strong Performance

This impressive turnaround is not a temporary anomaly but the result of several converging positive factors within the company’s core business segments and strategic execution.

Resurgence in Key Business Segments

The recovery in revenue was powered by two primary areas:

- •Solid Growth in Lead Frames: The global demand for automotive semiconductors continues to surge, directly benefiting HAESUNG DS’s automotive lead frame business. As a market leader in this niche, the company capitalized on the expanding EV market and the increasing electronic content in modern vehicles.

- •Stabilization of Package Substrates: The decline in the package substrate segment, a key concern in the first half of the year, appears to have bottomed out. This stabilization, coupled with the lead frame growth, created a powerful dual engine for revenue generation.

Mastery in Profitability and Cost Management

The significant outperformance in profit margins points to successful internal initiatives. The company likely implemented a combination of efficient production cost management and an improved product mix, prioritizing high-margin products. By focusing on high-value offerings, HAESUNG DS effectively protected its bottom line even amidst volatile raw material prices, a testament to its operational strength.

HAESUNG DS Stock Analysis & Investment Outlook

The outstanding HAESUNG DS Q3 2025 earnings report is poised to have a significant impact on investor sentiment and the company’s valuation. However, a nuanced approach is required when considering both short-term and long-term investment horizons.

Short-Term Momentum vs. Long-Term Fundamentals

In the short term, this earnings surprise will likely act as a strong positive catalyst, attracting buying interest and potentially driving the stock price upward. For a deeper understanding of market dynamics, investors can review related articles on broader semiconductor industry trends.

For a long-term HAESUNG DS stock analysis, investors must consider several key variables:

- •Sustainability: Is this a one-time rebound or the beginning of a sustained growth phase? Future earnings reports will be critical.

- •Financial Health: The strong Q3 performance will help offset the financial burdens from H1 investments, but diligent monitoring of the balance sheet is necessary.

- •External Risks: The company’s ability to navigate raw material price volatility (e.g., gold) and currency fluctuations remains a key determinant of long-term profitability.

Future Growth Engines and Challenges

While the current business is thriving, HAESUNG DS is also investing in next-generation technologies. The development of its graphene business is a key long-term growth driver. Graphene, a revolutionary material, has vast potential in electronics, and successful commercialization could open up significant new markets. For more on this material, authoritative sources like Graphene-Info provide excellent background.

Moving forward, the key challenge for HAESUNG DS will be to maintain its Q3 momentum while managing investment efficiency and financial stability. The market will be closely watching for sustained recovery in the package substrate segment and continued dominance in the automotive lead frame market.

Disclaimer: This analysis is based on publicly available information and is for informational purposes only. It is not intended as financial or investment advice. All investment decisions should be made based on the investor’s own research and judgment.

Leave a Reply