Investors are taking a keen interest in HD-Hyundai Marine Engine Co., Ltd. (071970) following its remarkable preliminary Q3 2025 earnings announcement. The company didn’t just meet expectations; it sailed right past them, delivering a significant ‘earnings surprise’ that signals accelerating growth and robust profitability. This report offers a comprehensive analysis of these results, dissecting the fundamental drivers, potential risks, and the long-term investment thesis for HD-Hyundai Marine Engine.

The Q3 2025 ‘Earnings Surprise’ by the Numbers

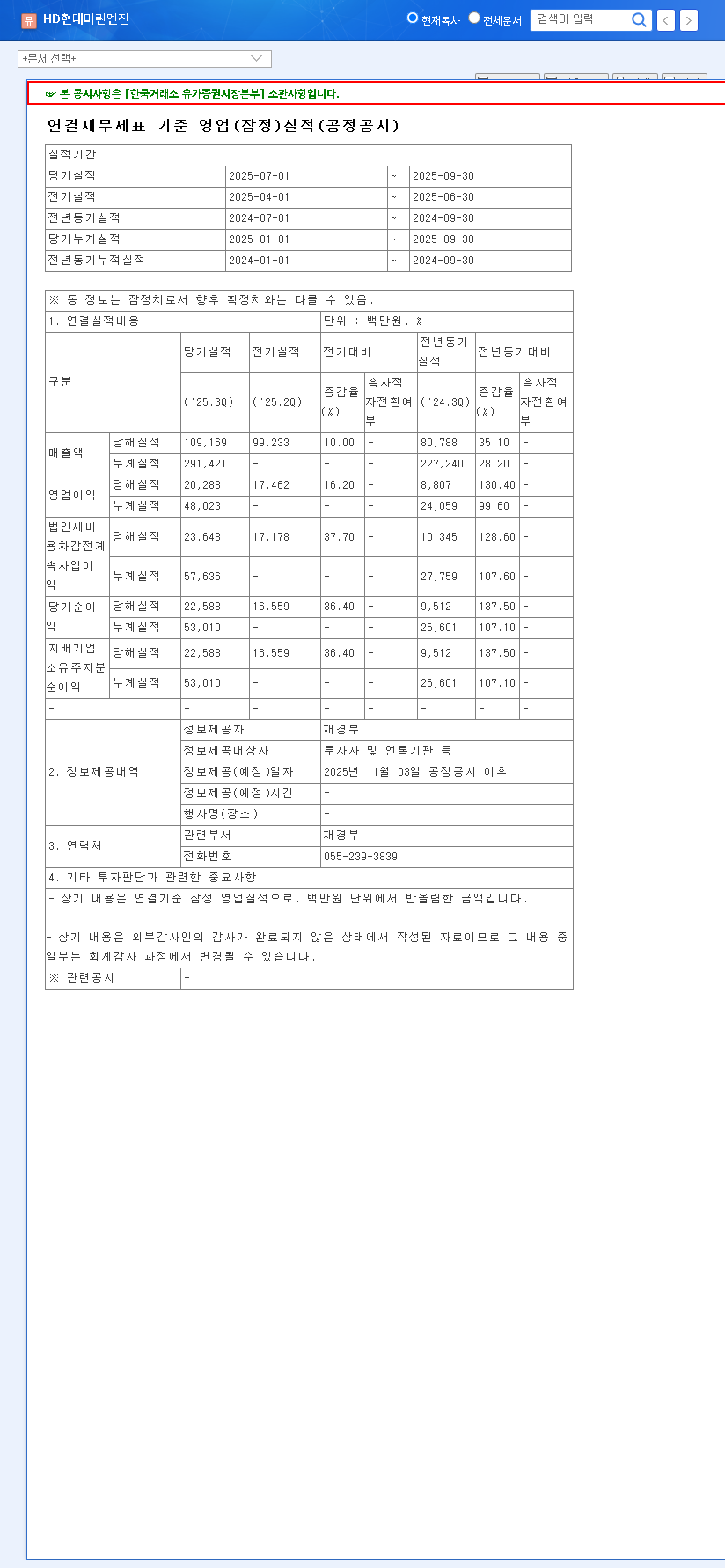

On November 3, 2025, HD-Hyundai Marine Engine released its preliminary consolidated operating results, decisively outperforming market consensus. This isn’t just a minor beat; the figures represent a substantial leap in performance, indicating strong operational efficiency and market demand. You can view the complete numbers in the Official Disclosure (Source).

- •Revenue: KRW 109.2 billion, a solid 6% above the market forecast of KRW 102.7 billion.

- •Operating Profit: KRW 20.3 billion, an impressive 22% above the forecast of KRW 16.6 billion.

- •Net Income: KRW 22.6 billion, a staggering 60% above the forecast of KRW 14.1 billion.

These powerful results underscore the company’s strengthening fundamentals and its ability to capitalize on current market conditions, setting a positive tone for investors and the broader market.

Core Growth Drivers: Analyzing HD-Hyundai Marine Engine’s Strengths

Behind these impressive numbers lies a foundation of strategic advantages and operational excellence. A closer look at the company’s fundamentals reveals several key growth drivers propelling its success.

Leadership in the Eco-Friendly Marine Engine Market

As global environmental regulations tighten, the demand for sustainable shipping solutions has skyrocketed. HD-Hyundai Marine Engine is at the forefront of this transition, specializing in dual-fuel engines that can run on cleaner alternatives like LNG and LPG. This positions the company perfectly to capture a growing share of the vessel replacement and newbuild market, driven by regulations from bodies like the International Maritime Organization (IMO). This strategic focus on eco-friendly marine engines is not just a trend; it’s a long-term structural shift in the industry.

Robust Order Backlog and Production Efficiency

A massive order backlog of over KRW 1 trillion provides exceptional revenue visibility and stability. This, combined with high production utilization rates—exceeding 90% for marine engines and an incredible 106% for 2-stroke crankshafts—demonstrates superior operational management. This efficiency not only ensures timely delivery but also directly contributes to healthier profit margins, a key factor in the recent earnings beat.

“The combination of a strong backlog and leadership in dual-fuel technology gives HD-Hyundai Marine Engine a powerful competitive moat. They are executing flawlessly in a market with clear, long-term tailwinds.”

Synergy and Financial Stability

Integration into the larger HD-Hyundai Group provides significant advantages. This relationship fosters group-wide synergies, enhances financial stability, and opens doors for strategic investments and business expansion. The dramatic improvements in operating profit (up 81.83% in H1) and operating cash flow are clear indicators of a financially sound and well-managed enterprise, a crucial point for any marine engine investment consideration.

Navigating Potential Risks and Headwinds

While the outlook is overwhelmingly positive, a prudent investment analysis requires examining potential challenges. Investors should remain aware of several factors that could impact future performance.

- •Exchange Rate Volatility: As a major exporter, the company’s profitability is sensitive to fluctuations in the KRW-USD and KRW-EUR exchange rates. Effective foreign exchange risk management will be critical to sustaining profit margins.

- •Segment Performance: The low production utilization rate for 4-stroke turbochargers (around 10%) presents an area for improvement. Boosting demand or reallocating resources in this segment could unlock further value.

- •Macroeconomic Factors: The global shipbuilding and shipping industries are cyclical. Changes in raw material prices, interest rates, and overall global trade will continue to influence the company’s trajectory. For more on this, see our overview of the industrial manufacturing sector.

Investment Thesis & Outlook for 071970 Stock

The Q3 2025 earnings announcement serves as a powerful validation of HD-Hyundai Marine Engine’s strategic direction and operational strength. The significant outperformance is likely to boost investor confidence and could serve as a catalyst for near-term stock price appreciation. Looking ahead, the company’s strong fundamentals and leadership in the growing eco-friendly marine engines market provide a compelling case for long-term value creation.

In summary, the investment appeal is high. While risks associated with currency and macroeconomic shifts must be monitored, the company’s core strengths present a clear and positive outlook. This earnings report reinforces the view that HD-Hyundai Marine Engine is not just surviving but thriving, making it a standout name in the global marine industry.

Disclaimer: This analysis is for informational purposes only and is based on publicly available data. Investment decisions should be made with the consultation of a qualified financial advisor.

Leave a Reply