In a significant development for the construction sector, KCC ENGINEERING & CONSTRUCTION CO., LTD. (KCC E&C) has officially secured a monumental contract valued at 227.1 billion KRW. This project, focused on a state-of-the-art logistics center, represents a major win that could reshape the company’s financial trajectory. But what does this deal truly mean for investors and the company’s stock value? This analysis dives deep into the contract’s specifics, KCC E&C’s current financial health, and the potential opportunities and risks that lie ahead.

We will unpack how this project not only signals external growth but also reinforces the company’s core competencies, providing a clear outlook for stakeholders making informed investment decisions regarding KCC E&C.

Unpacking the ₩227.1 Billion Contract

Key Project Details

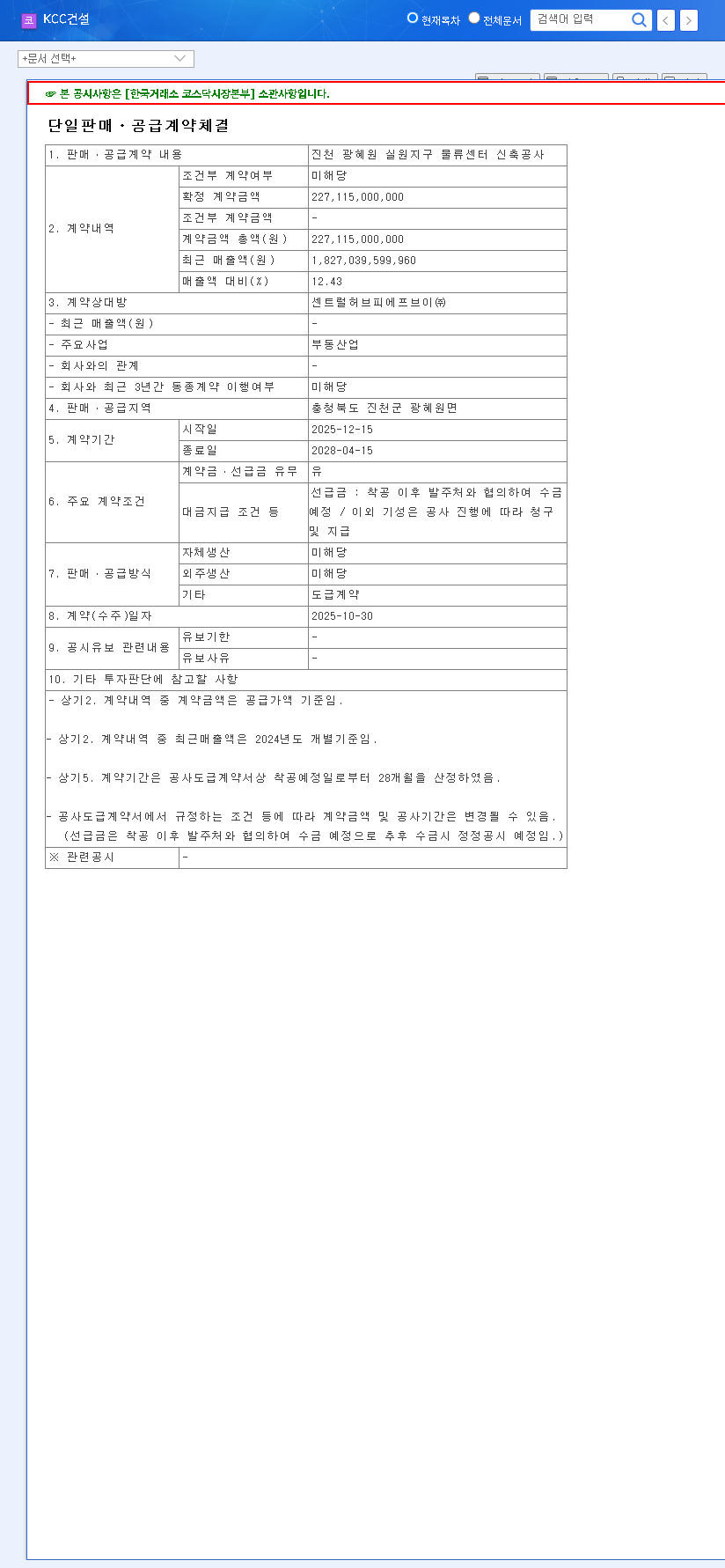

On October 31, 2025, KCC ENGINEERING & CONSTRUCTION formally announced its agreement with Central Hub PFV Co., Ltd. for the construction of the Jincheon Gwanghyewon Silwon District Logistics Center. The project’s value is an impressive 227.1 billion KRW, a figure that constitutes a substantial 12.43% of KCC E&C’s recent annual revenue. The official disclosure can be viewed directly on the DART system (Source).

The construction timeline is slated to begin on December 15, 2025, with a completion date of April 15, 2028, spanning approximately 28 months. This long-term project in Jincheon-gun, Chungcheongbuk-do, is set to become a cornerstone of KCC E&C’s portfolio, solidifying its dominant position in the large-scale building construction sector.

This contract is more than just a number; it’s a strategic move that significantly boosts KCC E&C’s order backlog, enhances its market reputation, and sets the stage for sustained profitability and growth.

Financial Health and Market Context

A Foundation of Strong Performance

This major contract win for KCC E&C doesn’t exist in a vacuum. It’s built upon a foundation of robust financial performance. The company’s 2025 semi-annual report revealed exceptional results: total assets grew by 8.89%, revenue climbed 6.15%, and most notably, operating profit skyrocketed by an astonishing 124.31% year-over-year. This surge improved the operating profit margin from 4.93% to an impressive 10.05%, signaling a dramatic enhancement in profitability.

The building division, which accounts for over 80% of total revenue, remains the primary engine of growth. Furthermore, the company is diversifying with its new ICT business, which is expected to begin generating revenue from smart safety technology systems. This move could further bolster its profit structure and create new synergies, like those detailed in our analysis of smart construction trends.

Positive Impacts on KCC E&C’s Outlook

The strategic implications of the Jincheon Logistics Center project are multifaceted and overwhelmingly positive. Here are the key benefits for the company:

- •Revenue & Backlog Growth: The ₩227.1 billion contract provides immediate, tangible growth to KCC E&C’s order backlog, guaranteeing a stable revenue stream for the next two-plus years.

- •Strengthened Core Business: Successfully delivering a large-scale logistics center enhances KCC E&C’s expertise and reputation, making it a more formidable competitor for future high-value projects in a growing sector.

- •Sustained Profitability: Building on the stellar performance of H1 2025, this project is expected to lock in stable profit margins, solidifying the company’s improved financial structure.

- •Innovation Synergy: The project presents a perfect opportunity to integrate KCC E&C’s smart construction and ICT solutions, showcasing their value and potentially creating new, high-margin business lines.

Potential Risks and Investor Considerations

While the outlook is bright, prudent investors must also consider potential challenges. A comprehensive stock analysis requires a balanced view:

- •Liquidity Management: The semi-annual report noted an increase in current liabilities. A large project like this requires significant upfront capital, making effective cash flow and liquidity management paramount to avoid funding strains.

- •Cost Control: The construction industry is susceptible to volatile raw material prices and intense competition. KCC E&C must diligently manage costs to protect the project’s profitability.

- •Execution Risk: A 28-month timeline introduces risks such as permitting delays, labor issues, or unforeseen site conditions. Staying on schedule is critical.

- •Macroeconomic Factors: Changes in the broader global economic environment, such as interest rate hikes or a slowdown in the domestic construction market, could impact financing and final profitability.

Final Assessment: A Catalyst for Growth

The KCC ENGINEERING & CONSTRUCTION logistics center contract is unequivocally a major catalyst for growth. It builds on recent financial momentum, significantly boosts future revenue visibility, and strengthens the company’s market leadership. For investors, this translates to a compelling long-term value proposition.

The key to unlocking this value will be KCC E&C’s ability to execute flawlessly while managing the inherent financial and operational risks. If the company continues its disciplined, profitability-focused strategy, this landmark project will serve as a powerful engine for sustainable growth and shareholder returns. Investors should closely monitor project milestones and the company’s quarterly financial reports for signs of continued strong execution.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Investment decisions should be made based on your own research and discretion.

Leave a Reply