The outlook for SEMCNS stock has become a primary focus for investors after the company announced a significant ‘earnings surprise’ in its Q3 2025 preliminary report. In a semiconductor market characterized by volatility, SEMCNS Co., Ltd. has distinguished itself with impressive growth, surpassing market forecasts and signaling a robust future. This performance isn’t a fleeting success; it’s a testament to the company’s strong fundamentals and strategic positioning in high-growth sectors.

This comprehensive analysis will delve into the factors behind SEMCNS’s remarkable Q3 results, evaluate its core technological advantages, and provide a forward-looking perspective on its investment potential. We will explore whether the current momentum in SEMCNS stock is sustainable and what investors should watch for in the coming quarters.

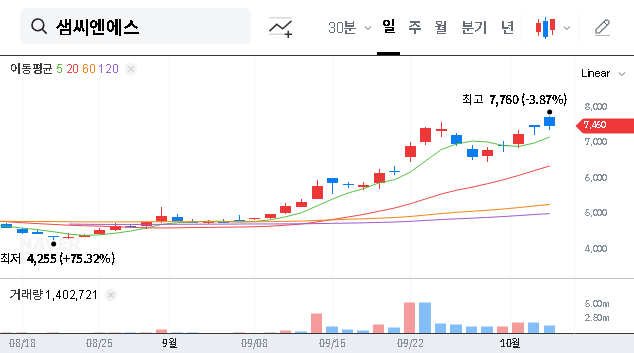

SEMCNS Q3 2025 Earnings: A Decisive Beat

SEMCNS Co., Ltd. delivered outstanding financial results for the third quarter of 2025, decisively beating market consensus. The preliminary SEMCNS earnings report highlights a company firing on all cylinders. You can view the complete filing here: Official Disclosure (DART).

- •Revenue: KRW 20.8 billion, exceeding the forecast of KRW 20.4 billion by 2.0%.

- •Operating Profit: KRW 5.4 billion, a massive 15.0% above the forecast of KRW 4.7 billion.

- •Net Profit: KRW 5.3 billion.

The year-on-year growth is even more staggering, with revenue surging 32.5% and operating profit exploding by 74.2%. This performance indicates powerful operational leverage and a sustained trend of improvement, solidifying the positive sentiment around SEMCNS stock.

Core Competencies Driving Explosive Growth

This ‘earnings surprise’ is no accident. It is the direct result of SEMCNS’s strategic alignment with high-demand markets and its unique technological moat.

1. Dominance in HBM and DRAM Components

The artificial intelligence revolution is powered by advanced hardware, and at its core is High Bandwidth Memory (HBM). SEMCNS is a key supplier in this ecosystem. The surging demand for HBM, coupled with the imminent approval for its multi-layer ceramic substrates for next-generation DRAM, places SEMCNS at the heart of the AI and data center boom. This synergy provides a powerful, long-term tailwind for the company’s growth.

2. The Technological Moat: LTCC Technology

SEMCNS’s most significant competitive advantage is its proprietary LTCC (Low-Temperature Co-fired Ceramic) technology. This technology is foundational to its ceramic STF (Socket Test Fixture) products, which are critical for semiconductor testing. Compared to alternatives, LTCC offers superior electrical performance, durability, and ease of multi-layer fabrication. This creates a high barrier to entry, protecting the company’s market share and profit margins. You can learn more about the broader semiconductor manufacturing process to understand its importance.

SEMCNS’s Q3 operating profit margin soared to nearly 26%, a dramatic increase from 18.7% in Q2 and just 8.9% in Q1. This demonstrates exceptional profitability and efficient cost management.

Investment Outlook: Strengths and Risks for SEMCNS Stock

A thorough semiconductor investment analysis requires a balanced view of both the opportunities and the potential headwinds. SEMCNS presents a compelling case, but investors must remain aware of the associated risks.

Key Strengths

- •High-Growth Alignment: Directly tied to the AI, HBM, and advanced DRAM markets.

- •Technological Superiority: Proprietary LTCC technology creates a strong competitive moat.

- •Financial Performance: Demonstrated ability to grow revenue while dramatically improving profitability.

- •Future Ventures: Active exploration into new sectors like advanced packaging, 5G/6G, and automotive modules.

Potential Risk Factors

- •Product Concentration: A high dependence on its Ceramic STF product line.

- •Industry Cyclicality: The semiconductor industry is known for its boom-and-bust cycles, as analyzed by institutions like McKinsey & Company.

- •Share Dilution: The potential conversion of outstanding convertible bonds could dilute equity for existing shareholders.

- •Macroeconomic Headwinds: Exposure to currency fluctuations and global interest rate policies.

Conclusion: A ‘Buy’ Rating with a Long-Term View

The analysis of the latest SEMCNS earnings report confirms the company’s powerful growth trajectory and strengthening market position. With a solid technological foundation and alignment with the most promising sectors of the semiconductor industry, SEMCNS has sent a clear positive signal to the market.

Considering these factors, we issue a ‘Buy’ opinion on SEMCNS stock. While the strong Q3 performance may fuel short-term appreciation, the real value lies in the company’s mid-to-long-term potential. Investors should continue to monitor the progress of its business diversification efforts and the broader health of the semiconductor market to make fully informed decisions.

Leave a Reply